Investing in stocks is a popular way to build wealth. However, navigating the tax implications associated with stock investments can be daunting.

This guide explains the key tax implications associated with stock investments in Australia.

Why Understanding Investment Taxes is Crucial

Taxes on investments can significantly impact overall returns.

Knowing the specific tax obligations and benefits can help with planning an investment strategy more effectively.

In Australia, the two main types of taxes that affect stock investors are capital gains tax (CGT) and investment income tax (dividends, distributions etc). Each of these has its own set of rules and considerations.

Capital Gains Tax (CGT)

Capital Gains Tax is calculated on the profit you make when you sell a stock for more than you paid for it.

Understanding how CGT works can help you plan the timing of your sales and take advantage of potential concessions, such as the CGT discount for long-term holdings.

Taxes: Unavoidable, but not as rigid as many presume

Taxes are an inevitable part of investing, but with the right knowledge and strategies, you can optimize your tax outcomes and your investment returns.

Our series of posts on Australian investment taxes for stocks gives you a all the key information and insights you need to navigate calculating and reporting tax as an investor.

Navexa Portfolio Tracker: Automatically Track All Investments & Sort Your Tax Reporting In Minutes

You don’t need to worry about manually tracking your investment’s gains, income, and long-term returns.

The Navexa Portfolio Tracker automatically handles performance tracking and tax reporting for Australian investors.

Take a free 14-day trial and see for yourself why thousands of investors trust Navexa to track their portfolio and sort their investment taxes the easy way.

Investing in stocks not only offers the potential for capital gains, but can also provide ongoing income in the form of dividends and distributions.

However, like all income, these earnings are subject to taxation.

Understanding the tax implications of your investment income is essential for maximizing your returns and ensuring compliance with Australian tax laws.

This article gives you an overview of investment income tax, focusing on two primary sources; dividends from ordinary stocks, and ETF distributions.

Dividends from Ordinary Stocks

What Are Dividends?

Dividends are payments made by a company to its shareholders, typically derived from the company’s profits.

They represent a share of the earnings and can be a reliable source of income for investors.

How Are Dividends Taxed?

In Australia, dividends are considered taxable income.

They are usually paid out in two forms: franked and unfranked.

Franked dividends come with franking credits, which are tax credits that can offset the tax paid by the company on its profits.

These credits can significantly reduce your tax liability.

Conversely, unfranked dividends do not come with these credits and are fully taxable at your marginal tax rate.

Key Considerations for Dividend Income

Franking Credits: Understanding how to utilize franking credits can reduce your tax bill.

Dividend Reinvestment Plans (DRPs): Some companies offer DRPs, allowing you to reinvest your dividends to purchase more shares, which can impact your tax situation.

Holding Period Rule: To claim the franking credits, you must hold the shares ‘at risk’ for at least 45 days.

ETF Distributions

What Are ETF Distributions?

Exchange-Traded Funds (ETFs) are investment funds traded on stock exchanges, similarly to stocks.

They pool together capital from many investors to invest in a diversified portfolio of assets.

ETFs distribute their income, which can include dividends, interest, and capital gains, to their investors.

Tax Components of ETF Distributions

ETF distributions are more complex than ordinary stock dividends because they can include various tax components, each with its own tax implications.

These components can include:

Dividends: Similar to dividends from ordinary stocks, they may be franked or unfranked.

Interest Income: Taxed at your marginal tax rate.

Capital Gains: Distributed capital gains are subject to CGT.

Foreign Income: May come with foreign tax credits that can offset Australian tax.

Non-Assessable Amounts: Such as return of capital, which can adjust the cost base of your ETF holdings.

Key Considerations for ETF Distributions

Annual Tax Statements: ETFs provide detailed tax statements, breaking down the various components of the distributions, which are crucial for accurate tax reporting.

Foreign Tax Credits: If the ETF invests in international assets, you may be entitled to foreign tax credits.

Tax Deferral Strategies: Understanding how to defer taxes on certain components of ETF distributions can enhance your tax efficiency.

Conclusion

Investment income from dividends and ETF distributions is an important part of a portfolio’s overall returns. But, it’s essential to understand the associated tax implications.

By being informed and strategic about your investment income, you can optimize your tax outcomes and potentially boost your net returns.

Stay tuned for our in-depth articles on dividends from ordinary stocks and ETF distributions, where we will explore each topic in greater detail and provide practical tips for managing your investment income taxes effectively.

Navexa Portfolio Tracker: Automatically Track All Your Dividends & Portfolio Income

You don’t need to worry about manually tracking your investment’s gains, income, and long-term returns.

The Navexa Portfolio Tracker automatically handles performance tracking and tax reporting for Australian investors.

Take a free 14-day trial and see for yourself why thousands of investors trust Navexa to track their portfolio and sort their investment taxes the easy way.

If you invest in stocks, understanding the tax implications is crucial for optimizing your returns.

One of the most significant taxes you’ll encounter is the Capital Gains Tax (CGT).

This tax is applied to the profit you make when you sell your stocks for more than what you paid for them.

This article breaks down the basics of CGT, its importance, and introduces you to some powerful strategies for effectively managing and optimizing your CGT obligations.

What is Capital Gains Tax?

Capital Gains Tax is a tax on the profit realized from the sale of an asset.

For stock investors, this means any gain from selling shares is subject to CGT.

The amount of tax you owe depends on several factors, including the duration for which you held the stocks, your overall income, and any applicable discounts or exemptions.

Why CGT Matters

Properly managing your CGT can make a significant difference in your overall investment returns.

By understanding how CGT works and employing effective strategies, you can legally minimize your tax liability, and maximize your profits.

Whether you’re a seasoned investor or just starting out, having a solid grasp of CGT is essential for making informed investment decisions.

Key Strategies for Managing CGT

There are several strategies you can use to manage your CGT liabilities.

Each strategy has its advantages and can be suited to different investment goals and circumstances.

These are the four primary CGT strategies:

1. FIFO (First In, First Out)

FIFO is a method where the oldest shares are sold first. This strategy can be beneficial in certain market conditions.

Sometimes, the goal is to reduce the taxable gain. This strategy involves carefully selecting which shares to sell based on their cost base and current market value.

Understanding and managing Capital Gains Tax is a critical aspect of successful investing in stocks.

By leveraging the right strategies, you can significantly impact your investment outcomes.

Navexa Portfolio Tracker: Automate all your CGT calculation & strategies

Understanding CGT is one thing, putting it into practice is another.

The Navexa Portfolio Tracker makes the whole process really simple.

In just a few clicks you can calculate all of your CGT for a given financial year and toggle between strategies in an instant.

Then, in years to come, all your records are there for you to refer back to.

You can literally calculate your investment taxes the most optimal way in seconds.

Take a free 14-day trial and see for yourself why thousands of investors trust Navexa to track their portfolio and sort their investment taxes the easy way.

The FIFO strategy is the most common way of calculating capital gains. It is often the default method used by accountants and people reporting their own taxes.

The strategy is simple. When calculating the capital gain, you process trades in order of the date you bought them.

The first share parcel bought = the first one out.

Let’s look at an example of FIFO:

Purchases:

Buy 10 shares at $1 each — Total cost: $10

Buy 10 shares at $5 each — Total cost: $50

Sale:

Sell 10 shares at $4 each — Total sale value: $40

FIFO Calculation:

First parcel: 10 shares at $1 each — Total cost: $10

Sold 10 shares for $40

Capital Gain:

Gain: $40 (sale value) -— $10 (cost) = $30

Since this is a capital gain, it is subject to capital gains tax.

