Foreign investment taxes can be complex. Generally, investors will pay capital gains tax or income tax, depending on the conditions. Here’s how to deal with Australian taxation on foreign investments.

Many Australians want to know how and where to invest in foreign stocks, property, bonds and other investments. This means they need to understand the tax implications of doing so. Australian taxation rules might seem complex when it comes to investing in foreign stocks.

The Australian government has signed many tax treaties. These provide benefits to Australian residents who invest in foreign stocks in countries that have tax treaties with Australia. Such treaties sometimes mean Australian residents may be exempt from paying tax. However, they may have to pay it in the foreign country.

If there’s no tax treaty, Australian residents may have to pay tax on every type of investment gain. Some might be eligible for a discount, depending on how long they have held the investment.

Generally speaking, foreign investments are taxable, be it in the source country or Australia. If you’re an investor, you’ll most likely pay capital gains tax or income tax. Keep reading to learn about Australian tax on foreign investments and how easy it is to track them using the Navexa portfolio tracker.

Overseas Investing From Australia

Australian residents are free to invest in foreign assets. They can own overseas property, offshore bank accounts, businesses, and stocks. Owning foreign investments requires that Australians comply with the latest rules and regulations regarding tax.

Australians can invest overseas, but need to understand their domestic and foreign tax obligations.

Interacting with the Australian Tax System

Every Australian resident is subject to tax on their income. This includes investment income such as dividends as well as capital gains from foreign investments. However, the Australian government has signed more than 40 tax treaties with other countries, including the US.

The US-Australia tax treaty gives Australian investors certain benefits. For example, there’s a reduced tax rate for US-sourced income (dividend payments) if certain conditions occur. Investors can also fill out specific forms that drop the rate of withheld tax from 30% to 15%. But, they may have to pay taxes in the US.

Australian investors might be able to claim US withholding tax from their dividends as a Foreign Income Tax Offset (FITO). FITO helps reduce taxes on foreign earnings.

But FITO rules are complex. It may be useful to seek professional guidance around this. Both the Inland Revenue Service (IRS) and US tax advisors can provide in-depth information for individual situations.

W-8BEN-E: A Key Form For Foreign Investors

The US government requires Australian investors fill out certain forms when investing in the country. A W-8BEN-E is a common form. It determines which investors are subject to paying 30% of their gross income earned in the US to the IRS. This form defines:

Interest

Royalties

Annuities

Rent

Premiums

Compensation for services

Substitute payments, if applicable

It’s required for all US holdings and remains valid for three years. If your information changes, you’ll be required to submit an update.

Australian residents for tax purposes have to declare all worldwide income.

Do Australian Residents Pay Tax on Gains and Income from Foreign Investments?

Australian residents for tax purposes have to declare the income they earn regardless of where that income came from. This is called the ‘worldwide income’ and it includes:

Pensions

Annuities

Business activities

Employment

Assets

Investments

Dividends from shares

Capital gains on overseas assets

Interest from bank deposits or bonds

Rental income from real estates

Royalties from intellectual property

If you have a temporary resident visa, you won’t pay tax on income. In case you receive income from a country that hasn’t signed a tax treaty with Australia, you’ll likely pay taxes in both countries. However, the tax you pay in a foreign country may make you eligible for FITO.

Australia also receives and exchanges information on all financial accounts with many foreign tax authorities.

How Is Foreign Investment Taxed?

Australian investors who have foreign assets and receive income from overseas will usually have to pay capital gains tax once they sell that asset. However, there could be other forms of taxes they are required to file (such as income from dividends). This is why it’s important to keep all the records on transactions, regardless of the country in which you invest.

Here’s where Navexa makes life easier. Our smart portfolio tracker lets you track foreign investments in both their local currency, and your tax residency’s currency, too.

This makes it super simple to monitor the performance of your foreign shares and keep records of all transactions for tax and compliance purposes.

The way dividends are taxed depends on the tax treaty between Australia and the source country.

Types of Investments and Their Taxation

Australian investors have access to several investment opportunities abroad. These are the most common ones.

Buying & Selling Stocks

Australians can own foreign stocks. Any individual who holds shares for more than 12 months may be eligible for the CGT discount. If they make a gain when they sell, Australian investors are required to notify the Australian Taxation Office. Investors are also advised to consult with the foreign tax authority to check the taxation process on capital gains.

Receiving Dividends From Foreign Investments

The way dividends are taxed depends on the tax treaty between Australia and the source country. In many cases, the source-country dividend tax is limited to 15%. Receiving dividends from companies that satisfy certain public listing requirements may result in tax exemption.

Depending on the conditions, some investors may be eligible for ‘franking credits’. That’s a form of tax credit that can offset against tax on dividends. Generally speaking, those who hold shares for a certain holding period (45 or 90 days) may be eligible.

Cryptocurrencies

In recent years, cryptocurrencies have become a major investment theme for Australian residents. When it comes to paying tax, Australian investors have to pay capital gains tax on crypto. On the other hand, professional traders pay income tax.

P2P Lending

Peer-to-peer (P2P) lending is a form of investment that’s accessible globally. Australians can access P2P lending platforms and lend money to borrowers without an intermediary. Peer-to-peer lending income listed in an investor’s loan portfolio will be included in the tax return form. For most people, this income is taxed like income from other investments. Australians who earn via P2P lending in foreign countries should consult their accountant.

Property Income

Australians who realize a gain when they sell foreign property are required to pay capital gains tax. However, if they held the property for 12 months or longer, they might be eligible for a 50% capital gains tax discount.

Additionally, investors who are subject to an overseas tax after selling their property will receive tax credits in the form of a foreign tax offset. Rental income may also be taxable in Australia or a foreign country, depending on the location of the property and current tax treaties.

Purchasing Bonds

Bonds can be highly tax efficient, since there are some benefits for those who hold them for 10 years. Otherwise, bonds are subject to the corporate tax rate of 30%. Investing in bonds means investors might not be eligible for tax credits and some other benefits.

Foreign Investment Capital Losses

Investors may sell a foreign investment for a lower price, and end up with a capital loss. In some cases, investors can use capital losses to reduce capital gains tax. Capital losses must be used at the first opportunity, unless there are restrictions. Capital losses can’t be used to reduce income, and should be reported to ATO just like capital gains.

Navexa lets you track foreign investments in both your tax residency’s currency and the local currency of the asset.

Foreign Investments: Track Everything Correctly

If you’re an Australian resident for tax purposes, you’ll be required to pay some form of Australian tax on foreign investments.

In general, all your worldwide income will be subject to tax, it’s just a matter of where you pay that tax. It’s always a smart idea to get familiar with the laws around this, and to consult professionals regarding your personal financial situation.

Further to this, serious investors should always track their transactions and portfolio performance for the purposes of both compliance and optimizing their investment strategy.

The Navexa portfolio tracker does exactly this. Track Australian and overseas investments, access detailed performance analytics on income, currency, trading fees and more.

And, most importantly, ensure your foreign investment gains and income are reported accurately at tax time.

Sign up to Navexa now for a free 14-day trial to see how easy tracking and reporting on foreign investments can be!

Your guide to calculating capital gains tax in Australia in 2022. From tax rates, CGT events, taxable income and more. Plus, discover four key tax reporting strategies investors use to adjust and optimize their total taxable capital gain.

Paying tax is a part of investing. It has long been a fact of life that a significant portion of our earnings will always be earmarked for payment to the state. This includes capital gains.

Tax is applied to a wide range of earnings including wages, salaries, and investment income from property, shares, and cryptocurrency.

In Australia, the tax rate that is applied to your investment income is known as the Capital Gains Tax, or CGT.

Whether you’re a seasoned investor or just starting out, it’s important to be aware of how CGT works. This article will explain how the CGT works, and how to calculate and report your capital gains in Australia in 2022.

While you can’t avoid paying CGT on your investment income, there are some strategies you should be aware of for minimizing the impact of tax on your capital gains. This blog post examines some of these strategies and provides examples of how they might look.

The Australian tax year, or financial year, runs from July 1 to June 30. This is the period for which you will need to submit your tax assessment based on any income you received during the financial year. This period is known as ‘tax season’.

How Does CGT Work?

The Australian Tax Office (ATO) requires individuals to declare investment activity in their tax return and pay tax on all investment earnings, including capital gains and dividend income.

If you buy shares, invest in property, or hold other investments which you sell at a higher price than what you bought them for, you will have made a capital gain. This means you will be paying CGT.

CGT is the tax rate that is applied to net capital gains (total gains minus total losses). It is not a set rate, but is calculated according to your marginal tax rate. This is the tax rate that you usually pay on your personal income, and will be the tax rate applied to your investment earnings.

Capital gains are taxed at an individual’s marginal tax rate

While CGT rates for individuals vary according to their marginal tax rate, flat rates apply for companies and self-managed funds.

