Compound annual growth rate, or CAGR, is one of the key methods for calculating investment performance. Here’s how to calculate it manually — and a fast way to automatically see an investment’s compound annual growth rate.

CAGR, or compound annual growth rate, is a method investors use to measure the annual growth rate of an investment. Generally it’s only used for portfolios that compound their growth by generating income which is in turn subject to capital appreciation.

While it’s not the only method of determining an investment’s long-term annual returns, it is one of the most popular. As we’ll show in this explainer, CAGR has advantages and disadvantages — which is why the Navexa portfolio tracker allows you to compare CAGR-measured performance with other calculation methods.

What Is Compound Interest?

To understand CAGR and its possibilities, you should first understand how compound interest works. Compound interest is what happens when money accrues interest, and that interest then accrues more, and so on. Basically, it’s an interest you earn on interest.

On the opposite end, there’s simple interest. This type of interest represents financial gains an investor earns just on the principal portion of the loan or their initial investment. In other words, simple interest is limited to one earning cycle — it leaves out interest earning more interest.

Compound interest is what happens when money accrues interest, and that interest then accrues more.

Definition of Compound Annual Growth Rate

Compound annual growth rate is defined as the rate of return required for an investment to grow from its starting balance to the ending value. It’s used when profits are reinvested at the end of each period.

With CAGR, investors can compare the present value of two or more stocks, and see which one has performed better over a certain timeframe.

CAGR calculates past performance. Furthermore, the compound annual growth rate isn’t the same as the true rate of return. Instead, CAGR is a metric used to determine how an investment may perform in the future, based on past performance.

Investors use CAGR as an estimate, rather than the exact measurement of the portfolio performance. It’s important to understand that neither CAGR, nor any other performance calculation methods, are any guarantee of future performance.

Other Growth Metrics to Know

Here are some other metrics investors use to help measure their journey.

Year-over-Year (YoY) Growth compares the changes in annualized metrics at the fiscal year-end date.

Month-over-Month Growth (MoM) compares the changes in the value of a metric at the end of the current month compared to the past month.

Last Twelve Months (LTM) is the timeframe of the immediately preceding 12 months, often used to evaluate a company’s performance.

Reinvestment Rate is the expected return that occurs after the reinvestment of the previous gains.

What Is CAGR Used For?

The CAGR is used to calculate an investments’ performance when compounding gains, or interest, are taken into account. It presumes profits or income will be reinvested, and gives a representational figure, which, as you’ll see shortly, has benefits and limitations as far as understanding performance.

CAGR is useful for understanding long-term performance in that it smooths out the effects of volatility. If an investment is up 10% one year and down 5% the next, then up 4% the next year, CAGR shows the long-term trend.

CAGR presumes profits or income will be reinvested, and gives a representational figure

Benefits and Downsides of CAGR

There are many advantages of using the compound annual growth rate formula:

It’s one of the most reliable ways of calculating ROI for compound interest.

Helps compare stock performance in different time periods.

Can be used for each investment separately.

Fixes the limitations of the average return calculation.

Works better for short-term calculations.

Some of the CAGR calculation’s limitations:

Doesn’t account for investment risks.

Implies a constant growth rate, which is not always the case.

Can’t be used to measure the profitability of an asset’s inflows and outflows.

Ignores market volatility.

CAGR Formula

To calculate CAGR, investors divide the value of the investment at the end of the period of time (EV) by the value of the investment at the beginning of the period (BV).

The next step is to raise the result to an exponent of 1 divided by the number of years (n).

Then, subtract one from the result.

To get the percentage, investors multiply the result by 100.

The complete formula looks like this:

CAGR = (EV / BV) ^ 1/n – 1 x 100

Modification of the CAGR formula

Investors have to modify the CAGR formula to get the correct data on their investments.

They need to know how long they’ve been holding a particular asset. To get this number, investors calculate how many days they held an asset for the beginning and the end of the period, then take into account all the other “complete” years, shown in days.

For example, someone held the investment for 300 days during the first year, plus three years (equals 1,095 days), then exited the position after 200 days in the last year. Their total holding period is 300 + 1,095 + 200 = 1,595 days.

To get the years, divide by 365, which makes 4.369.

They can then use this number in the CAGR formula, where n = 4.369

CAGR Calculated via Excel Spreadsheet

Some investors like to track their stock performance via an Excel spreadsheet. It’s possible, but not as easy — Excel requires that they use “RATE” (used for calculating the rate of return), and the “COUNTA” function (counts the number of years) to get the desired value.

However, there’s an easier way to calculate compound annual growth rate, using the CAGR calculator online.

CAGR Calculator

An online calculator is a simple solution to calculate an investment’s compound annual growth rate. Online calculators are straightforward, and investors get results immediately.