A more complex FIFO example.

Suppose we buy the following parcels in company ABC:

Buy 10 shares at $2 each — Total: $20

Buy 5 shares at $5 each — Total: $25

Buy 10 shares at $3 each — Total: $30

This gives us a total of 25 shares at different price points.

Now, let’s sell 13 shares at $4 per share using the FIFO (First-In-First-Out) method.

First Parcel (a):

10 shares at $2 each.

Total cost: $20

Sale value: 10 shares x $4 = $40

Gain: $40 — $20 = $20

Second Parcel (b):

Remaining 3 shares to be sold.

Next parcel: 5 shares at $5 each.

Cost for 3 shares: 3 shares x $5 = $15

Sale value: 3 shares x $4 = $12

Loss: $12 — $15 = -$3

Total Capital Gain:

Gain from first parcel: $20

Loss from second parcel: -$3

Total gain: $20 — $3 = $17

Therefore, the total capital gain from selling 13 shares is $17.

Navexa Portfolio Tracker: Automate Your CGT Strategy For Tax Reporting

You don’t need to worry about manually tracking your investment’s gains, income, and long-term returns.

The Navexa Portfolio Tracker automatically handles performance tracking and tax reporting for Australian investors.

Take a free 14-day trial and see for yourself why thousands of investors trust Navexa to track their portfolio and sort their investment taxes the easy way.

The Minimize Gain strategy is a way of calculating capital gains. It is used when people are trying to minimize their capital gain.

The strategy is simple. When calculating the capital gain, you process trades in order ofthe price you bought them for, with the highest price parcel coming first.

Let’s look at an example of Minimize Gain:

Purchases:

Buy 10 shares at $1 each — Total cost: $10

Buy 10 shares at $5 each — Total cost: $50

Sale:

Sell 10 shares at $4 each — Total sale value: $40

Minimize Gain Calculation:

Highest price parcel: 10 shares at $5 each — Total cost: $50

Sold 10 shares for $40

Capital Gain:

Gain: $40 (sale value) — $50 (cost) = $-10

Since this results in a capital loss, it is not subject to capital gains tax.

This loss can then be used to offset other capital gains, or be carried forward to future financial years.

A more complex Minimize Gain example

Suppose we buy the following parcels:

Buy 10 shares at $2 each — Total: $20

Buy 5 shares at $5 each — Total: $25

Buy 10 shares at $3 each -— Total: $30

This gives us a total of 25 shares at different price points.

Now, let’s sell 13 shares at $4 per share using the Minimize Gain method.

First Parcel (a):

5 shares at $5 each.

Total cost: $25

Sale value: 5 shares x $4 = $20

Gain: $20 — $25 = $-5

Second Parcel (b):

Remaining 8 shares to be sold.

Next parcel: 10 shares at $3 each.

Cost for 8 shares: 8 shares x $3 = $24

Sale value: 8 shares x $4 = $32

Loss: $32 — $24 = $8

Total Capital Gain:

Loss from first parcel: $-5

Gain from second parcel: $8

Total gain: $8 – $5 = $3

Therefore, the total capital gain from selling 13 shares is $3.

Navexa Portfolio Tracker: Automate Your CGT Strategy For Tax Reporting

You don’t need to worry about manually tracking your investment’s gains, income, and long-term returns.

The Navexa Portfolio Tracker automatically handles performance tracking and tax reporting for Australian investors.

Take a free 14-day trial and see for yourself why thousands of investors trust Navexa to track their portfolio and sort their investment taxes the easy way.

The LIFO strategy is a way of calculating capital gains. It is used when people are trying to minimize their capital gain.

This is because, usually, the last shares you bought will have a price that is closest to what you are selling them for.

The strategy is simple, when calculating the capital gain, you process trades in order of most recent purchases.

The last trade purchased = the first one out.

Let’s look at an example of LIFO:

Purchases:

Buy 10 shares at $1 each — Total cost: $10

Buy 10 shares at $5 each — Total cost: $50

Sale:

Sell 10 shares at $4 each — Total sale value: $40

LIFO Calculation:

Last parcel: 10 shares at $5 each — Total cost: $50

Sold 10 shares for $40

Capital Gain:

Gain: $40 (sale value) — $50 (cost) = $-10

Since this results a capital loss, it is not subject to capital gains tax.

This loss can then be used to offset other capital gains or be carried forward to future financial years.

A more complex LIFO example.

Suppose we buy the following parcels in company ABC:

Buy 10 shares at $2 each — Total: $20

Buy 5 shares at $5 each — Total: $25

Buy 10 shares at $3 each — Total: $30

This gives us a total of 25 shares at different price points.

Now, let’s sell 13 shares at $4 per share using the LIFO (Last-In-First-Out) method.

First Parcel (a):

10 shares at $3 each.

Total cost: $30

Sale value: 10 shares x $4 = $40

Gain: $40 — $30 = $10

Second Parcel (b):

Remaining 3 shares to be sold.

Next parcel: 5 shares at $5 each.

Cost for 3 shares: 3 shares x $5 = $15

Sale value: 3 shares x $4 = $12

Loss: $12 — $15 = -$3

Total Capital Gain:

Gain from first parcel: $10

Loss from second parcel: -$3

Total gain: $10 – $3 = $7

Therefore, the total capital gain from selling 13 shares is $7.

Navexa Portfolio Tracker: Automate Your CGT Strategy For Tax Reporting

You don’t need to worry about manually tracking your investment’s gains, income, and long-term returns.

The Navexa Portfolio Tracker automatically handles performance tracking and tax reporting for Australian investors.

Take a free 14-day trial and see for yourself why thousands of investors trust Navexa to track their portfolio and sort their investment taxes the easy way.

The Maximize Gain strategy is a method of calculating capital gains. It is used when investors are trying to maximize their capital gain.

The strategy is simple. When calculating the capital gain, you process trades in order of the price you bought them for, with the lowest price parcel coming first.

An example of Maximize Gain:

Purchases:

Buy 10 shares at $1 each — Total cost: $10

Buy 10 shares at $5 each — Total cost: $50

Sale:

Sell 10 shares at $4 each — Total sale value: $40

Maximize Gain Calculation:

Lowest price parcel: 10 shares at $1 each — Total cost: $10

Sold 10 shares for $40

Capital Gain:

Gain: $40 (sale value) — $10 (cost) = $30

A more complex Maximize Gain example.

Suppose we buy the following parcels:

Buy 10 shares at $2 each — Total: $20

Buy 5 shares at $5 each — Total: $25

Buy 10 shares at $3 each — Total: $30

This gives us a total of 25 shares at different price points.

Now, let’s sell 13 shares at $4 per share using the Maximize Gain method.

First Parcel (a):

10 shares at $2 each.

Total cost: $20

Sale value: 10 shares x $4 = $40

Gain: $40 — $20 = $20

Second Parcel (b):

Remaining 3 shares to be sold.

Next parcel: 10 shares at $3 each.

Cost for 3 shares: 3 shares x $3 = $9

Sale value: 3 shares x $4 = $12

Loss: $12 — $9 = $3

Total Capital Gain:

Gain from first parcel: $20

Gain from second parcel: $3

Total gain: $20 + $3 = $23

Therefore, the total capital gain from selling 13 shares is $23.

Navexa Portfolio Tracker: Automate Your CGT Strategy For Tax Reporting

You don’t need to worry about manually tracking your investment’s gains, income, and long-term returns.

