Managing a complex portfolio and calculating cash dividends might be challenging. Here’s how it can be done with ease with a few formulas — and with the Navexa portfolio tracker.

Most people who consider investing are familiar with owning stocks. Some are also highly interested in receiving a dividend payout. Those who go deeper into researching an investment, might decide on purchasing stocks of companies because that pay cash dividends.

Dividends might help investors maintain a stable portfolio, remain invested in quality companies, and earn a profit, all while holding shares.

However, novice investors may find dividends confusing — especially when it comes to calculating their dividend yield per share.

The traditional way to calculate dividend per share is using the company’s income statement and similar reports. But, there are other, easier methods, too.

Dividends Explained

A dividend is defined as a distribution of a company’s earnings or stocks to a class of its shareholders. Dividend payouts are determined by the board of directors, and shareholders receive them for as long as they hold the stock.

A dividend is a form of reward to shareholders for investing in the organization and for holding the stock. Dividends may also help a stock’s price remain relatively stable.

Some companies offer dividend payments and prefer to keep the shareholders satisfied. Others decide not to pay dividends, instead reinvesting profits back into the company.

Dividends are paid monthly, quarterly, or annually, depending on the company. They’re paid at a scheduled frequency, so investors always know when they’ll receive the profit from holding shares.

Receiving a dividend based is a great way to increase one’s income, but there’s more to it.

Shareholders also pay attention to other factors, such as dividend yield, rates, retention ratio, and other key numbers.

Dividend Rate vs Dividend Yield

The dividend rate is a percentage that shows how much the company pays in dividends annually, relative to its stock price. The dividend rate can be fixed or adjustable, and it’s expressed as a dollar figure.

The dividend rate is calculated with the following formula:

Dividend rate = dividend per share / current price

On the other hand, the dividend yield is expressed as a percentage, and shows the ratio of a company’s annual dividend payout, compared to its share price.

Shareholders can calculate the dividend yield by using the following formula:

Dividend yield = annual dividends per share / current share price x 100

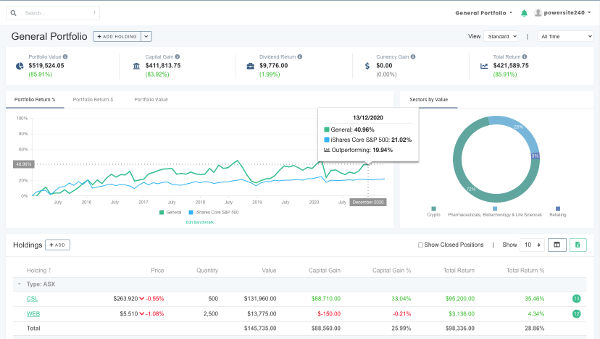

Navexa helps share investors by calculating dividend performance automatically. Navexa’s app is easy to use, and tracks multiple types of investments. This includes tracking and reporting on cryptocurrency investments.

Dividend Payout Ratio vs. Retention Ratio

The dividend payout ratio shows how much of the company’s earnings after tax are paid to the shareholders. It’s in direct relation to the organization’s net income amount, and it’s used to measure the net income percentage.

It’s calculated by the following formula:

Dividend payout ratio = total dividends / net income

On the other hand, the dividend retention ratio represents the percentage of net income that the company keeps to grow the business, instead of paying it out to the shareholders as dividends.

It’s calculated by the following formula:

Retention ratio = retained earnings / net income attributed to stockowners

Calculating Dividends per Share and Earnings per Share

Dividends per share (DPS) is the number of stated dividends paid by companies for each of the shares outstanding. It represents the number of dividends each shareholder receives based on the shares they own.

DPS is often used to calculate dividend yield, and the formula goes as follows:

DPS = total dividends paid over a period – special dividend payout / shares outstanding

On the other hand, earnings per share (EPS) are useful in calculating how profitable the company is based on measuring the net income for each of the company’s outstanding shares.

EPS is also an important number used to determine share price.

EPS shows whether investing in a certain company and holding its shares would benefit the shareholders and improve their net income.

For example, if the company reports an EPS that’s below a certain estimate, that might cause its share prices to drop.