Trading companies pay 26% if their annual turnover is less than $50 million, and if it exceeds $50 million, the CGT applied is 30%. Investment companies don’t qualify for the 26% rate and are taxed at 30%. Self-managed super funds are taxed at a lower rate of 15%.

If you sold any assets during a financial year, you will need to work out your capital gain or capital loss for each asset. CGT will need to be paid on your net capital gains.

To calculate your capital gains, you first need to know the ‘cost base’ or original purchase price of the asset. From there, you can work out how much profit you’ve made by subtracting the selling price from the cost base.

Depending on how long you’ve held the shares for, you may or may not qualify for Australia’s 50% CGT discount on investments held longer than 12 months.

The Navexa platform provides an automated solution for making these calculations — more on that later.

That’s how the CGT rate is determined. So, let’s take a closer look at which investments the CGT applies to.

What Does CGT Apply To In Australia?

CGT applies to a wide range of investment income in Australia, including earnings generated from real estate, shares, cryptocurrency, foreign exchange, and collectibles.

When you dispose of an asset for more than what you paid for it, you realize a capital gain which you will have to pay CGT on.

There are a range of other situations that will trigger the requirement to pay CGT. These are known as ‘CGT Events’. A CGT event occurs when an investor makes a capital gain or incur a capital loss on an asset.

The Australian Tax Office (ATO) imposes CGT when you make a capital gain or loss

How Does CGT Apply To Shares?

When you sell shares for more than what you paid for them and realize a capital gain, you will have to pay CGT. When other CGT events occur, you will also have to pay CGT on your shares. Examples include switching shares in a managed fund between funds, or owning shares in a company that is subject to a takeover or merger.

It is important to keep good records of all your share transactions, including amounts and dates of purchase. When you file your tax return, CGT will need to be calculated for any profits you made from selling your shares.

Does CGT Apply To Dividend Pay-outs?

Many Australian investors enjoy investing in companies that pay out dividends (a percentage share of their profits) to their shareholders. But, like other forms of income, dividends are subject to taxation.

Dividends are paid from profits that have already been subjected to Australian company tax. Because the profits have already been taxed, shareholders won’t be taxed again when they receive the profits as dividends, provided that their marginal tax rate is lower than the tax rate paid by the company.

These dividends are described as being ‘franked’. A ‘franking credit’ is attached to the dividend and represents the tax that has already been paid by the company distributing the dividend. The shareholder who receives the dividend with an attached franking credit will either pay less than their usual tax rate, or receive a tax refund.

The general rule is that if your marginal tax rate is lower than the rate of tax paid by a company or fund, you might be entitled to claim a refund. However, if your marginal tax rate is higher than the tax already paid on the dividend, you may have to pay additional tax.

Does CGT Apply To Crypto?

If you were hoping to avoid paying CGT by investing in cryptocurrency, we have bad news for you. Cryptocurrency investment in Australia is also subject to taxation, in a similar way to other investment assets.

In recent years, the cryptocurrency market has grown rapidly, and the ATO has been quick to catch up.

Crypto gains are subject to CGT in Australia.

Cryptocurrency markets have exploded in recent years and the ATO is all over it

As with other assets, CGT may apply in circumstances other than just selling your crypto. The ATO classifies four main CGT events for crypto activity:

You’ll be taxed when you:

Sell crypto.

Exchange one crypto for another.

Convert crypto to a fiat currency like AUD.

Pay for goods or services in crypto.

Just like when you pay CGT at your marginal tax rate when you sell shares, you pay this rate when you sell crypto.

Generally, you could apply the same tax rules to your crypto portfolio as you would for investment in stocks.

You must pay CGT when you realize a capital gain from property. This could include selling an investment property for more than what you paid for it or selling a block of land that you created through a subdivision process.

Your main residence is generally excluded from CGT if you meet certain criteria specified by the ATO:

You will need to have lived in the home for the whole period that you have owned it.

The home can’t have been used to produce income or have been bought with the intention of renovating and selling it for a profit.

It must be on land no greater than two hectares.

If you meet the criteria, you may be able to avoid paying CGT when you sell your house. If not, you may still qualify for a partial exemption. The ATO provides a property exemption tool on their website to help you make the calculations.

In Australia, investors can expect to pay CGT on shares, crypto, property and more.

Capital Gains Tax (CGT) has to be paid on investment income from property

If you acquired property on or prior to 20 September 1985, CGT does not apply. But it will apply to certain capital improvements made after this date. It is also important to keep track of any rental income you receive from property and include it in your tax return. For more details on CGT and property, visit the ATO.

If You Are An Investor, It Pays To Know About CGT

As you can see, CGT applies to a wide range of investment income. When you prepare your tax return, you will need to provide the ATO with your assessable income and any capital gains or capital losses you made that year.

While this article isn’t financial advice, we do advise you to be well informed. The above is not an exhaustive list of what CGT applies to in Australia, so you should check with the ATO if you are unsure about what your tax obligations are.

You can’t escape having to file a tax return, but fortunately there are a few strategies you can use to reduce your tax burden, legally.

Let’s explore some of the strategies that investors use to minimize investment tax.

Effective Strategies To Minimize Tax Payments

There are several legal investment strategies investors employ to minimize tax bills and claim tax deduction. This goes for both gains and income.

Below you’ll find some of the ways Australian investors hold on to as much of their investment gains and income as possible.

The following is not investment advice. As with all the information on the Navexa blog, it’s general investment information our writers have collated from other sources. For any financial or investment decisions, you should always understand the risks, and seek professional advice if necessary.

Strategy 1: Hold Onto Your Investments For Longer Than 12 Months

Australian tax law makes a distinction between short and long term capital gains. A long term capital gain is when you make a profit on an investment that you’ve held for longer than 12 months. It’s a short term capital gain if you’ve held the asset for shorter than 12 months.

As an investor, this is important to understand because of something known as the ‘CGT discount’.

If you’ve held an asset for longer than 12 months before a given ‘CGT event’ occurs, you may be able to claim a CGT discount of 50%. Remember, a ‘CGT event’ is the point at which you make a capital gain or loss on an asset.

Let’s say you made $30,000 profit from investments that you’d held for less than 12 months, and your marginal tax rate was 37%. You’d have a $11,100 tax liability.

However, if you’d held the asset for longer than 12 months before you sold, the CGT discount would mean your tax liability was just $5,500! That’s a significant amount saved on your tax bill.

Capital Gains Tax discount applies to a wide range of investment income, including shares, property, and cryptocurrency.

As you can see, holding onto your investments for longer than 12 months to take advantage of this discount can be much more tax effective than disposing of them quickly.

Remember, you must be an Australian resident for tax purposes to take advantage of the CGT discount. There are also some other situations where the CGT discount does not apply.

For example, the discount is not available if the asset is your home and you started using it as a rental property or business less than 12 months before disposing of it.

A CGT discount of 50% is available to Australian trusts, and complying super funds can receive a discount of 33.33%. However, companies can not take advantage of the CGT discount.

When you file your tax return, you must subtract any capital losses that you may have from your capital gains before applying the CGT discount. In most cases you will be eligible for the discount if the asset has been held for longer than 12 months.

Navexa provides a platform where you can easily track your portfolio performance and calculate both your taxable capital gains and taxable income. Our CGT Reporting Tool gives a detailed breakdown of which assets are ‘non-discountable’ from a CGT perspective (those which have been held for less than the required 12 months to qualify), reducing the amount of tedious leg-work at tax time.

Navexa’s tax reporting tools remove the need to manually calculate your portfolio’s tax obligations and show you the most tax effective way to prepare a tax return.

Provided the portfolio data in your account is correct and up-to-date, you can run an automated tax report in just a few seconds.