The Navexa Portfolio Tracker automatically handles performance tracking and tax reporting for Australian investors.

Take a free 14-day trial and see for yourself why thousands of investors trust Navexa to track their portfolio and sort their investment taxes the easy way.

Foreign investment taxes can be complex. Generally, investors will pay capital gains tax or income tax, depending on the conditions. Here’s how to deal with Australian taxation on foreign investments.

Many Australians want to know how and where to invest in foreign stocks, property, bonds and other investments. This means they need to understand the tax implications of doing so. Australian taxation rules might seem complex when it comes to investing in foreign stocks.

The Australian government has signed many tax treaties. These provide benefits to Australian residents who invest in foreign stocks in countries that have tax treaties with Australia. Such treaties sometimes mean Australian residents may be exempt from paying tax. However, they may have to pay it in the foreign country.

If there’s no tax treaty, Australian residents may have to pay tax on every type of investment gain. Some might be eligible for a discount, depending on how long they have held the investment.

Generally speaking, foreign investments are taxable, be it in the source country or Australia. If you’re an investor, you’ll most likely pay capital gains tax or income tax. Keep reading to learn about Australian tax on foreign investments and how easy it is to track them using the Navexa portfolio tracker.

Overseas Investing From Australia

Australian residents are free to invest in foreign assets. They can own overseas property, offshore bank accounts, businesses, and stocks. Owning foreign investments requires that Australians comply with the latest rules and regulations regarding tax.

Australians can invest overseas, but need to understand their domestic and foreign tax obligations.

Interacting with the Australian Tax System

Every Australian resident is subject to tax on their income. This includes investment income such as dividends as well as capital gains from foreign investments. However, the Australian government has signed more than 40 tax treaties with other countries, including the US.

The US-Australia tax treaty gives Australian investors certain benefits. For example, there’s a reduced tax rate for US-sourced income (dividend payments) if certain conditions occur. Investors can also fill out specific forms that drop the rate of withheld tax from 30% to 15%. But, they may have to pay taxes in the US.

Australian investors might be able to claim US withholding tax from their dividends as a Foreign Income Tax Offset (FITO). FITO helps reduce taxes on foreign earnings.

But FITO rules are complex. It may be useful to seek professional guidance around this. Both the Inland Revenue Service (IRS) and US tax advisors can provide in-depth information for individual situations.

W-8BEN-E: A Key Form For Foreign Investors

The US government requires Australian investors fill out certain forms when investing in the country. A W-8BEN-E is a common form. It determines which investors are subject to paying 30% of their gross income earned in the US to the IRS. This form defines:

Interest

Royalties

Annuities

Rent

Premiums

Compensation for services

Substitute payments, if applicable

It’s required for all US holdings and remains valid for three years. If your information changes, you’ll be required to submit an update.

Australian residents for tax purposes have to declare all worldwide income.

Do Australian Residents Pay Tax on Gains and Income from Foreign Investments?

Australian residents for tax purposes have to declare the income they earn regardless of where that income came from. This is called the ‘worldwide income’ and it includes:

Pensions

Annuities

Business activities

Employment

Assets

Investments

Dividends from shares

Capital gains on overseas assets

Interest from bank deposits or bonds

Rental income from real estates

Royalties from intellectual property

If you have a temporary resident visa, you won’t pay tax on income. In case you receive income from a country that hasn’t signed a tax treaty with Australia, you’ll likely pay taxes in both countries. However, the tax you pay in a foreign country may make you eligible for FITO.

Australia also receives and exchanges information on all financial accounts with many foreign tax authorities.

How Is Foreign Investment Taxed?

Australian investors who have foreign assets and receive income from overseas will usually have to pay capital gains tax once they sell that asset. However, there could be other forms of taxes they are required to file (such as income from dividends). This is why it’s important to keep all the records on transactions, regardless of the country in which you invest.

Here’s where Navexa makes life easier. Our smart portfolio tracker lets you track foreign investments in both their local currency, and your tax residency’s currency, too.

This makes it super simple to monitor the performance of your foreign shares and keep records of all transactions for tax and compliance purposes.

The way dividends are taxed depends on the tax treaty between Australia and the source country.

Types of Investments and Their Taxation

Australian investors have access to several investment opportunities abroad. These are the most common ones.

Buying & Selling Stocks

Australians can own foreign stocks. Any individual who holds shares for more than 12 months may be eligible for the CGT discount. If they make a gain when they sell, Australian investors are required to notify the Australian Taxation Office. Investors are also advised to consult with the foreign tax authority to check the taxation process on capital gains.

Receiving Dividends From Foreign Investments

The way dividends are taxed depends on the tax treaty between Australia and the source country. In many cases, the source-country dividend tax is limited to 15%. Receiving dividends from companies that satisfy certain public listing requirements may result in tax exemption.

Depending on the conditions, some investors may be eligible for ‘franking credits’. That’s a form of tax credit that can offset against tax on dividends. Generally speaking, those who hold shares for a certain holding period (45 or 90 days) may be eligible.

Cryptocurrencies

In recent years, cryptocurrencies have become a major investment theme for Australian residents. When it comes to paying tax, Australian investors have to pay capital gains tax on crypto. On the other hand, professional traders pay income tax.

P2P Lending

Peer-to-peer (P2P) lending is a form of investment that’s accessible globally. Australians can access P2P lending platforms and lend money to borrowers without an intermediary. Peer-to-peer lending income listed in an investor’s loan portfolio will be included in the tax return form. For most people, this income is taxed like income from other investments. Australians who earn via P2P lending in foreign countries should consult their accountant.

Property Income

Australians who realize a gain when they sell foreign property are required to pay capital gains tax. However, if they held the property for 12 months or longer, they might be eligible for a 50% capital gains tax discount.

Additionally, investors who are subject to an overseas tax after selling their property will receive tax credits in the form of a foreign tax offset. Rental income may also be taxable in Australia or a foreign country, depending on the location of the property and current tax treaties.

Purchasing Bonds

Bonds can be highly tax efficient, since there are some benefits for those who hold them for 10 years. Otherwise, bonds are subject to the corporate tax rate of 30%. Investing in bonds means investors might not be eligible for tax credits and some other benefits.

Foreign Investment Capital Losses

Investors may sell a foreign investment for a lower price, and end up with a capital loss. In some cases, investors can use capital losses to reduce capital gains tax. Capital losses must be used at the first opportunity, unless there are restrictions. Capital losses can’t be used to reduce income, and should be reported to ATO just like capital gains.

Navexa lets you track foreign investments in both your tax residency’s currency and the local currency of the asset.

Foreign Investments: Track Everything Correctly

If you’re an Australian resident for tax purposes, you’ll be required to pay some form of Australian tax on foreign investments.

In general, all your worldwide income will be subject to tax, it’s just a matter of where you pay that tax. It’s always a smart idea to get familiar with the laws around this, and to consult professionals regarding your personal financial situation.

Further to this, serious investors should always track their transactions and portfolio performance for the purposes of both compliance and optimizing their investment strategy.

The Navexa portfolio tracker does exactly this. Track Australian and overseas investments, access detailed performance analytics on income, currency, trading fees and more.

And, most importantly, ensure your foreign investment gains and income are reported accurately at tax time.

Sign up to Navexa now for a free 14-day trial to see how easy tracking and reporting on foreign investments can be!

Your guide to calculating capital gains tax in Australia in 2022. From tax rates, CGT events, taxable income and more. Plus, discover four key tax reporting strategies investors use to adjust and optimize their total taxable capital gain.