The formula for calculating earnings per share goes as follows:

EPS = net income – preferred stock dividends / outstanding shares

Types of Dividends

There are several types of dividends that a company may pay to the shareholders. These include:

- Cash dividend

- Stock dividend

- Property dividend

- Liquidating dividend

Cash dividends are the most common. They represent a simple distribution of funds to incentivize shareholders to hold their shares, improve the shareholders’ equity, and increase confidence in the organization.

What Are Cash Dividends?

Cash dividends represent money a company pays to the shareholders per share they own. The money can come from the organizations’ current earnings or accumulated profit. Cash dividends are paid regularly, usually by quarterly or annual payments.

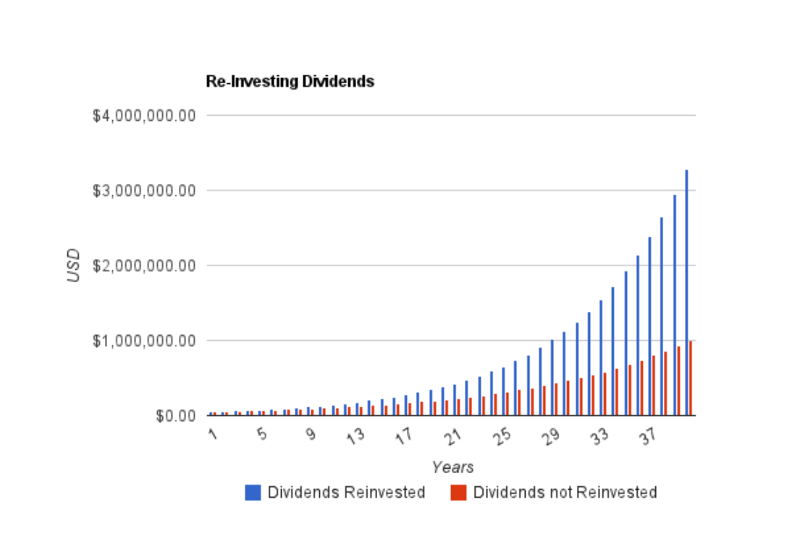

Once the shareholders receive this dividend, they may have the option to accept the cash payment, or reinvest in additional shares (known as a dividend reinvestment plan) and improve their position in the market.

The willingness of the company to pay cash dividends shows a solid financial strength, and positive performance, although that’s not always the case. Sometimes the companies may keep paying dividends, but still be in a poor financial position and eventually shut down.

This is why potential stock owners must be careful when investing and take everything into consideration before they invest in the organization.

Which Company Can Afford to Pay a Cash Dividend Yield?

Many companies have outstanding earnings, and can afford this form of dividend payout. These are just some of the companies that offer dividend payouts across the ASX, NASDAQ and NYSE:

- IBM

- AT&T

- Johson & Johnson

- QUALCOMM

- Fortescue Metals Group

- BHP

- Magellan Financial Group

More experienced investors can easily determine which company has a solid income statement, and capital, which helps them invest in profitable shares. On the other hand, novice investors may struggle in finding the dividend shares worth investing in.

Still, investing in shares that pay these types of dividends can help both new and experienced investors increase capital.

Additionally, those who wish to invest often check out the company’s trailing 12 months (TTM).

This is a set of performance data that shows how the organization managed finances in the last year. TTM is beneficial for understanding a company’s growth and potential.

Example of a Cash Dividend Payout

Here’s a simple example of a cash dividend:

One investor owns 100 shares of company X. At the end of a quarter, the company X calculates its financial performance for that quarter.

The board of directors then reviews the information, and decides on a $0.50 dividend per share for the quarter.

This means that the investor is entitled to $0.50 x 100 shares = $50

How Does a Cash Dividend Work?

When a company earns enough, it may decide to distribute part of its earnings to the shareholders. This part of the earnings is most commonly distributed via cash dividends paid in regular intervals, usually quarterly.

While these dividends are a great way of motivating shareholders to stay with the company, they may cause the stock price to drop. Still, investors love companies that offer dividends, as they know they can count on regular payouts.

Why Does a Cash Dividend Matter?

There are many reasons these dividends are important to shareholders. For example, the cash dividends could signal whether the company has good financial health.