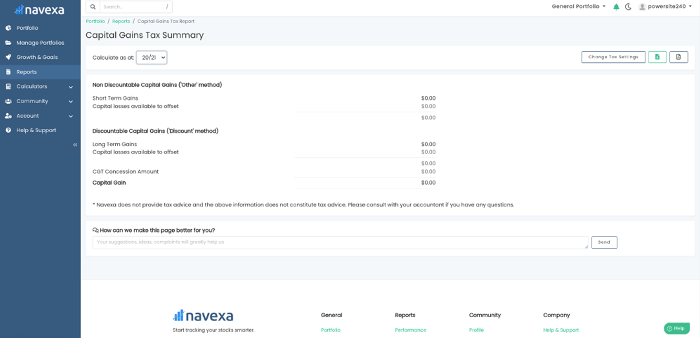

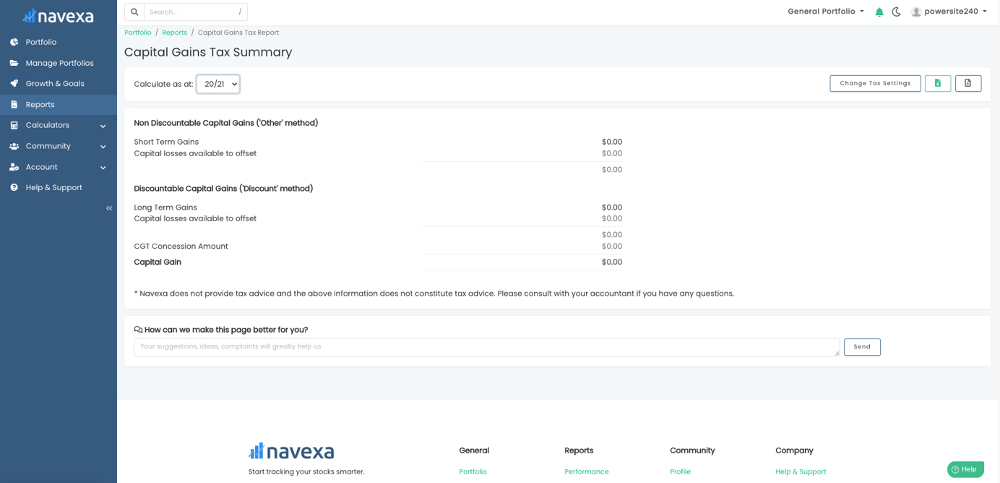

Navexa’s CGT Reporting Tool.

What you see above is Navexa’s CGT Report.

Navexa calculates your taxable gains and displays a detailed breakdown. Capital gains are displayed according to Short or Long Term status alongside your Capital Losses Available to Offset. The report also calculates your CGT Concession Amount and finally, your total Capital Gain.

Navexa’s CGT Reporting Tool makes it easy to categorize your investments for your tax return.

Strategy 2: Offset Your Capital Gains With Capital Losses

Another useful strategy at tax time is using capital losses to offset your capital gains. While it would be nice if your assets always made gains and never losses, most of us who invest know that this isn’t the case. Thankfully, the silver lining here is that your capital losses can be used to reduce the tax you pay on your capital gains.

You will have made a capital loss when you sell an asset for less than what you paid for it. This loss can be deducted from capital gains that you made from other sources, to reduce the tax you pay. If you don’t have any capital gains to deduct from, the capital loss can generally be carried forward to future financial years. If you make capital gains in future years, the capital losses are still up your sleeve to deduct from any gains and reduce tax.

While there is no time limit on how long you can carry the losses forward if you don’t make any gains, the ATO does require that capital losses are used at the first available opportunity. This means when you have a capital gain to declare and capital losses available to offset, you must do so. They also require the earliest losses to be used first.

For example, if an investor owed $5,000 in CGT for their investments in a financial year, but had declared losses of $1,500 the previous financial year, they could carry these losses over to offset their capital gain, resulting in a reduced tax bill of $3,500.

There are some capital losses that can’t be deducted, so be aware of these. These include personal use assets such as boats or furniture, or collectables below a certain value. The ATO also won’t allow capital losses to be deducted from collectables unless they are deducted from capital gains from collectables.

Capital losses can also be deducted from your cryptocurrency assets, too. Let’s say you bought $5,000 worth of Ethereum because it had been surging in price and you were experiencing crypto-FOMO. You buy near the peak and in subsequent weeks the price crashes heavily, after a large nation announces that it won’t endorse cryptocurrency in their economy. Despite this disappointment, don’t forget that if you sell the asset and realize a capital loss, it could be a handy tool to offset other capital gains in your portfolio.

Despite a few exclusions, however, most capital losses from your investments can be deducted from capital gains you have made from other assets. If you are unsure about whether you can deduct a particular capital loss, check with the ATO.

Strategy 3: Invest In Companies That Pay High Dividends And Franking Credits

We’ve already looked at how the ATO taxes dividends, so what does this mean for minimizing your income tax obligations? Again, this is not financial advice.

Remember that companies must pay the Australian Companies Tax on their profits. If an investor receiving a dividend has a tax rate greater than the company tax rate that has already been applied to the company’s profits, they will receive a franking credit.

Let’s look at an example. Say an investor with a 32.5% tax rate receives a $1,750 dividend with a $750 franking credit attached. The franking credit takes the taxable income to $2,500, with gross tax of $812.50 payable. The franking credit rebate of $750 is deducted from the gross tax and the investor is left to pay a reduced tax amount of $62.50, leaving them with $1,687.50 after tax income. As you can see, the impact of the franking credit rebate is significant. For a full breakdown of this and other franked dividend scenarios, click here.

The investor in the above situation manages to retain most of their dividend income. Because the franking credit offsets their CGT so significantly, the amount of tax the individual pays is greatly minimized. Obviously, if your marginal tax rate is lower than 32.5% you will pay less tax and receive a larger chunk of the dividend. If you’re in a higher tax bracket than this, you will receive less.

Regardless of your marginal tax rate, franked dividends are a useful tool to reduce your tax obligations. Choosing to invest in companies that pay dividends, especially fully or highly franked dividends, is a popular strategy for minimizing tax paid on investment returns.

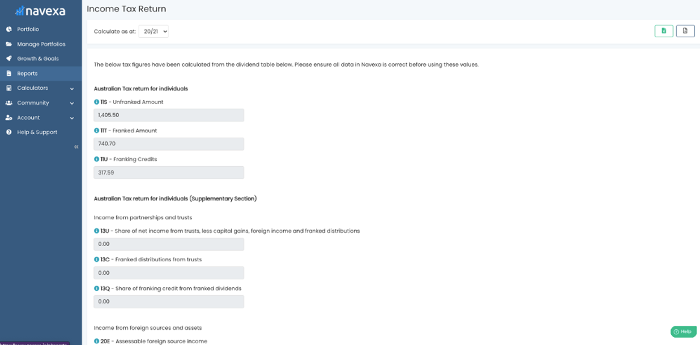

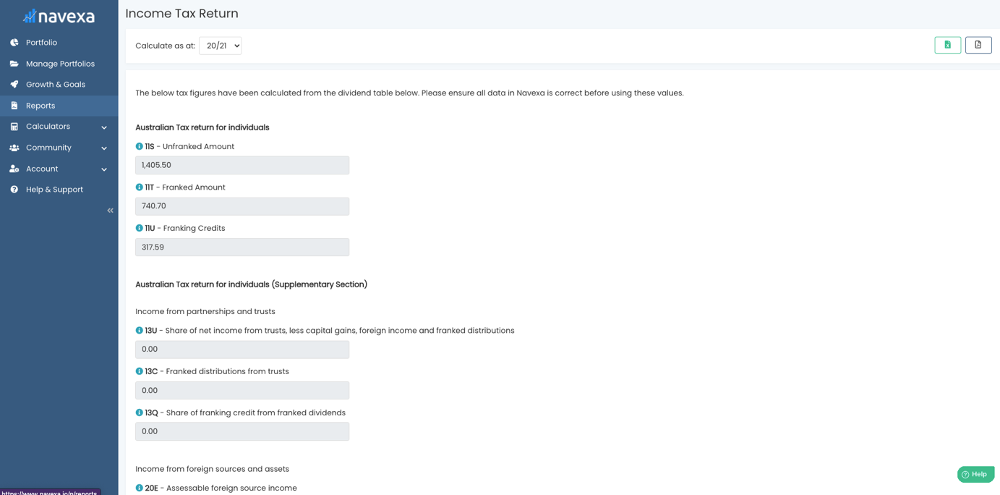

Navexa’s Taxable Income Reporting Tool

Navexa can help you accelerate the process of determining your taxable income. When you automate your portfolio tracking in Navexa, the Taxable Investment Income Report provides you with everything you need to know to prepare your tax return.

Navexa’s Taxable Investment Income Tool.

As you can see above, the Taxable Income Tool displays the Unfranked Amount and the Franked Amount for your dividends, as well as the total franking credits attached to them.