Paying tax is a part of investing. It has long been a fact of life that a significant portion of our earnings will always be earmarked for payment to the state. This includes capital gains.

Tax is applied to a wide range of earnings including wages, salaries, and investment income from property, shares, and cryptocurrency.

In Australia, the tax rate that is applied to your investment income is known as the Capital Gains Tax, or CGT.

Whether you’re a seasoned investor or just starting out, it’s important to be aware of how CGT works. This article will explain how the CGT works, and how to calculate and report your capital gains in Australia in 2022.

While you can’t avoid paying CGT on your investment income, there are some strategies you should be aware of for minimizing the impact of tax on your capital gains. This blog post examines some of these strategies and provides examples of how they might look.

The Australian tax year, or financial year, runs from July 1 to June 30. This is the period for which you will need to submit your tax assessment based on any income you received during the financial year. This period is known as ‘tax season’.

How Does CGT Work?

The Australian Tax Office (ATO) requires individuals to declare investment activity in their tax return and pay tax on all investment earnings, including capital gains and dividend income.

If you buy shares, invest in property, or hold other investments which you sell at a higher price than what you bought them for, you will have made a capital gain. This means you will be paying CGT.

CGT is the tax rate that is applied to net capital gains (total gains minus total losses). It is not a set rate, but is calculated according to your marginal tax rate. This is the tax rate that you usually pay on your personal income, and will be the tax rate applied to your investment earnings.

Capital gains are taxed at an individual’s marginal tax rate

While CGT rates for individuals vary according to their marginal tax rate, flat rates apply for companies and self-managed funds.

Trading companies pay 26% if their annual turnover is less than $50 million, and if it exceeds $50 million, the CGT applied is 30%. Investment companies don’t qualify for the 26% rate and are taxed at 30%. Self-managed super funds are taxed at a lower rate of 15%.

If you sold any assets during a financial year, you will need to work out your capital gain or capital loss for each asset. CGT will need to be paid on your net capital gains.

To calculate your capital gains, you first need to know the ‘cost base’ or original purchase price of the asset. From there, you can work out how much profit you’ve made by subtracting the selling price from the cost base.

Depending on how long you’ve held the shares for, you may or may not qualify for Australia’s 50% CGT discount on investments held longer than 12 months.

The Navexa platform provides an automated solution for making these calculations — more on that later.

That’s how the CGT rate is determined. So, let’s take a closer look at which investments the CGT applies to.

What Does CGT Apply To In Australia?

CGT applies to a wide range of investment income in Australia, including earnings generated from real estate, shares, cryptocurrency, foreign exchange, and collectibles.

When you dispose of an asset for more than what you paid for it, you realize a capital gain which you will have to pay CGT on.

There are a range of other situations that will trigger the requirement to pay CGT. These are known as ‘CGT Events’. A CGT event occurs when an investor makes a capital gain or incur a capital loss on an asset.

The Australian Tax Office (ATO) imposes CGT when you make a capital gain or loss

How Does CGT Apply To Shares?

When you sell shares for more than what you paid for them and realize a capital gain, you will have to pay CGT. When other CGT events occur, you will also have to pay CGT on your shares. Examples include switching shares in a managed fund between funds, or owning shares in a company that is subject to a takeover or merger.

It is important to keep good records of all your share transactions, including amounts and dates of purchase. When you file your tax return, CGT will need to be calculated for any profits you made from selling your shares.

Does CGT Apply To Dividend Pay-outs?

Many Australian investors enjoy investing in companies that pay out dividends (a percentage share of their profits) to their shareholders. But, like other forms of income, dividends are subject to taxation.

Dividends are paid from profits that have already been subjected to Australian company tax. Because the profits have already been taxed, shareholders won’t be taxed again when they receive the profits as dividends, provided that their marginal tax rate is lower than the tax rate paid by the company.

These dividends are described as being ‘franked’. A ‘franking credit’ is attached to the dividend and represents the tax that has already been paid by the company distributing the dividend. The shareholder who receives the dividend with an attached franking credit will either pay less than their usual tax rate, or receive a tax refund.

The general rule is that if your marginal tax rate is lower than the rate of tax paid by a company or fund, you might be entitled to claim a refund. However, if your marginal tax rate is higher than the tax already paid on the dividend, you may have to pay additional tax.

Does CGT Apply To Crypto?

If you were hoping to avoid paying CGT by investing in cryptocurrency, we have bad news for you. Cryptocurrency investment in Australia is also subject to taxation, in a similar way to other investment assets.

In recent years, the cryptocurrency market has grown rapidly, and the ATO has been quick to catch up.

Crypto gains are subject to CGT in Australia.

Cryptocurrency markets have exploded in recent years and the ATO is all over it

As with other assets, CGT may apply in circumstances other than just selling your crypto. The ATO classifies four main CGT events for crypto activity:

You’ll be taxed when you:

Sell crypto.

Exchange one crypto for another.

Convert crypto to a fiat currency like AUD.

Pay for goods or services in crypto.

Just like when you pay CGT at your marginal tax rate when you sell shares, you pay this rate when you sell crypto.

Generally, you could apply the same tax rules to your crypto portfolio as you would for investment in stocks.

You must pay CGT when you realize a capital gain from property. This could include selling an investment property for more than what you paid for it or selling a block of land that you created through a subdivision process.

Your main residence is generally excluded from CGT if you meet certain criteria specified by the ATO:

You will need to have lived in the home for the whole period that you have owned it.

The home can’t have been used to produce income or have been bought with the intention of renovating and selling it for a profit.

It must be on land no greater than two hectares.

If you meet the criteria, you may be able to avoid paying CGT when you sell your house. If not, you may still qualify for a partial exemption. The ATO provides a property exemption tool on their website to help you make the calculations.

In Australia, investors can expect to pay CGT on shares, crypto, property and more.

Capital Gains Tax (CGT) has to be paid on investment income from property

If you acquired property on or prior to 20 September 1985, CGT does not apply. But it will apply to certain capital improvements made after this date. It is also important to keep track of any rental income you receive from property and include it in your tax return. For more details on CGT and property, visit the ATO.

If You Are An Investor, It Pays To Know About CGT

As you can see, CGT applies to a wide range of investment income. When you prepare your tax return, you will need to provide the ATO with your assessable income and any capital gains or capital losses you made that year.

While this article isn’t financial advice, we do advise you to be well informed. The above is not an exhaustive list of what CGT applies to in Australia, so you should check with the ATO if you are unsure about what your tax obligations are.

You can’t escape having to file a tax return, but fortunately there are a few strategies you can use to reduce your tax burden, legally.

Let’s explore some of the strategies that investors use to minimize investment tax.

Effective Strategies To Minimize Tax Payments

There are several legal investment strategies investors employ to minimize tax bills and claim tax deduction. This goes for both gains and income.

Below you’ll find some of the ways Australian investors hold on to as much of their investment gains and income as possible.

The following is not investment advice. As with all the information on the Navexa blog, it’s general investment information our writers have collated from other sources. For any financial or investment decisions, you should always understand the risks, and seek professional advice if necessary.

Strategy 1: Hold Onto Your Investments For Longer Than 12 Months

Australian tax law makes a distinction between short and long term capital gains. A long term capital gain is when you make a profit on an investment that you’ve held for longer than 12 months. It’s a short term capital gain if you’ve held the asset for shorter than 12 months.

As an investor, this is important to understand because of something known as the ‘CGT discount’.