It may show that a company is more effective in using its capital, compared to companies that don’t pay dividends.

Dividend payment per stock also increases the chance of shareholders remaining invested in the stock. This means the company’s stock price may stay more stable.

Are Cash Dividends Better Than Stock Dividends?

Even though these dividends are a more common way of paying shareholders, stock ones are sometimes considered better.

When it comes to the cash dividend, shareholders have no other option but to either keep it, or reinvest it and increase the number of shares they own.

With a stock dividend, they can keep the shares or turn them into cash. Plus, stock dividends aren’t treated as taxable, as they’re usually not turned into income.

The Advantages of Cash Dividends

There are many advantages of the dividend payout for shareholders. One of the main advantages is the steady income. These dividend payouts are regular, so shareholders know when they’ll receive the funds.

Regular payouts are especially beneficial for those who build a large portfolio with a view to living on the income.

Receiving dividend payments can also be a good way of establishing a market hedge. This defends the shareholders from the stock price dropping, which often happens during a bear market.

Furthermore, they know that companies that pay dividend yield may be more careful with their financial decisions, as they want to keep people invested in their shares.

The Disadvantages of Cash Dividends

While these types of dividends are common, and can yield great profit for investors, there are certain financial disadvantages for companies.

One of the major disadvantages to paying the dividend is that the money that’s paid to shareowners can’t be used to further develop the business. In a way, paying the dividend prevents the company from investing in increasing sales and profits. Instead, offering a healthy dividend might sustain or even raise the share price — effectively raising capital for the business.

When it comes to shareholders, dividend payments mean they’ll have taxable income. However, if an investor has an income that’s too low to make them liable for tax, they may be entitled to a refund from the Australian Taxation Office.

Do Cash Dividends Go on the Balance Sheet?

A balance sheet is a financial statement that involves the company’s stock, other assets, liabilities, and shareholder equity. This sheet is also used to evaluate the business.

Dividends do impact the balance sheet, as they will show a decrease in the company’s dividends payable, and financial balance. The balance will be reduced.

To check the total amount of paid dividends, investors should also use a financial statement. This statement shows how much money is entering and leaving the company.

Why Do Shareholders Prefer Cash Dividends?

According to financial theory, investors don’t care much about whether they’ll receive cash or stock dividends, for as long as they have the same value. However, this approach doesn’t include other complexities, such as taxes, transaction costs, dividend payout, demographic attributes of investors, etc.

On the other hand, the theory states that investors would pay additional expenses for receiving cash dividends, and they may prefer them over stock dividends.

Some shareholders would rather pay the taxes and receive cash for their outstanding shares, than receive additional stocks, simply because of direct financial compensation.

Accounting for the Cash Dividend

These forms of dividends are usually accounted for as a reduction of a company’s retained earnings. After the board of directors allows this type of dividend payout, the company debits the retained earnings account, and creates a liability account called ‘dividends payable’.

By moving funds to a dividends payable account, the company reduces equity, which is instantly shown in the company’s balance sheet even though no money has been paid out yet. This, in turn, increases liability.

Once the payment date comes, the company then reverses the dividend payable with a debit entry, and credits the cash account for the cash outflow.

In that way, these forms of dividends don’t actually affect the company’s income statement. Still, all companies that pay these dividends must report the payments in the cash flow statement.

Calculating Cash Dividend

Based on the complexity of these types of dividends, potential stockholders may struggle in finding the appropriate information they can use to calculate the dividend payout. In general, companies report their dividends in a statement they send together with their accounting summary to their stock owners.

Some organizations share the date in press releases. However, that’s not always the case.

Those who can’t find this data officially, usually consult the company’s balance sheet, which can be found in the annual reports.

Calculating Cash Dividend From a Balance Sheet and Income Statement

If the dividend payout is not explicitly stated in any public document, potential shareholders can look into two things:

- Balance sheet

- Income statement

The balance sheet is a record of the organization’s assets and liabilities. This document reveals how much the organization has kept in terms of retained earnings. Retained earnings are all earnings of the company that weren’t paid out as dividends.

The second document, which can be found in the annual report, measures the organization’s financial performance for a certain time period. The income statement shows how much net income a company had during a certain year.