But, if you don’t want to deal with any calculations, Navexa is here to help.

Navexa: Automatic CAGR Calculations

Sometimes, calculating CAGR requires collecting a lot of data from your portfolio. The Navexa portfolio tracking platform can calculate investment performance using multiple formulas. Just upload your portfolio, and Navexa will do all the work for you.

Once you finish uploading your holdings, you can toggle between “Simple” and “Compound” and the platform will provide you with detailed performance metrics.

With Navexa, there’s no need to question whether the CAGR calculator is correct. You’ll get the data instantly within the app, so you know how your portfolio performs.

Example of CAGR Formula

If you’re still struggling to understand how compound annual growth rate works when using a formula, here’s an example.

Let’s say a company has a revenue of $100 million at the end of year 0.

Three years from then, the company is projected to reach a revenue of $150 million.

To start calculating, you should ignore the initial year (year 0), as the formula only takes into account the compounded revenue. To get the initial balance, subtract the beginning period (year 0) from the ending period (year 3).

Proceed to enter the following data into the compound annual growth rate formula:

Beginning Value = $100 million

Ending Value = $150 million

Number of Periods = 3 years

In this case, the annual growth rate CAGR formula looks like this:

CAGR = (150 million / 100 million) ^ 1/3 – 1 x 100

Based on this example, the compound annual growth rate is 14.47 %

CAGR vs. IRR

CAGR shows the return of an investment over a specific time period. However, there’s one more calculation you should know about — the Internal Rate of Return (IRR).

IRR also measures growth rate and performance, but in a more flexible way compared to CAGR.

One of the key differences between CAGR and IRR is that CAGR is used for simple calculations. Additionally, investors can calculate CAGR by hand, or with a CAGR calculator.

IRR, is used to show the growth rate of complex investments. IRR is used with portfolios with various cash inflows and outflows. If you want to measure IRR, you’ll likely need a powerful calculator or an accounting system.

IRR is often used for an investment that can’t be managed with a CAGR calculation.

CAGR shows the return of an investment over a specific time period. IRR also measures growth rate and performance, but in a more flexible way compared to CAGR.

CAGR vs. AAGR

Average Annual Growth Rate (AAGR) is another performance calculation. While CAGR accounts for the compound annual growth rate, AAGR doesn’t. Instead, it’s a linear measure that shows the average annual return.

What is Risk-Adjusted CAGR?

The risk-adjusted formula helps the investor determine whether a certain investment is worth the risk. With this method, investors measure and compare the generated returns and risks. This gives them an idea of the potential ending value of their portfolio.

Risk-adjusted CAGR requires a bit more calculation, and is more advanced. This is because it takes into account the standard deviation figure — a measure of volatility, which is different for every asset.

Calculating risk-adjusted CAGR is done by multiplying the CAGR by 1 and subtracting the standard deviation. In case the volatility number is 0, CAGR remains the same. However, with a higher standard deviation, CAGR gets lower.

This formula helps investors compare multiple investments and decide which one can provide the highest likelihood of returns for the desired time period. Again, no calculation method is ever going to protect against investment risk or predict future performance reliably.

How Investors Use CAGR

There are many ways to use CAGR in investing. The first is to determine the rate of return and likely future value of an investment.

Additionally, CAGR helps investors set objectives and calculate the rate they need to successfully grow their investment. This is especially true for risk-adjusted CAGR. This formula includes the risks related to a specific investment, which helps determine future growth rates.

The CAGR formula is also an ideal way of comparing multiple investment opportunities. Using it to forecast future value helps investors make strategic decisions.

The Importance of CAGR for Companies

Investors aren’t the only ones calculating growth rates and dealing with CAGR. Business owners and CEOs also utilize CAGR to determine company performance.

Finally, CAGR is crucial for companies that plan to give out dividends to shareholders, as it shows the company’s (positive or negative) performance between two different years.

What is Considered Good CAGR?

Generally speaking, a CAGR of 15% to 25% for the period of five years would considered a good compound annual growth rate for stocks and mutual funds.

However, if the CAGR were lower than 12% for stocks and mutual funds, investors might gravitate towards other opportunities, such as real estate or other securities.

See Your CAGR & Simple Returns in Navexa

Compound annual growth rate (CAGR) is one of the methods investors measure the performance of their holdings. The formula is fairly simple, but it doesn’t account for market volatility and investment risks, unless you use a risk-adjusted one.

The CAGR formula can only be used for compounding investments. Compound annual growth rate is different from AAGR, which simply shows the average change for one year. Many investors prefer CAGR since it smoothes out the year-by-year volatility in growth rates.

Among many other features, Navexa also offers CAGR calculations based on uploaded portfolio data. Simply toggle between ‘Simple’ and ‘Compound’ to get accurate data instantly. To check out how it works, register today and start your free trial.