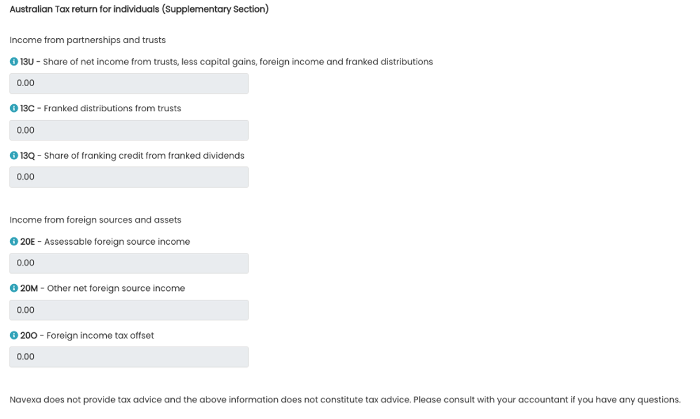

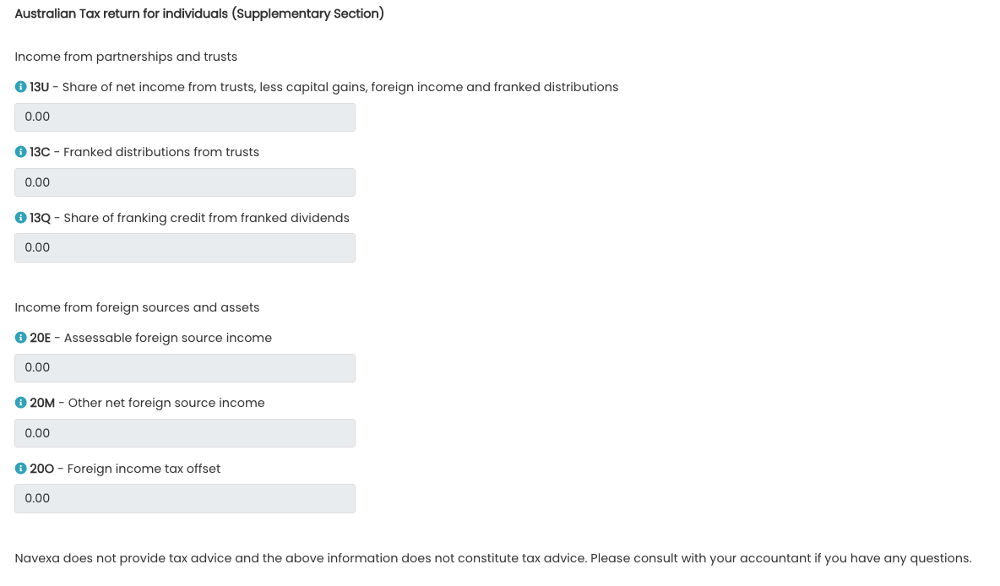

And in the below image, you can see the additional fields in the ‘Supplementary’ section. These display further tax-relevant information such as the amount of Franked Distributions From Trusts, the amount of Assessable Foreign Source Income, and your Foreign Income Tax Offset.

The report automatically categorizes sources and tax return codes.

A foreign income tax offset is when you may have already paid tax on something in another country. This might be employment income or capital gains. In some instances, you may be able to claim a foreign tax offset as part of your tax return. Navexa’s Taxable Investment Income Tool will calculate and display these details for you.

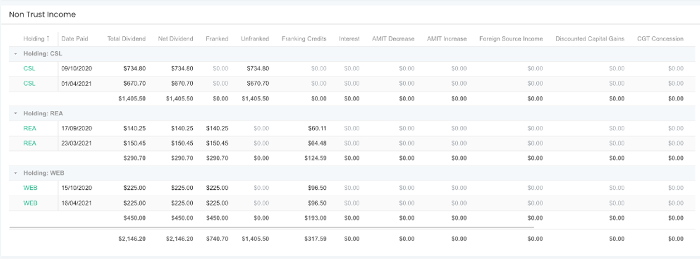

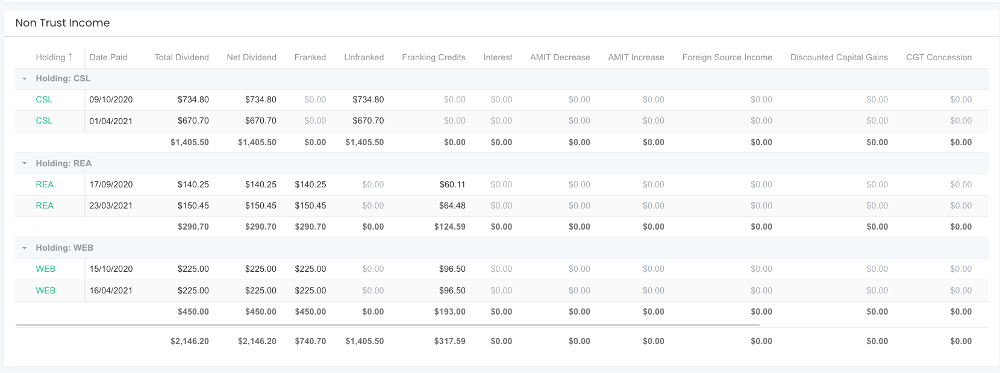

Below these fields, you’ll be provided with a holding by holding breakdown of your taxable investment income, like this:

Navexa’s holding by holding investment income breakdown.

This shows you subtotals for payments from each holding, with grand totals for each column at the bottom. Assets are organized by the dates at which you acquired them, which has important tax implications.

At the top right of the report, you’ll find buttons for exporting the report as both an XLS and a PDF file.

This helps you accelerate the process of preparing your investment income for assessment.

Let’s take a look now at how different investors might choose to dispose of their assets.

Different Tax Strategies For Disposing Of Investments

When the time comes that you want to sell, it can be easy to get excited about the potential gains you are about to realize. This excitement can be dampened, however, when you are faced with the reality of your tax bill.

Choosing a particular method to dispose of your assets can have a major impact on the profits you generate and the tax you pay on them.

Please remember that this does not constitute financial advice. Our writers have collated a wide range of information relating to investment tax that we think is useful for you to consider. As always, we recommend you do your own research before making any investment decisions — tax or otherwise

Strategy 1: First-In-First-Out (FIFO)

The first-in-first-out (FIFO) approach is a common method used by investors when they sell holdings. When you purchase a group of shares at a given price, they will constitute a ‘parcel’.

You may acquire shares in the same company in several different transactions over a period of time. Each transaction forms its own parcel of shares.

The concept of FIFO relates to the disposal of investments. When you are ready to sell shares, you can choose which parcels — sometimes called ‘lots’ — of shares you would like to sell.

Using the FIFO method, you would sell the parcels that have been held for the longest period. Provided that the share price has risen since the time of purchase, the FIFO method will ensure the greatest capital gain from the sale of a parcel of shares. Obviously, this won’t always be the case, and adopting a FIFO approach might not result in the greatest capital gain.

For example, if an investor purchased 100 shares in a company at $20 per share three years ago, and another 100 shares at $40 two years ago, they might choose to use the FIFO method when they choose to sell some of those shares.

Let’s say the company’s share price has now risen to $50. The investor sells using the FIFO method, disposing of the first 100 shares that were purchased at $20. Because the share price has grown $30 since they purchased them, they realize a gross profit of $3,000. However, if they had chosen to sell the more newly acquired shares parcel, they would only realize a gross profit of $1,000.

As mentioned, FIFO will only result in the largest capital gain if the share price has risen consistently over time. If share prices have dropped since you bought them, the FIFO approach might not result in the greatest capital gain — but it could lower your tax burden.

Strategy 2: Last-In-First-Out

In the above example, the investor opted to sell their more recently acquired shares because they wanted to maximise their capital gains. Because the share price rose over time, the FIFO approach achieved this goal.

LIFO works in the opposite manner to FIFO — your newest shares are sold first. The LIFO method ‘typically results in the lowest tax burden when stock prices have increased, because your newer shares had a higher cost and therefore, your taxable gains are less’.

If we continue to assume a consistent growth in share price, LIFO would be a useful strategy to dispose of assets and realize less capital gain from the disposal — and subsequently pay less tax.

However, don’t forget that you can only qualify for the CGT discount if you’ve held shares for longer than 12 months.

Investors have four main ways to calculate their portfolio’s capital gains.

FIFO and LIFO are based on shares being organized by time

The FIFO and LIFO approaches above assume that share prices have risen over time. When the opposite is the case, a smaller capital gain may be realized by selling the newly acquired shares or vice versa. The degree to which FIFO or LIFO suits your goals will depend on how the share price has behaved since you acquired the asset.

Some investors might opt for a more precise method of disposal such as maximum or minimum gain, to ensure that they dispose of the parcels which will return the greatest capital gain or result in the lowest tax burden.

Strategy 3: Maximum Gain

The FIFO and LIFO methods are based on selling assets based on the time at which you acquired them. One alternative approach is maximum gain, which is focused on the price at which shares were bought, rather than the time they were bought.

The suitability of FIFO or LIFO will depend on what has happened with the share price since you bought, and what your goal is. Maximum gain focuses on disposing of the assets that were acquired for the lowest price, rather than those which were acquired first or last. This approach is suitable for those looking to ensure maximum capital gains when they sell.

An example of the maximum gain approach: A prospective home buyer has found their dream home and needs to prove to their bank that they can service a large mortgage. They carefully select the shares that were bought at the lowest price in their portfolio to sell, so they can realize the maximum possible capital gain from the sale. While they will pay the most tax using this method, the capital gain will be the largest, and this will help paint a healthy financial picture to the bank.

But, you may want to minimize your CGT obligations.