This document helps determine what changes would occur in retained earnings if the organization had decided not to offer a dividend payout for that time period.

Calculating the dividend payout for the given year is done by subtracting the retained earnings from the beginning of the year from the end-of-the-year numbers.

This will give the net change in retained earnings, which should then be subtracted from the net income for the year.

The final number shows the total amount of dividends paid during the stated period.

Cash Dividend Per Share Formula

Those who wish to do their own accounting can easily calculate the earnings they receive from per-share dividend yield. After purchasing a stock that pays dividends per share, the shareholder would usually get quarterly dividend checks.

To find the dividend payment per share, the quarterly dividend payout should be divided by the number of shares.

To get annual numbers, the shareholder can multiply the quarterly dividend yield by four.

However, with Navexa, there’s no need to use complicated formulas to calculate the growth of a portfolio.

Navexa is a smart portfolio tracker that manages accounting for its users. Our app makes investing simple, as it automatically calculates portfolio changes.

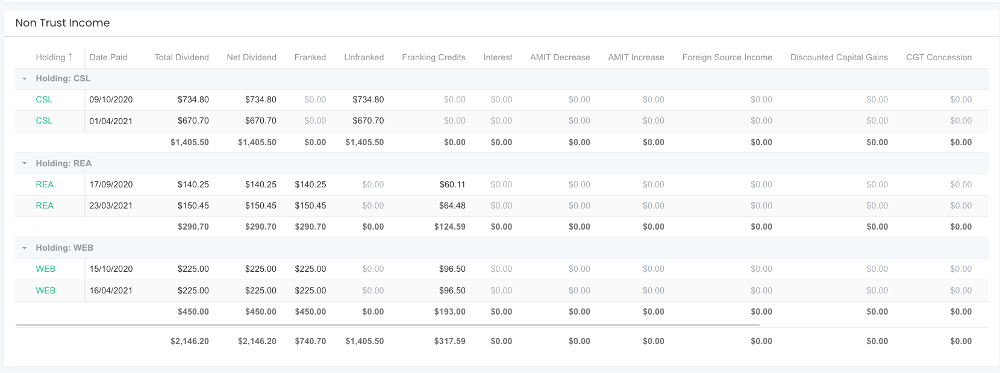

Navexa tracks and records every dividend payment — cash and reinvested — in a portfolio and provides insights into which holdings are earning the most and least in a given period.