If you’ve held an asset for longer than 12 months before a given ‘CGT event’ occurs, you may be able to claim a CGT discount of 50%. Remember, a ‘CGT event’ is the point at which you make a capital gain or loss on an asset.

Let’s say you made $30,000 profit from investments that you’d held for less than 12 months, and your marginal tax rate was 37%. You’d have a $11,100 tax liability.

However, if you’d held the asset for longer than 12 months before you sold, the CGT discount would mean your tax liability was just $5,500! That’s a significant amount saved on your tax bill.

Capital Gains Tax discount applies to a wide range of investment income, including shares, property, and cryptocurrency.

As you can see, holding onto your investments for longer than 12 months to take advantage of this discount can be much more tax effective than disposing of them quickly.

Remember, you must be an Australian resident for tax purposes to take advantage of the CGT discount. There are also some other situations where the CGT discount does not apply.

For example, the discount is not available if the asset is your home and you started using it as a rental property or business less than 12 months before disposing of it.

A CGT discount of 50% is available to Australian trusts, and complying super funds can receive a discount of 33.33%. However, companies can not take advantage of the CGT discount.

When you file your tax return, you must subtract any capital losses that you may have from your capital gains before applying the CGT discount. In most cases you will be eligible for the discount if the asset has been held for longer than 12 months.

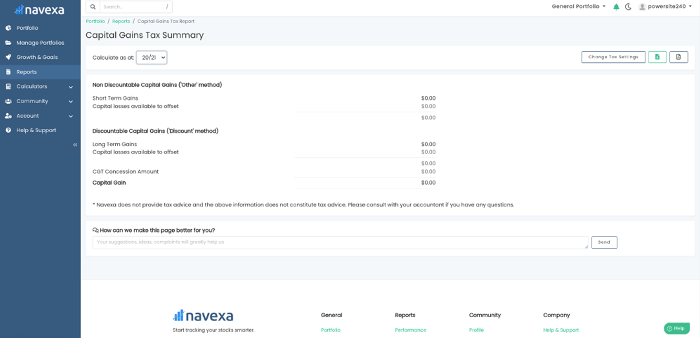

Navexa provides a platform where you can easily track your portfolio performance and calculate both your taxable capital gains and taxable income. Our CGT Reporting Tool gives a detailed breakdown of which assets are ‘non-discountable’ from a CGT perspective (those which have been held for less than the required 12 months to qualify), reducing the amount of tedious leg-work at tax time.

Navexa’s tax reporting tools remove the need to manually calculate your portfolio’s tax obligations and show you the most tax effective way to prepare a tax return.

Provided the portfolio data in your account is correct and up-to-date, you can run an automated tax report in just a few seconds.

Navexa’s CGT Reporting Tool.

What you see above is Navexa’s CGT Report.

Navexa calculates your taxable gains and displays a detailed breakdown. Capital gains are displayed according to Short or Long Term status alongside your Capital Losses Available to Offset. The report also calculates your CGT Concession Amount and finally, your total Capital Gain.

Navexa’s CGT Reporting Tool makes it easy to categorize your investments for your tax return.

Strategy 2: Offset Your Capital Gains With Capital Losses

Another useful strategy at tax time is using capital losses to offset your capital gains. While it would be nice if your assets always made gains and never losses, most of us who invest know that this isn’t the case. Thankfully, the silver lining here is that your capital losses can be used to reduce the tax you pay on your capital gains.

You will have made a capital loss when you sell an asset for less than what you paid for it. This loss can be deducted from capital gains that you made from other sources, to reduce the tax you pay. If you don’t have any capital gains to deduct from, the capital loss can generally be carried forward to future financial years. If you make capital gains in future years, the capital losses are still up your sleeve to deduct from any gains and reduce tax.

While there is no time limit on how long you can carry the losses forward if you don’t make any gains, the ATO does require that capital losses are used at the first available opportunity. This means when you have a capital gain to declare and capital losses available to offset, you must do so. They also require the earliest losses to be used first.

For example, if an investor owed $5,000 in CGT for their investments in a financial year, but had declared losses of $1,500 the previous financial year, they could carry these losses over to offset their capital gain, resulting in a reduced tax bill of $3,500.

There are some capital losses that can’t be deducted, so be aware of these. These include personal use assets such as boats or furniture, or collectables below a certain value. The ATO also won’t allow capital losses to be deducted from collectables unless they are deducted from capital gains from collectables.

Capital losses can also be deducted from your cryptocurrency assets, too. Let’s say you bought $5,000 worth of Ethereum because it had been surging in price and you were experiencing crypto-FOMO. You buy near the peak and in subsequent weeks the price crashes heavily, after a large nation announces that it won’t endorse cryptocurrency in their economy. Despite this disappointment, don’t forget that if you sell the asset and realize a capital loss, it could be a handy tool to offset other capital gains in your portfolio.

Despite a few exclusions, however, most capital losses from your investments can be deducted from capital gains you have made from other assets. If you are unsure about whether you can deduct a particular capital loss, check with the ATO.

Strategy 3: Invest In Companies That Pay High Dividends And Franking Credits

We’ve already looked at how the ATO taxes dividends, so what does this mean for minimizing your income tax obligations? Again, this is not financial advice.

Remember that companies must pay the Australian Companies Tax on their profits. If an investor receiving a dividend has a tax rate greater than the company tax rate that has already been applied to the company’s profits, they will receive a franking credit.

Let’s look at an example. Say an investor with a 32.5% tax rate receives a $1,750 dividend with a $750 franking credit attached. The franking credit takes the taxable income to $2,500, with gross tax of $812.50 payable. The franking credit rebate of $750 is deducted from the gross tax and the investor is left to pay a reduced tax amount of $62.50, leaving them with $1,687.50 after tax income. As you can see, the impact of the franking credit rebate is significant. For a full breakdown of this and other franked dividend scenarios, click here.

The investor in the above situation manages to retain most of their dividend income. Because the franking credit offsets their CGT so significantly, the amount of tax the individual pays is greatly minimized. Obviously, if your marginal tax rate is lower than 32.5% you will pay less tax and receive a larger chunk of the dividend. If you’re in a higher tax bracket than this, you will receive less.

Regardless of your marginal tax rate, franked dividends are a useful tool to reduce your tax obligations. Choosing to invest in companies that pay dividends, especially fully or highly franked dividends, is a popular strategy for minimizing tax paid on investment returns.

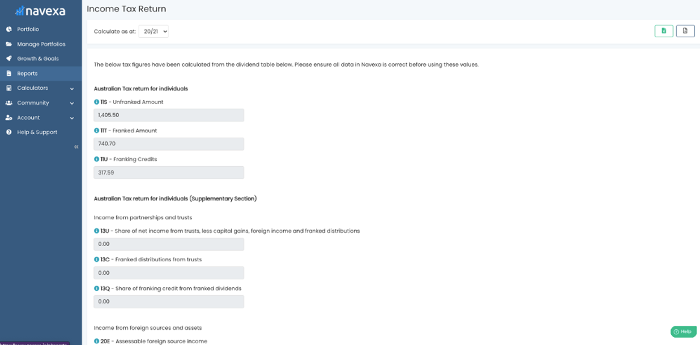

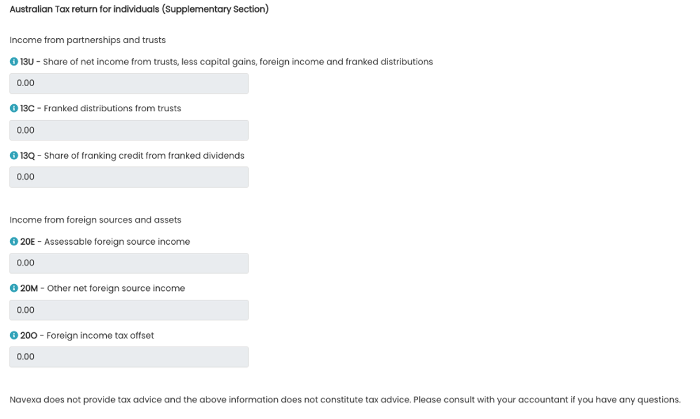

Navexa’s Taxable Income Reporting Tool

Navexa can help you accelerate the process of determining your taxable income. When you automate your portfolio tracking in Navexa, the Taxable Investment Income Report provides you with everything you need to know to prepare your tax return.