Strategy 4: Minimum Gain

The minimum gain approach works in the opposite way to maximum gain — you select the parcels of shares in your portfolio that you acquired for the most expensive price and sell these first. By choosing to sell the tax lots with the highest cost base, you will minimize your gain.

This strategy is generally used by investors who want to minimize their CGT obligations. As we know, less capital gain = less tax paid.

Minimum and Maximum gain, as well as FIFO and LIFO approaches, will suit different investors depending on their requirements.

Regardless of what your aspirations are, and which approach you choose, it is important to make sure that your investment portfolio is kept in good order.

Record keeping is paramount in both portfolio management and personal finance — particularly as it concerns reporting your investment activity to the tax authorities.

The above strategies are probably best deployed when you have a clear understanding of your portfolio’s performance. It is important to keep an accurate record of your transaction history, including the dates and prices at which you bought particular shares. This knowledge is vital if you wish to select the most tax-efficient disposal strategy that you can. Or in some instances, simply if you want to maximise your capital gains.

The Navexa Portfolio Tracker automates this entire process, from tracking trades and transactions to optimizing how you report CGT on a portfolio.

Remember, Navexa doesn’t offer tax advice. We always encourage you to consult your accountant or seek other professional advice when it comes to investments and taxes.

The Navexa portfolio tracker’s portfolio overview.

Automate Your Portfolio Tax Reporting & Optimization With Navexa

Navexa is a platform for tracking your investment portfolio and displaying detailed information that will help you better understand your performance — and better handle investment tax reporting.

When it is time to prepare your tax return, you should have a clear vision of what you want to achieve. Whether you are looking to maximise your capital gains or minimize the impact of CGT, Navexa makes the process fast and stress-free.

Our CGT and the Taxable Income tools can help you determine your obligations and options when it is time to file your tax return.

Join thousands of Australian investors already using Navexa to manage their investment portfolios.

With Navexa you can:

Track your stocks and crypto investments together in one account.

Automatically track capital gains, portfolio income, currency gains and losses and trading fees.

Benchmark your long-term portfolio performance against any index you choose.

Automatically track your dividend and distribution income from stocks, ETFs, LICs and Mutual/Managed Funds

Use the Dividend Reinvestment Plan (DRPs/DRIPs) feature to track the impact of DRP transactions on your performance (and tax)

See the complete picture of your investment performance, including the impact of brokerage fees, dividends, and capital gains with Navexa’s annualized performance calculation methodology

Run powerful tax reports to calculate your dividend income with the Taxable Income Report

Calculate your CGT obligations with our Australian Capital Gains Tax Report and the Unrealised Capital Gains Tax Report

An introduction to some of the (legal) ways to optimize investment taxes in Australia.

Paying tax is part of investing. While you can’t avoid paying tax (at least, not legally), there are several ways in which you can reduce the impact of tax on your investment earnings.

This post explains the tax system in Australia as it relates to investment income, and introduces some strategies Australians use to minimize their investment taxes.

Different investment strategies have different tax obligations

Tax And Investing In Australia

The Australian Tax Office (ATO) requires individuals to declare investment activity in their tax return and pay tax on all investment earnings, including capital gains and dividend income.

If you buy shares, invest in property, or hold other investments and then sell them at a higher price, you will have made a capital gain.

The Capital Gains Tax (CGT) is the tax rate that is applied to net capital gains (total gains minus total losses).

How Does the Capital Gains Tax (CGT) Work?

The capital gains tax is not a set rate but is calculated according to an individual’s marginal tax rate. This is the tax rate for personal income, and will be the tax rate applied to investment earnings.

Capital gains are taxed at an individual’s marginal tax rate

Unlike CGT rates for individuals, flat CGT rates apply for companies and self-managed funds. Trading companies pay 26% if their annual turnover is less than $50 million. If it exceeds $50 million, the CGT applied is 30%. Investment companies don’t qualify for the 26% rate and are taxed at 30%. Self-managed super funds are taxed at a lower rate of 15%.

Getting back to individual taxation, if you sold any investments during a financial year, including shares, you will need to work out your capital gain or loss for each asset. CGT will need to be paid on your net capital gains. The Navexa platform provides a straightforward solution for making these calculations — more on that later.

Which Investments Does The CGT Apply To?

CGT applies to a wide range of investments, including property, shares, and cryptocurrency. When you sell an asset and realize a gain from that sale, you will be charged CGT.

In addition to owing CGT when you sell an asset, the tax also applies in other investment situations, or ‘CGT events’. A CGT event occurs when you make a capital gain or incur a capital loss.

Examples of other CGT events include switching shares in a managed fund between funds or owning shares in a company that is subject to a takeover or merger.

The ATO considers these dividends ‘franked’. A ‘franking credit’ is attached to the dividend and represents the tax that has already been paid by the company distributing the dividend. The shareholder who receives the dividend with an attached franking credit will either owe less than their usual tax rate, or receive a tax refund.

Tax And Cryptocurrency

Cryptocurrency investment is also subject to taxation in Australia. Cryptocurrency is taxed in a similar way to other investment assets.

The ATO classifies four main CGT events for crypto activity.

You’ll be taxed when you:

Sell cryptocurrency.

Exchange one crypto for another.

Convery crypto to fiat currency like AUD.

Pay for goods or services in crypto.

Just like when you pay CGT at your marginal tax rate when you sell shares, you owe this rate when you sell crypto.

Capital gains are taxed for cryptocurrency investments, too.

Now that we’ve discussed the basics of tax for Australian investors, let’s explore some of the strategies that investors use to minimize investment tax.

Effective Strategies to Minimize Tax Payments

There are several legal investment strategies investors employ to minimize tax bills and claim tax deduction. This goes for both gains and income.

Below you’ll find some of the ways Australian investors hold on to as much of their investment gains and income as possible.

The following is not investment advice. As with all the information on the Navexa blog, it’s general investment information our writers have collated from other sources. For any financial or investment decisions, you should always understand the risks and seek professional advice if necessary.

Strategy 1: Hold Onto Your Investments For Longer Than 12 Months

Australian tax law makes a distinction between short and long term capital gains. A long term capital gain is when you make a profit on an investment that you’ve held for longer than 12 months.It’s ashort term capital gain if you’ve held the asset for less than 12 months.

As an investor, this is important to understand, because of something known as the ‘CGT discount’.

If you’ve held an asset for longer than 12 months before a given ‘CGT event’ occurs, you may be able to claim a CGT discount of 50%. Remember, a ‘CGT event’ is the point at which you make a capital gain or loss on an asset.

Fifty percent is a significant discount. If you made $40,000 profit from investments that you’d held for less than 12 months, and your marginal tax rate was 37%, you’d have a $14,800 tax liability.

However, if you’d held for longer than 12 months, the CGT discount rules would mean your tax liability was just $7,400 — a much more ‘tax effective’ amount.

The CGT discount applies to crypto investments, too.

As you can see, holding onto your investments for longer than 12 months to take advantage of this tax discount can be much more tax effective.

Navexa provides a platform where you can easily track your asset performance and calculate your taxable gains. The CGT Reporting Tool gives a detailed breakdown of which assets are ‘non-discountable’ from a CGT perspective and reduces the amount of tedious leg-work at tax time.

Navexa’s tax reporting tools remove the need to manually calculate their portfolio tax obligations or the most tax effective way to prepare a tax return.

Provided the portfolio data in your account is correct and up-to-date, you can run an automated tax report in just a few seconds.

Navexa’s Capital Gains Tax Tool

Navexa’s CGT reporting tool

What you see above is Navexa’s CGT Report.

Navexa calculates your taxable gains and displays a detailed breakdown. Capital gains are displayed according to Short or Long Term status alongside your Capital Losses Available to Offset. The report also calculates your CGT Concession Amount and finally, your total Capital Gain.

Navexa’s CGT Reporting Tool makes it easy to categorize your investments for your tax return, while the Unrealized Capital Gains report can help show the most tax efficient way to dispose of investments.

Strategy 2: Lower Capital Gains With Capital Losses

Another useful tool for investors at tax time is their capital losses.

You make a capital loss when you sell an asset for less than what you paid for it. This loss can be deducted from your capital gains (from other sources) to reduce the amount of tax. If you don’t have any capital gains to deduct from, the capital loss can generally be carried forward to future financial years. If you make capital gains in future years, the capital losses are still up your sleeve to deduct from any gains and reduce tax.

For example, if an investor owed $4,000 in CGT for their investments in a financial year, but had declared losses of $1,500 the previous financial year, they could carry these losses over to offset their capital gain, resulting in a reduced tax bill of $2,500.

Strategy 3: Invest In Companies That Pay High Dividends And Franking Credits

We’ve already looked at how the ATO taxes dividends, so what does this mean for minimizing your income tax obligations?