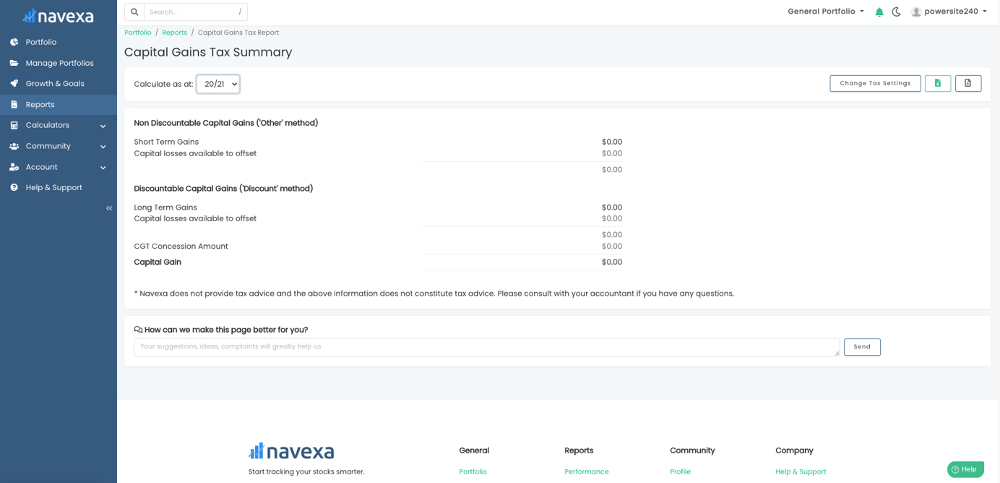

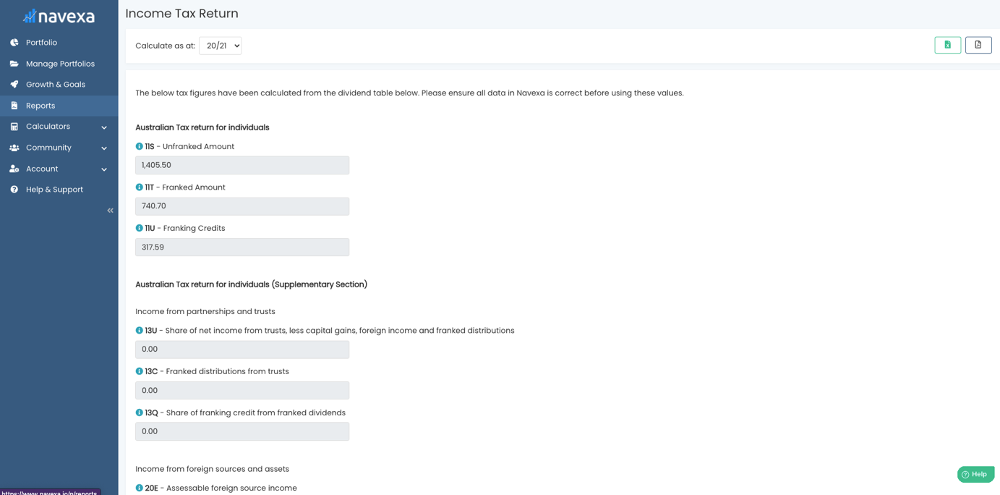

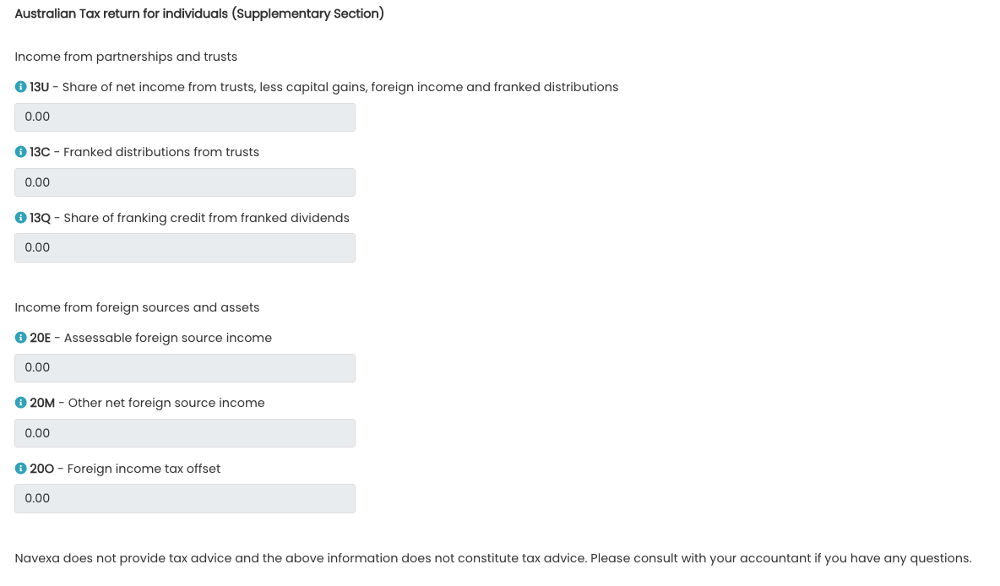

Plus, Navexa can annualize portfolio performance, and automate portfolio income tax reporting.

Final Word On Calculating Cash Dividends

Owning dividend-paying stocks is an attractive proposition and a key part of many investors’ long-term wealth building strategies.

But while earning income from an investing is good, it’s vital that investors keep track of their dividend performance — whether that’s from cash dividends or reinvested dividends.

This is important not just to understand and analyze how much a portfolio is generating in income (and how much that income contributes to overall performance), but because investment income is taxable.

Tax reporting requirements require that investors provide full details of their investment income.

That’s why we’ve built the Navexa portfolio tracker’s automated taxable income calculator. The tool calculates every last cent worth of income an investor needs to report for a given tax year, including details on franking credits (for Australian investors).

It’s part of our mission to empower investors to build brighter financial futures with simple, but powerful, automated investment analytics and reporting tools.