Navexa’s Taxable Investment Income Tool.

As you can see above, the Taxable Income Tool displays the Unfranked Amount and the Franked Amount for your dividends, as well as the total franking credits attached to them.

And in the below image, you can see the additional fields in the ‘Supplementary’ section. These display further tax-relevant information such as the amount of Franked Distributions From Trusts, the amount of Assessable Foreign Source Income, and your Foreign Income Tax Offset.

The report automatically categorizes sources and tax return codes.

A foreign income tax offset is when you may have already paid tax on something in another country. This might be employment income or capital gains. In some instances, you may be able to claim a foreign tax offset as part of your tax return. Navexa’s Taxable Investment Income Tool will calculate and display these details for you.

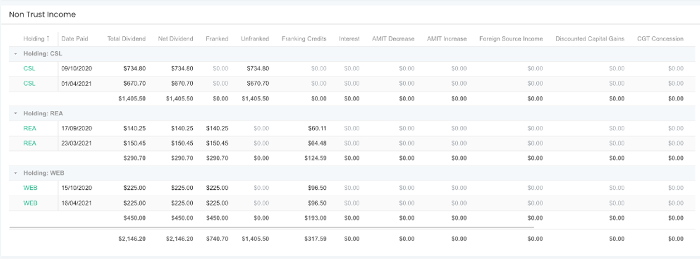

Below these fields, you’ll be provided with a holding by holding breakdown of your taxable investment income, like this:

Navexa’s holding by holding investment income breakdown.

This shows you subtotals for payments from each holding, with grand totals for each column at the bottom. Assets are organized by the dates at which you acquired them, which has important tax implications.

At the top right of the report, you’ll find buttons for exporting the report as both an XLS and a PDF file.

This helps you accelerate the process of preparing your investment income for assessment.

Let’s take a look now at how different investors might choose to dispose of their assets.

Different Tax Strategies For Disposing Of Investments

When the time comes that you want to sell, it can be easy to get excited about the potential gains you are about to realize. This excitement can be dampened, however, when you are faced with the reality of your tax bill.

Choosing a particular method to dispose of your assets can have a major impact on the profits you generate and the tax you pay on them.

Please remember that this does not constitute financial advice. Our writers have collated a wide range of information relating to investment tax that we think is useful for you to consider. As always, we recommend you do your own research before making any investment decisions — tax or otherwise

Strategy 1: First-In-First-Out (FIFO)

The first-in-first-out (FIFO) approach is a common method used by investors when they sell holdings. When you purchase a group of shares at a given price, they will constitute a ‘parcel’.

You may acquire shares in the same company in several different transactions over a period of time. Each transaction forms its own parcel of shares.

The concept of FIFO relates to the disposal of investments. When you are ready to sell shares, you can choose which parcels — sometimes called ‘lots’ — of shares you would like to sell.

Using the FIFO method, you would sell the parcels that have been held for the longest period. Provided that the share price has risen since the time of purchase, the FIFO method will ensure the greatest capital gain from the sale of a parcel of shares. Obviously, this won’t always be the case, and adopting a FIFO approach might not result in the greatest capital gain.

For example, if an investor purchased 100 shares in a company at $20 per share three years ago, and another 100 shares at $40 two years ago, they might choose to use the FIFO method when they choose to sell some of those shares.

Let’s say the company’s share price has now risen to $50. The investor sells using the FIFO method, disposing of the first 100 shares that were purchased at $20. Because the share price has grown $30 since they purchased them, they realize a gross profit of $3,000. However, if they had chosen to sell the more newly acquired shares parcel, they would only realize a gross profit of $1,000.

As mentioned, FIFO will only result in the largest capital gain if the share price has risen consistently over time. If share prices have dropped since you bought them, the FIFO approach might not result in the greatest capital gain — but it could lower your tax burden.

Strategy 2: Last-In-First-Out

In the above example, the investor opted to sell their more recently acquired shares because they wanted to maximise their capital gains. Because the share price rose over time, the FIFO approach achieved this goal.

LIFO works in the opposite manner to FIFO — your newest shares are sold first. The LIFO method ‘typically results in the lowest tax burden when stock prices have increased, because your newer shares had a higher cost and therefore, your taxable gains are less’.

If we continue to assume a consistent growth in share price, LIFO would be a useful strategy to dispose of assets and realize less capital gain from the disposal — and subsequently pay less tax.

However, don’t forget that you can only qualify for the CGT discount if you’ve held shares for longer than 12 months.

Investors have four main ways to calculate their portfolio’s capital gains.

FIFO and LIFO are based on shares being organized by time

The FIFO and LIFO approaches above assume that share prices have risen over time. When the opposite is the case, a smaller capital gain may be realized by selling the newly acquired shares or vice versa. The degree to which FIFO or LIFO suits your goals will depend on how the share price has behaved since you acquired the asset.

Some investors might opt for a more precise method of disposal such as maximum or minimum gain, to ensure that they dispose of the parcels which will return the greatest capital gain or result in the lowest tax burden.

Strategy 3: Maximum Gain

The FIFO and LIFO methods are based on selling assets based on the time at which you acquired them. One alternative approach is maximum gain, which is focused on the price at which shares were bought, rather than the time they were bought.

The suitability of FIFO or LIFO will depend on what has happened with the share price since you bought, and what your goal is. Maximum gain focuses on disposing of the assets that were acquired for the lowest price, rather than those which were acquired first or last. This approach is suitable for those looking to ensure maximum capital gains when they sell.

An example of the maximum gain approach: A prospective home buyer has found their dream home and needs to prove to their bank that they can service a large mortgage. They carefully select the shares that were bought at the lowest price in their portfolio to sell, so they can realize the maximum possible capital gain from the sale. While they will pay the most tax using this method, the capital gain will be the largest, and this will help paint a healthy financial picture to the bank.

But, you may want to minimize your CGT obligations.

Strategy 4: Minimum Gain

The minimum gain approach works in the opposite way to maximum gain — you select the parcels of shares in your portfolio that you acquired for the most expensive price and sell these first. By choosing to sell the tax lots with the highest cost base, you will minimize your gain.

This strategy is generally used by investors who want to minimize their CGT obligations. As we know, less capital gain = less tax paid.

Minimum and Maximum gain, as well as FIFO and LIFO approaches, will suit different investors depending on their requirements.

Regardless of what your aspirations are, and which approach you choose, it is important to make sure that your investment portfolio is kept in good order.

Record keeping is paramount in both portfolio management and personal finance — particularly as it concerns reporting your investment activity to the tax authorities.