For example, an investor with a 32.5% tax rate receives a $1,750 dividend with a $750 franking credit attached. The franking credit takes the taxable income to $2,500, with gross tax of $812.50 payable. The franking credit rebate of $750 is deducted from the gross tax and the investor is left to pay only $62.50 in tax, leaving them with $1,687.50 after tax income. For a full breakdown of this and other franked dividend scenarios, click here.

As you can see, the investor in the above situation manages to retain most of dividend income. Because the franking credit offsets their CGT so significantly, the amount of income tax the individual pays is greatly minimized.

Choosing to invest in companies that pay dividends, especially fully or highly franked dividends, is a popular strategy for minimizing tax paid on investment returns. Fully franked dividends are effectively tax free income.

Navexa can also help you accelerate the process of determining your taxable income. When you automate your portfolio tracking in Navexa, the Taxable Investment Income tool provides you with everything you need to know to prepare your tax return.

Navexa’s Taxable Income Tool

As you can see above, the Taxable Income Tool displays the Unfranked Amount and the Franked Amount for your dividends, as well as the total Franking Credits attached to them.

And in the below image, you can see the additional fields in the ‘Supplementary’ section. These display further tax-relevant information such as the amount of Franked Distributions From Trusts, the amount of Assessable Foreign Source Income, and your Foreign Income Tax Offset.

Fully franked dividends are like tax free investment income!

Below these fields, you’ll also be provided with a holding by holding breakdown of your taxable investment income, like this:

Navexa’s holding by holding investment income breakdown

This shows you subtotals for payments from each holding, and grand totals for each column at the bottom.

At the top right of the report, you’ll find buttons for exporting the report as both an XLS and PDF file.

This helps you accelerate the process of preparing your investment income for assessment.

Dispose Of Your Investments In A Tax-Efficient Way

When the time comes that you want to sell it can be easy to get excited about the potential gains you are about to realize. This excitement can be dampened, however, when you are faced with the reality of your tax bill.

Choosing a particular method to dispose of your investments can have a major impact on the profits you generate and the tax you pay on them.

First-In-First-Out (FIFO)

The first-in-first-out (FIFO) approach is a common method used by investors when they sell holdings. When you purchase a group of shares at a given price, they will constitute a ‘parcel’.

You may acquire shares in the same company in several different. Each transaction will form its own parcel of shares.

The concept of FIFO relates to the disposal of investments. When you are ready to sell shares, you can choose which parcels — sometimes called ‘lots’ — of shares you would like to sell. The FIFO method involves disposing of the parcels that have been held for the longest period. Provided that the share price has risen since the time of purchase, the FIFO method will ensure the greatest capital gain from the sale of a selection of shares.

For example, if an investor purchased 100 shares at $20 in a company three years ago, and another 100 shares at $40 in the company two years ago, they might choose to use the FIFO method when they choose to sell some of those shares.

Let’s say the company’s share price has now risen to $50. The investor opts to sell using the FIFO method, disposing of the first 100 shares which were purchased at $20. Because the share price has grown $30 since they purchased them, they realize a gross profit of $3,000. However, if they had chosen to sell the more newly acquired shares parcel, they would only realize a gross profit of $1,000. The FIFO method is therefore popular with investors looking to maximise capital gains when they sell. But what about tax?

Last-In-First-Out (LIFO)

In the above example, the investor opted not to sell their more recently acquired shares because they wanted to maximise their capital gains. But if you are looking to minimize the impact of tax, adopting the LIFO approach could be advantageous.

LIFO works in the opposite manner to FIFO — your newest shares are sold first. The LIFO method ‘typically results in the lowest tax burden when stock prices have increased, because your newer shares had a higher cost and therefore, your taxable gains are less’.

Because the investor has chosen to dispose of shares that were bought at a higher price, they realize a smaller capital gain — and subsequently pay a lower tax bill.

However, don’t forget that you can only qualify for the CGT discount if you’ve held the shares that you sell for over a year.

The FIFO and LIFO approaches discussed above assume that the share prices involved have risen over time. This won’t always be the case. If the price of an asset drops over time, a smaller capital gain may be realized by selling the newly acquired shares. Smaller capital gain = less tax.

In some instances, investors might choose to dispose of a particular lot or parcel that cost more than the current share price so they can realize a capital loss. This capital loss could be used to offset other capital gains.

Regardless of the approach you choose, it is important to keep good records and understand the tax implications of disposing of the various share parcels in your portfolio.

We hope you’ve enjoyed this quick guide to investment tax and some of the strategies investors use to help minimize their tax bill in Australia.

Navexa doesn’t offer tax advice, and we always encourage you consult your accountant or seek other professional advice when it comes to investments and taxes.

Navexa is a platform where you can easily track your investment portfolio and display detailed information that will help you at tax time.

Navexa empowers investors to build brighter financial futures with simple, but powerful, automated investment analytics and reporting tools.

Features such as the CGT Reporting Tool and the Taxable Investment Income Tool can help you determine your obligations and opportunities when the time comes to pay the tax man.

Our guide to what is — and is not — taxable for cryptocurrency investments in Australia. From basics like capital gains tax from selling crypto, to paying tax on crypto staking income, declaring capital losses and understanding how the ATO treats DeFi.

If you’re buying and selling cryptocurrencies in the hope the Australian Taxation Office either won’t know about, or won’t be able to tax, your profits and income, I have bad news:

Crypto’s ‘wild west’ days — at least in terms of mainstream adoption and regulation — are gone.

While you’ll find many a tweet about how ‘it’s not too late to be early’, it is, in fact, too late to slide into what was once a murky, misunderstood world of strange new digital currencies.

(As an aside, I first heard about Bitcoin from a friend of a friend on a tram in Melbourne around 2013. That was early.)

The markets have grown exponentially since Bitcoin’s inception.

Today, the Australian government, like many others around the world, has a greater grasp on the cryptocurrency markets and blockchain technology than ever.

As you’ll see in this guide to crypto tax in 2022, as the technology and markets for digital currencies and assets grows and becomes more complex, so do the tax laws surrounding them.

Now, more than ever, Australians investing in (or trading) the cryptocurrency markets need to prepare themselves to accurately track, report and declare their activity.

As the ATO states:

‘Everybody involved in acquiring or disposing of cryptocurrency needs to keep records in relation to their cryptocurrency transactions.’

This guide covers basic concepts around how the government in Australia treats digital currency for tax purposes, capital gains and taxable income, tax deductions and even tax-free digital asset transactions.

Plus, we’ll introduce some useful services and tools which may be helpful in tracking and reporting all the information the ATO requires when lodging crypto information at tax time.

Please bear in mind this article is neither tax nor financial advice. It is general information collated from credible sources, including the ATO.

Bitcoin, like other digital currencies, is subject to tax in Australia.

The ATO Knows About Your Cryptocurrency

As the crypto markets and the platforms people use to navigate them have grown in recent years, there’s been an increasing emphasis on ‘know your customer’, or KYC practices.

KYC is a way both for governments to impose regulation on crypto providers, and a way for crypto providers to communicate legitimacy — and distance themselves from the criminal activity which continues to plague the fast-evolving crypto space.

In Australia, this means you can’t register for a crypto exchange or wallet without providing documents and details that prove your identity (like your driver’s license or passport) and address.

The crypto providers, in turn, must provide details on their customers to the ATO, which began collecting details in 2019 to ensure Australians active in the crypto markets were complying with tax laws.

So if someone doesn’t declare their crypto activity, that doesn’t mean the Australian government won’t know about it. And, when someone does report it, the ATO can match what’s reported with what they have on file as a result of their data matching program protocol (the current version of which runs until 2023).

In other words, it’s probably not going to work out well for those who attempt to dodge declaring their crypto activity or paying tax on it — see here for more.

The ATO Can Legally Tax Australian Residents’ Crypto Activity

Australian tax law and the ATO have caught up to the crypto markets significantly in the past few years. As we mentioned, the wild west days are over. While Bitcoin survives, it’s now one of thousands of digital currencies.

Today, those investing in and trading ‘virtual currency’ need to accept taxation as a given, just as they would with traditional stocks and other assets.

As the crypto space continues to expand in bold new directions (while initial coin offerings were once crypto’s hottest topic, NFTs are the latest booming multi-billion dollar acronym), the tax regulation surrounding it grows ever more complicated.

Below, you’ll find introductions to many different tax scenarios surrounding various areas of the crypto markets (like DeFi and staking).

The basic premise though, is this: The ATO does not treat virtual currencies like currency at all. It’s not ‘money’ for tax purposes. They treat digital assets as property.

For the purposes of applying capital gains tax, or CGT, the ATO treats crypto like any other investment asset (like shares or property). In other cases, it will treat crypto as taxable income.

The ATO makes a distinction between two types of crypto activity.

The ATO can tax trading, staking, and other blockchain activities.