The above strategies are probably best deployed when you have a clear understanding of your portfolio’s performance. It is important to keep an accurate record of your transaction history, including the dates and prices at which you bought particular shares. This knowledge is vital if you wish to select the most tax-efficient disposal strategy that you can. Or in some instances, simply if you want to maximise your capital gains.

The Navexa Portfolio Tracker automates this entire process, from tracking trades and transactions to optimizing how you report CGT on a portfolio.

Remember, Navexa doesn’t offer tax advice. We always encourage you to consult your accountant or seek other professional advice when it comes to investments and taxes.

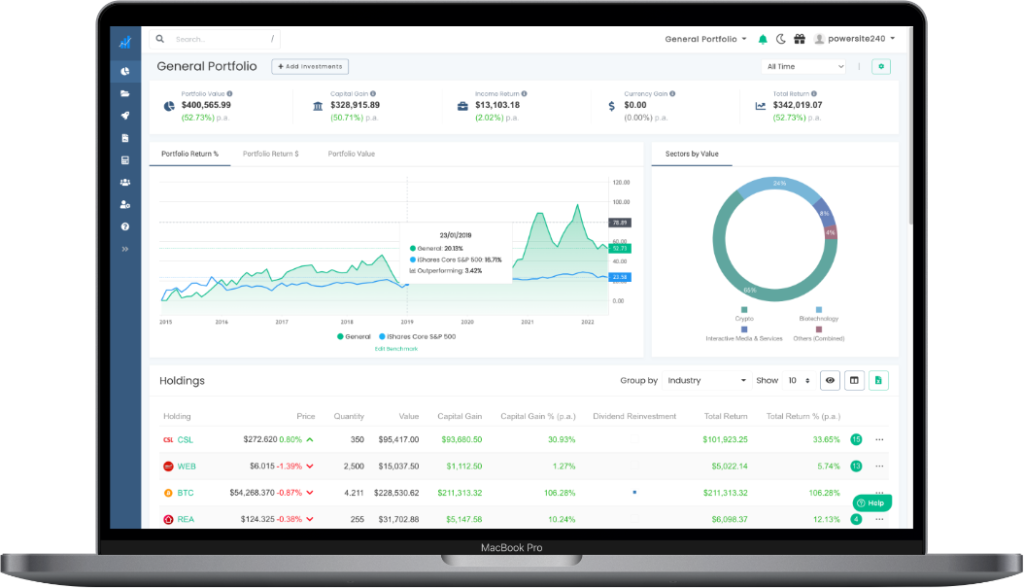

The Navexa portfolio tracker’s portfolio overview.

Automate Your Portfolio Tax Reporting & Optimization With Navexa

Navexa is a platform for tracking your investment portfolio and displaying detailed information that will help you better understand your performance — and better handle investment tax reporting.

When it is time to prepare your tax return, you should have a clear vision of what you want to achieve. Whether you are looking to maximise your capital gains or minimize the impact of CGT, Navexa makes the process fast and stress-free.

Our CGT and the Taxable Income tools can help you determine your obligations and options when it is time to file your tax return.

Join thousands of Australian investors already using Navexa to manage their investment portfolios.

With Navexa you can:

Track your stocks and crypto investments together in one account.

Automatically track capital gains, portfolio income, currency gains and losses and trading fees.

Benchmark your long-term portfolio performance against any index you choose.

Automatically track your dividend and distribution income from stocks, ETFs, LICs and Mutual/Managed Funds

Use the Dividend Reinvestment Plan (DRPs/DRIPs) feature to track the impact of DRP transactions on your performance (and tax)

See the complete picture of your investment performance, including the impact of brokerage fees, dividends, and capital gains with Navexa’s annualized performance calculation methodology

Run powerful tax reports to calculate your dividend income with the Taxable Income Report

Calculate your CGT obligations with our Australian Capital Gains Tax Report and the Unrealised Capital Gains Tax Report

An introduction to some of the (legal) ways to optimize investment taxes in Australia.

Paying tax is part of investing. While you can’t avoid paying tax (at least, not legally), there are several ways in which you can reduce the impact of tax on your investment earnings.

This post explains the tax system in Australia as it relates to investment income, and introduces some strategies Australians use to minimize their investment taxes.

Different investment strategies have different tax obligations

Tax And Investing In Australia

The Australian Tax Office (ATO) requires individuals to declare investment activity in their tax return and pay tax on all investment earnings, including capital gains and dividend income.

If you buy shares, invest in property, or hold other investments and then sell them at a higher price, you will have made a capital gain.

The Capital Gains Tax (CGT) is the tax rate that is applied to net capital gains (total gains minus total losses).

How Does the Capital Gains Tax (CGT) Work?

The capital gains tax is not a set rate but is calculated according to an individual’s marginal tax rate. This is the tax rate for personal income, and will be the tax rate applied to investment earnings.

Capital gains are taxed at an individual’s marginal tax rate

Unlike CGT rates for individuals, flat CGT rates apply for companies and self-managed funds. Trading companies pay 26% if their annual turnover is less than $50 million. If it exceeds $50 million, the CGT applied is 30%. Investment companies don’t qualify for the 26% rate and are taxed at 30%. Self-managed super funds are taxed at a lower rate of 15%.

Getting back to individual taxation, if you sold any investments during a financial year, including shares, you will need to work out your capital gain or loss for each asset. CGT will need to be paid on your net capital gains. The Navexa platform provides a straightforward solution for making these calculations — more on that later.

Which Investments Does The CGT Apply To?

CGT applies to a wide range of investments, including property, shares, and cryptocurrency. When you sell an asset and realize a gain from that sale, you will be charged CGT.

In addition to owing CGT when you sell an asset, the tax also applies in other investment situations, or ‘CGT events’. A CGT event occurs when you make a capital gain or incur a capital loss.

Examples of other CGT events include switching shares in a managed fund between funds or owning shares in a company that is subject to a takeover or merger.

The ATO considers these dividends ‘franked’. A ‘franking credit’ is attached to the dividend and represents the tax that has already been paid by the company distributing the dividend. The shareholder who receives the dividend with an attached franking credit will either owe less than their usual tax rate, or receive a tax refund.

Tax And Cryptocurrency

Cryptocurrency investment is also subject to taxation in Australia. Cryptocurrency is taxed in a similar way to other investment assets.

The ATO classifies four main CGT events for crypto activity.

You’ll be taxed when you:

Sell cryptocurrency.

Exchange one crypto for another.

Convery crypto to fiat currency like AUD.

Pay for goods or services in crypto.

Just like when you pay CGT at your marginal tax rate when you sell shares, you owe this rate when you sell crypto.

Capital gains are taxed for cryptocurrency investments, too.

Now that we’ve discussed the basics of tax for Australian investors, let’s explore some of the strategies that investors use to minimize investment tax.

Effective Strategies to Minimize Tax Payments

There are several legal investment strategies investors employ to minimize tax bills and claim tax deduction. This goes for both gains and income.

Below you’ll find some of the ways Australian investors hold on to as much of their investment gains and income as possible.

The following is not investment advice. As with all the information on the Navexa blog, it’s general investment information our writers have collated from other sources. For any financial or investment decisions, you should always understand the risks and seek professional advice if necessary.

Strategy 1: Hold Onto Your Investments For Longer Than 12 Months

Australian tax law makes a distinction between short and long term capital gains. A long term capital gain is when you make a profit on an investment that you’ve held for longer than 12 months.It’s ashort term capital gain if you’ve held the asset for less than 12 months.

As an investor, this is important to understand, because of something known as the ‘CGT discount’.