The Difference Between Investing In & Trading Cryptocurrency

As in the traditional investment markets, there’s a distinction between investing and trading in crypto, too. Some people buy some Bitcoin or Ethereum in the hope they’ll someday realize a huge profit.

Others will buy and sell frequently, perhaps even as their full-time job.

With crypto, the ATO makes this distinction between investors and traders.

How a person classifies their crypto activity has a significant impact on how they’ll be taxed on it in Australia.

You’re A Crypto Investor, If…

You are an individual buying crypto for the purpose of generating a future return. This means you buy and sell digital currencies as you would shares in a company, with the same goal — profiting from long-term capital gains as those assets rise in price.

Generally speaking, most Australians in the crypto space would be classed as investors by the ATO.

You’re A Crypto Trader, If…

You use crypto activity to make an income from a business. This includes short-term buying and selling, mining crypto, and operating an exchange, for example. Whatever proceeds you generate from your crypto business activities, the ATO treats as taxable income.

Obviously, given the ATO’s oversight on crypto activity in general, both of these use cases demand detailed record keeping, regardless of how seriously or casually one is active in the market.

The big difference from a tax perspective is that while investors can qualify for capital gains tax discounts (resulting from holding an investment longer than 12 months), traders cannot, since their crypto profits are classed as taxable income, not capital gains.

For the purposes of this explainer post, we’ll focus on crypto investing, not trading.

Which Crypto Activity Does The ATO Tax?

In short, everything. The ATO classifies four main CGT events for crypto activity.

You’ll be taxed when you:

Sell cryptocurrency (or gift it to someone).

Exchange one crypto for another.

Convert crypto to fiat currency like AUD.

Pay for good or services in crypto.

These are just the main taxable events the ATO looks at. We’ll get to the more complex scenarios shortly.

First, it’s worth noting that the ATO doesn’t consider a digital crypto wallet as an asset. Rather, it treats the individual crypto assets within a wallet as separate CGT asset (the same way that an investment portfolio is not taxable — the investments within it are).

There are some similarities between cryptocurrency taxation and traditional investment taxation.

Paying Tax On Crypto Capital Gains

Australians pay capital gains tax on their crypto investments at the same tax rate they pay on their personal income for the financial year.

So, for example, if someone earns $100,000 from their employment and makes a $20,000 profit from selling some Bitcoin and Ethereum, they’d held for less than 12 months, their capital gains tax rate would be 32.5%.

This means they would be taxed $6,500 on the capital gains they realized by selling their crypto.

It’s important to note that capital gains tax rates differ for individuals, companies and self-managed superannuation funds in Australia.

Australian tax law makes a distinction between long term and short term capital gains. This effectively incentivizes investors to hold investments for more than a year.

In the example above the investor has held their Bitcoin and Ethereum for fewer than 12 months before selling and realizing their capital gain.

This means they pay the same tax on their crypto gains as they do their personal income (for tax purposes, capital gains profits are added to other income to determine the tax rate).

But if they held the Bitcoin and Ethereum for more than 12 months, they’d qualify for a 50% CGT discount.

So, instead of paying $6,500 of their $20,000 capital gain, they’d only need to pay $3,250 — substantially less money.

Learn more about capital gains tax obligations in Australia here (ATO) and here (NAB).

Declaring Capital Losses On Crypto

Of course, people don’t always sell cryptocurrency for a capital gain. If someone bought 100 Solana at $100, got excited when it rose to $150, but then panicked when the coin dipped back to, say, $70, they might choose to sell to stop any potential further losses.

In that case, they’d be selling for $7,000 a crypto investment they paid $10,000 for in the first place — realizing a $3,000 capital loss.

Firstly, they don’t need to pay any tax on the $7,000 they received from selling the asset, since it represents a loss. Secondly, they can deduct that $3,000 loss from any other capital gains they might declare in the same — or a future — financial year.

Going back to the previous example, assuming someone needed to pay a $6,500 capital gains tax on their crypto profits, but had in the previous year realized a $3,000 loss, they could apply that loss in their current tax return, bringing the total payable CGT on their crypto down to $3,500.

Declaring a capital loss on crypto can allow an investor to offset gains they may have realized not just on other crypto, but on shares or property. They cannot, however, carry them over as a deduction on regular income.

Crypto-to-crypto trades are generally considered CGT events in Australia.

Paying Tax On Crypto-To-Crypto Transactions

The ATO doesn’t just view selling crypto for fiat currency (like AUD) as a CGT event. It also requires Australian investors report any crypto-to-crypto transactions for capital gains tax.

Remember, for tax purposes in Australia, every asset within a digital wallet is considered a separate CGT asset. So when people trade between different assets within a wallet or on an exchange, they need to track and record this like any other investment CGT event.

Since crypto is effectively property as far as the ATO is concerned, its value is based on a given currency’s market value at a given time.

Here’s an example to illustrate crypto-to-crypto tax in action:

Crypto-Crypto CGT Example

An investor trades some ETH for some SOL.

Say they bought $2,000 worth of ETH. Over three years, their $2,000 investment rises to $6,000.

Then, they trade it for $6,000 worth of SOL. By doing so, they realize a capital gain of $4,000, because they’re effectively ‘selling’ out of their ETH investment. It’s just that they’re realizing their gain in SOL, as opposed to AUD.

So while they don’t convert any crypto back into AUD, they still need to declare this trade as a CGT event when they file their tax return.

Similarly, had their ETH investment fallen by 50% to $1,000, and they’d traded that for SOL, they’d be able to declare a capital loss of $1,000.

Transferring crypto between different digital wallets is not a taxable event in Australia, since people don’t realize a capital gain by doing so.

Staking = taxable income

Crypto Staking Rewards = Taxable Income

Crypto ‘staking’ is a blockchain mechanism whereby holders of particular cryptocurrencies can contribute to the coin’s blockchain by making their coins available to help validate transactions.

If that’s too complex, don’t worry. The simpler way to think of crypto staking is like a savings account that pays interest.

When you stake crypto, you earn more of that crypto back as a percentage of the amount you choose to stake on its blockchain.

For example, say I have 100 SOL worth $10,000 ($100 each) and I choose to stake it at a rate of 7% per annum. Nine months later, I ‘unstake’ my SOL and receive an extra 5.25 SOL in staking rewards.

Let’s say in the nine months I staked my SOL, the value rose 50%.

So when I receive my new 5.25 SOL, they’re worth $787.50 — the market value at the time I receive them.

How To Treat Staking Rewards For Tax Purposes

Unlike the other transactions we’ve looked at so far in this post, the ATO considers staking rewards as ordinary taxable income.

This is different from a capital gain. In this case, the $787.50 gets added to my regular income (like my salary, for example) and taxed at the appropriate personal tax rate.

In other words, it’s taxed like interest I might earn from keeping money in a savings account.

But, were I to sell the extra SOL I earned by staking my initial investment, I would have to pay capital gains tax on that — although the base price would be the market value at the time I received it, not the price I paid for the initial investment.

Crypto Tax On Decentralized Finance (DeFi)

Decentralized Finance, or DeFi, is one area of crypto where Australian tax policy is seemingly still playing catchup.

DeFi is, in basic terms, is the finance marketplace on the blockchain. As the name suggests, this is finance without centralization — or intermediaries like banks, finance brokers or credit card companies.

DeFi protocols allows people to lend and borrow capital through blockchain-based peer-to-peer financial networks.

While you could argue DeFi is still in its infancy, reports suggest there is already nearly $1 trillion ‘locked’ into DeFi protocols such as Aave (AAVE), Solana (SOL) and Uniswap (UNI).

At this stage, while the ATO doesn’t have any specific guidance as yet, this doesn’t mean that DeFi activity can’t be taxed.

If someone uses a DeFi protocol to earn crypto, chances are the ATO would consider this taxable income. And like crypto staking, if they sold or traded any crypto earned through DeFi, this would trigger a CGT event.

This excellent guide details the possible tax implications of various DeFi actions.

Crypto investors are entitled to certain tax breaks in Australia.

Tax Breaks For Australian Crypto Investors

It’s not all tax obligations when it comes to crypto activity for Australian investors.

As with traditional investments, there are three main ways the ATO offers tax relief.

The first is the standard personal income tax break on the first $18,200 of personal income. While it’s probably unlikely someone in the crypto markets would make less than that in a financial year, it is, technically possible to pay no tax on crypto gains in this respect.

Second, the 50% capital gains tax discount is not to be underestimated. If someone realized $100,000 in gains on crypto they held less than 12 months, and that gain is taxed at the highest rate (45%), they’ll net just $55,000.

But, if they tactically hodl longer than 12 months before realizing the gain, that $45,000 tax bill comes down to $22,500 — meaning they keep $77,500. This is a significant financial difference when you consider that the difference between ‘less than’ and ‘more than’ 12 months is a single day.

The third way Australians can qualify for a crypto tax break is through personal use. The window for claiming crypto activity as personal use is quite small. Basically, if someone buys up to $10,000 worth of crypto and then immediately buys something else with it, they can claim personal use (as opposed to investing for a future gain).

As with everything when it comes to crypto tax, it’s always important to closely track and record every transaction. The burden of proof is on investors to produce the records required to prove what they claim in their tax return.

Tax-Free Crypto Transactions? They Exist!

Not only are there tax breaks available to those investing in crypto in Australia — there’s even a list of crypto transactions that trigger no tax events.

These are, of course, transactions in which the person probably won’t make a significant profit.

Australian investors won’t pay crypto tax when they:

Buy cryptocurrency

Receive cryptocurrency as a gift

Give cryptocurrency as a charity donation

Hold cryptocurrency (even if it goes up 10,000%)

Receive cryptocurrency from ‘hobby’ mining

Move cryptocurrency between digital wallets

Buy goods and services up to the value of $10,000 using cryptocurrency (see the personal use scenario above)

Where To Find Tools & More Information About Crypto Tax In Australia

It might seem difficult to understand the nuances of crypto tax law in Australia. But the reality is that for the average crypto investor —someone who buys and sells crypto with the objective of making some money — it should be pretty straightforward.

By and large, you could apply the same tax rules to your crypto portfolio as you would for investments in stocks.

If you sell an investment for a capital gain, you’ll need to pay a capital gains tax.

If you make money from an investment, you’ll need to declare it as income and pay tax at the marginal rate applied to your total income for the financial year.

But, as you’ve seen in this post, things can quickly grow more complex the deeper you get into the crypto markets.

Here at Navexa we’re proponents of continuously searching for and acquiring financial literacy.

Here are some resources we consulted in putting this guide together that may help you with your own crypto investing and tax reporting:

As always, seek professional advice and support when considering investing and its tax implications!

Navexa helps speed up the crypto tax reporting process

Navexa: Automated Tracking For Crypto Capital Gains & Income

If you’re investing in cryptocurrencies and you’d prefer a quick, automated way of not only tracking your portfolio performance and returns, but also of generating comprehensive, accurate tax reports, try Navexa.

We’ve developed Navexa to give investors radical insight into how their portfolio performs over time.

Not only does the platform break down your total return by capital gains and dividend income, it calculates the impact of trading fees on your portfolio performance.

As you may already know, trading fees can have a massive impact on crypto transactions. The Ethereum blockchain has been notorious in recent years for slapping users with transaction fees which often outweigh the value of the coins being transacted.

If you don’t consistently and accurately track the impact of fees on your crypto investments, you may end up with a distorted picture of how they’re performing.

Proper tracking is also a requirement if you find you need to provide detailed information to the ATO regarding your tax return. As we outlined above, you need to be able to show the fine details of transactions to substantiate capital gains, losses and income that you’re claiming in a tax return.

While you can pull this information together using data from exchanges and wallets, Navexa allows you to consolidate your crypto portfolio data even if you trade across multiple platforms.

Remember the 50% capital gains discount the ATO offers on crypto investments held longer than 12 months? If you’re filing a tax return containing 100 trades off various sizes across 100 different dates within the financial year, calculating which qualify for the CGT discount could quickly become a headache.

With Navexa’s tax reporting tools, this calculation is completely automated — your account gives you a detailed breakdown of which holdings qualify and which do not in a single click (so long as all your portfolio data is accurate and up to date!).

We’ve built (and are constantly) developing Navexa’s analytics and reporting tools to empower investors in stocks and crypto to get powerful insights into their portfolio performance and make calculating and reporting tax details fast and easy.

If you invest in Australia, the Australian Taxation Office requires you pay tax on both capital gains and dividend income. Here are some basic things to know about paying tax on your investments in Australia.

Paying a portion of our income to our government has long been a fact of life — the phrase ‘certain as death and taxes’ stretches back more than 300 years.

In Australia as elsewhere, this goes for income we earn from employment, a rental property, and other sources. It also applies to investment income.

Below, you’ll find information (general, of course, and not in any way to be considered financial or taxation advice!) about:

The Australian tax year and cycle.

Capital gains tax (CGT) events for investments (long and short term).

Taxable investment income from dividends.

Different ways you can report on your investments for tax purposes.

Tax benefits from ‘franked’ dividends.

Let’s start by explaining the Australian tax cycle.

Tax Time: Key Australian Dates

These are the key dates to keep in mind for calculating your portfolio tax and filing your tax return in Australia.

The income year for tax purposes — otherwise known as the ‘financial year’ — goes from July 1 to June 30.

This is the period for which you’ll need to collect and collate your financial information for assessment during the period known as ‘tax season’.

Australian Tax Season

Tax season runs from the start of the next financial year (July 1) to October 31 — a period of four months.

If you’re lodging your own tax return, you have until October 31 to do so. If you use a registered tax agent, you have a little longer — usually May 15 the following year.

Check with your accountant or the Australian Taxation Office (ATO) to ensure the key dates for your specific situation.

If you’re an investor, you’ll need to report on your portfolio’s activities during the relevant financial year. Here are the main things you’ll need to consider as an individual.

Capital Gains Tax On Investments In Australia

Australian tax law specifies that you must pay tax on any assets you own when you sell them, or when another ‘CGT event’ happens to them.

At its most basic, this refers to selling shares. But it covers many other events, too, including switching shares in a managed fund between funds and owning shares in a company which another company takes over (or merges with).

What Is The Capital Gains Tax Rate?

Australians pay CGT on their investments at the same marginal tax rate they pay on their personal income for the financial year.

So, for example, if someone earned $100,000 from their employment and also made $20,000 from selling shares they’d held for more than 12 months, their marginal tax rate would be 32.5% — meaning they would need to pay $6,500 in tax on the capital gains from their investments.

The CGT rate differs for individuals, companies and self-managed superannuation funds.

If someone sell some shares for a capital loss, this may result in tax benefits, since they can deduct that loss from any gains they may have realized on other assets. If they didn’t make any capital gains (only losses) in a given financial year, they can carry a capital loss over to other financial years!

Long Term & Short Term Capital Gains

Australian tax law makes a distinction between long term and short term capital gains. This is effectively an incentive for investors to hold investments for more than a year at a time.

In the example above, where someone makes a combined $120,000 in the financial year from their employment and selling some shares, they’ve held those shares for less than 12 months.

This means they pay the same tax on their investment profits as they do their personal income (for tax purposes, capital gain profit gets added to other income to determine the marginal tax rate).

But if that person held the shares for more than 12 months, they’d qualify for a 50% CGT discount. Instead of paying $6,500 of their $20,000 capital gain, they’d only need to pay $3,250.

How To Calculate Your Portfolio’s Capital Gains Tax Obligations In Seconds

Bearing in mind we’re only talking about the capital gain side of portfolio tax, it’s easy to understand why so many of us don’t exactly look forward to tax time.

Navexa’s tax reporting tools are powerful ways to remove the need for someone to have to manually calculate — or pay someone to manually calculate — their portfolio tax obligations.

Navexa’s CGT Reporting Tool

Navexa’s Capital Gains Tax Tool

What you see above is Navexa’s CGT Report.

Once you track your investment portfolio in a Navexa account, you can access a suite of analytics about everything from individual holding performance through to portfolio contributions, and of course tax analysis.

Provided the portfolio data in your account is correct and up to date, you can run an automated tax report in literally a few seconds.

The CGT Report Breakdown

As you can see in the sample image above, Navexa calculates your taxable capital gain and displays a detailed breakdown.

Under ‘Non Discountable Capital Gains’ you have:

Short Term Gains: The capital gains you’ve made on assets sold within 12 months of buying them.

Capital losses available to offset: Any capital loss you’ve realized by selling assets for less than you paid for them.

Under ‘Discountable Capital Gains’ you have:

Long Term gains: The capital gains you’ve made on assets sold after holding them for 12 months or more.

Capital losses available to offset: Any losses realized from assets you’ve sold after holding longer than 12 months.

Then you have your CGT Concession Amount and, finally, your total Capital Gain for the portfolio (for the financial year and tax settings you’ve selected).

It’s important to note that Navexa doesn’t provide tax advice. But as long as your account information is accurate and up to date, this should be all you need to file your return.

At the top right of the report, you’ll find buttons for exporting the report as both an XLS and PDF file.

So now you understand the basics of capital gains tax for investments.

Let’s dive into the income side of the portfolio tax equation.

Intelligent Portfolio Performance Tracking

Track Australian & US trades, cryptos, cash accounts, currency gain, dividend income and more with the Navexa Portfolio Tracker.

Capital gains isn’t the only form of investment income people pay tax on in Australia. Just like income from a rental property, dividends count, too. You must declare investment income.