If you’ve held an asset for longer than 12 months before a given ‘CGT event’ occurs, you may be able to claim a CGT discount of 50%. Remember, a ‘CGT event’ is the point at which you make a capital gain or loss on an asset.

Fifty percent is a significant discount. If you made $40,000 profit from investments that you’d held for less than 12 months, and your marginal tax rate was 37%, you’d have a $14,800 tax liability.

However, if you’d held for longer than 12 months, the CGT discount rules would mean your tax liability was just $7,400 — a much more ‘tax effective’ amount.

The CGT discount applies to crypto investments, too.

As you can see, holding onto your investments for longer than 12 months to take advantage of this tax discount can be much more tax effective.

Navexa provides a platform where you can easily track your asset performance and calculate your taxable gains. The CGT Reporting Tool gives a detailed breakdown of which assets are ‘non-discountable’ from a CGT perspective and reduces the amount of tedious leg-work at tax time.

Navexa’s tax reporting tools remove the need to manually calculate their portfolio tax obligations or the most tax effective way to prepare a tax return.

Provided the portfolio data in your account is correct and up-to-date, you can run an automated tax report in just a few seconds.

Navexa’s Capital Gains Tax Tool

Navexa’s CGT reporting tool

What you see above is Navexa’s CGT Report.

Navexa calculates your taxable gains and displays a detailed breakdown. Capital gains are displayed according to Short or Long Term status alongside your Capital Losses Available to Offset. The report also calculates your CGT Concession Amount and finally, your total Capital Gain.

Navexa’s CGT Reporting Tool makes it easy to categorize your investments for your tax return, while the Unrealized Capital Gains report can help show the most tax efficient way to dispose of investments.

Strategy 2: Lower Capital Gains With Capital Losses

Another useful tool for investors at tax time is their capital losses.

You make a capital loss when you sell an asset for less than what you paid for it. This loss can be deducted from your capital gains (from other sources) to reduce the amount of tax. If you don’t have any capital gains to deduct from, the capital loss can generally be carried forward to future financial years. If you make capital gains in future years, the capital losses are still up your sleeve to deduct from any gains and reduce tax.

For example, if an investor owed $4,000 in CGT for their investments in a financial year, but had declared losses of $1,500 the previous financial year, they could carry these losses over to offset their capital gain, resulting in a reduced tax bill of $2,500.

Strategy 3: Invest In Companies That Pay High Dividends And Franking Credits

We’ve already looked at how the ATO taxes dividends, so what does this mean for minimizing your income tax obligations?

For example, an investor with a 32.5% tax rate receives a $1,750 dividend with a $750 franking credit attached. The franking credit takes the taxable income to $2,500, with gross tax of $812.50 payable. The franking credit rebate of $750 is deducted from the gross tax and the investor is left to pay only $62.50 in tax, leaving them with $1,687.50 after tax income. For a full breakdown of this and other franked dividend scenarios, click here.

As you can see, the investor in the above situation manages to retain most of dividend income. Because the franking credit offsets their CGT so significantly, the amount of income tax the individual pays is greatly minimized.

Choosing to invest in companies that pay dividends, especially fully or highly franked dividends, is a popular strategy for minimizing tax paid on investment returns. Fully franked dividends are effectively tax free income.

Navexa can also help you accelerate the process of determining your taxable income. When you automate your portfolio tracking in Navexa, the Taxable Investment Income tool provides you with everything you need to know to prepare your tax return.

Navexa’s Taxable Income Tool

As you can see above, the Taxable Income Tool displays the Unfranked Amount and the Franked Amount for your dividends, as well as the total Franking Credits attached to them.

And in the below image, you can see the additional fields in the ‘Supplementary’ section. These display further tax-relevant information such as the amount of Franked Distributions From Trusts, the amount of Assessable Foreign Source Income, and your Foreign Income Tax Offset.

Fully franked dividends are like tax free investment income!

Below these fields, you’ll also be provided with a holding by holding breakdown of your taxable investment income, like this:

Navexa’s holding by holding investment income breakdown

This shows you subtotals for payments from each holding, and grand totals for each column at the bottom.

At the top right of the report, you’ll find buttons for exporting the report as both an XLS and PDF file.

This helps you accelerate the process of preparing your investment income for assessment.

Dispose Of Your Investments In A Tax-Efficient Way

When the time comes that you want to sell it can be easy to get excited about the potential gains you are about to realize. This excitement can be dampened, however, when you are faced with the reality of your tax bill.

Choosing a particular method to dispose of your investments can have a major impact on the profits you generate and the tax you pay on them.

First-In-First-Out (FIFO)

The first-in-first-out (FIFO) approach is a common method used by investors when they sell holdings. When you purchase a group of shares at a given price, they will constitute a ‘parcel’.

You may acquire shares in the same company in several different. Each transaction will form its own parcel of shares.

The concept of FIFO relates to the disposal of investments. When you are ready to sell shares, you can choose which parcels — sometimes called ‘lots’ — of shares you would like to sell. The FIFO method involves disposing of the parcels that have been held for the longest period. Provided that the share price has risen since the time of purchase, the FIFO method will ensure the greatest capital gain from the sale of a selection of shares.

For example, if an investor purchased 100 shares at $20 in a company three years ago, and another 100 shares at $40 in the company two years ago, they might choose to use the FIFO method when they choose to sell some of those shares.

Let’s say the company’s share price has now risen to $50. The investor opts to sell using the FIFO method, disposing of the first 100 shares which were purchased at $20. Because the share price has grown $30 since they purchased them, they realize a gross profit of $3,000. However, if they had chosen to sell the more newly acquired shares parcel, they would only realize a gross profit of $1,000. The FIFO method is therefore popular with investors looking to maximise capital gains when they sell. But what about tax?

Last-In-First-Out (LIFO)

In the above example, the investor opted not to sell their more recently acquired shares because they wanted to maximise their capital gains. But if you are looking to minimize the impact of tax, adopting the LIFO approach could be advantageous.

LIFO works in the opposite manner to FIFO — your newest shares are sold first. The LIFO method ‘typically results in the lowest tax burden when stock prices have increased, because your newer shares had a higher cost and therefore, your taxable gains are less’.

Because the investor has chosen to dispose of shares that were bought at a higher price, they realize a smaller capital gain — and subsequently pay a lower tax bill.

However, don’t forget that you can only qualify for the CGT discount if you’ve held the shares that you sell for over a year.

The FIFO and LIFO approaches discussed above assume that the share prices involved have risen over time. This won’t always be the case. If the price of an asset drops over time, a smaller capital gain may be realized by selling the newly acquired shares. Smaller capital gain = less tax.

In some instances, investors might choose to dispose of a particular lot or parcel that cost more than the current share price so they can realize a capital loss. This capital loss could be used to offset other capital gains.

Regardless of the approach you choose, it is important to keep good records and understand the tax implications of disposing of the various share parcels in your portfolio.

We hope you’ve enjoyed this quick guide to investment tax and some of the strategies investors use to help minimize their tax bill in Australia.

Navexa doesn’t offer tax advice, and we always encourage you consult your accountant or seek other professional advice when it comes to investments and taxes.

Navexa is a platform where you can easily track your investment portfolio and display detailed information that will help you at tax time.

Navexa empowers investors to build brighter financial futures with simple, but powerful, automated investment analytics and reporting tools.

Features such as the CGT Reporting Tool and the Taxable Investment Income Tool can help you determine your obligations and opportunities when the time comes to pay the tax man.