Time-weighted return is one of the most popular ways of measuring investment performance and calculating returns. We explain how to calculate TWR and explore other key methods of tracking portfolio performance.

It can be challenging for investors to find the best method of measuring portfolio performance and investment returns. The time-weighted return is on of the most common ways of doing so.

Besides a simple rate of return, there’s the time-weighted return (TWR) method. It’s among the most common formulas used to track investment performance. In short, it accounts for moments when cash flows occur, and creates sub-periods to help investors track growth rates.

Keep reading to learn how bankers, investment professionals, and portfolio managers use a time-weighted rate of return to evaluate investment performance.

Impact of Inflows and Outflows of a Portfolio

Cash flows are vital to time-weighted returns

Before diving into the time-weighted return, it’s crucial to understand cash flows. Cash flows are an important part of calculating portfolio performance. They also make a difference in which method experts use, because each performance calculation treats inflows and outflows differently.

Cash flows, or inflows and outflows, represent the total money transferred into and out of one’s portfolio — deposits and withdrawals. The example of inflows includes proceeds from the selling the asset. Outflows can be payments for buying a stock.

Cash flows can be used to define a sub-period, and the method that will be used to calculate the rate of return — the money-weighted rate of return, or time-weighted rate of return formulas.

If someone invested money and never made any withdrawals from their portfolio, calculating the rate of return on their investments would be easy. Any method would give the same result, since there were no outflows and inflows to observe across the sub-periods.

Still, this rarely happens in practice, and cash flows are always present. Investors may make changes in their portfolios daily, and calculating the weighted rate of return can be challenging. Since each method (TWR, RoR, MWRR) handles these cash flows differently, each will give a different performance number.

Here’s what you should know about the time-weighted return.

What Is the Time-Weighted Return?

Time-weighted returns are one measure of compound growth.

Time-weighted return (TWR) is a method of measuring the compound growth rate of one’s portfolio. This method is designed to help investors eliminate the distorting effects of deposits and withdrawals.

TWR breaks up the investment performance into sub-periods, based on the moment when the money was added to, or taken out of, the account. Then, it provides the rate of return for each interval with cash flow changes.

Is Time-Weighted Return Correct?

By isolating the intervals based on these inflows and outflows, TWR provides more accurate numbers than simply subtracting the beginning balance from the final value of the portfolio.

Additionally, the time-weighted rate of return formula multiplies the returns for each sub-period, links them together, and shows how the returns have compounded.

The time-weighted rate assumes all gains are reinvested in the portfolio.

This method is also more commonly used by fund managers, or bankers, and not private investors. This is because fund managers usually don’t have control over cash flows, but still need some way to calculate portfolio performance and returns for their clients.

Can Time-Weighted Return Be Used to Compare Investments?

Some experts argue that TWR shouldn’t be used to compare investment performance, and that the money-weighted rate of return formula (equal to IRR) is a better measurement for comparison. This is mainly due to the complexity of its formula, which is not ideal for regular investors.

However, TWR remains preferred among fund managers and finance experts who don’t have control on the cash flows in the portfolios they manage.

Time-Weighted vs. Basic Rate of Return

The rate of return is one of the simplest ways of calculating the rate of return over a certain period. RoR is shown in percentage and represents the change from the beginning of the holding period until the end.

RoR is not always an accurate measurement, since it doesn’t account for cash flows. However, the time-weighted return calculation is there to eliminate the effect of cash flows, and create intervals based on when the money was added or withdrawn from one’s portfolio.

By isolating each time period, TWR provides more accurate results. In practice, the sub-periods between cash flow events are treated as constituent performance units, which are then combined to give the total performance for the overarching period.

However, there’s another method to compare it with.

Time-Weighted vs. Money-Weighted Rate of Return

Money-weighted rate of return accounts for timing and size of a portfolio’s cash outflows.

Money-weighted rate of return (MWRR), which is equal to an internal rate of return (IRR) is another performance measurement method.

While the time-weighted method factors in the moment of change, creates the period for each change, and calculates period return, MWRR accounts for both the timing and sizes of cash outflows, such as:

The cost of a purchased investment

Withdrawals

Reinvested dividends

It also accounts for inflows:

Received dividends

Deposits

Sale proceeds

Contributions

The key difference between TWR and MWRR is that MWRR doesn’t create time periods based on cash flows like the TWRR. This means that any cash flow within a time period can impact MWRR. If there’s no cash flow, both methods should provide similar results.

Money-weighted rate of return is a more complicated, but more accurate measurement of investment performance. This is also the most appropriate way to measure the return on investment.

The Importance of the Time-Weighted Return

Since the time-weighted return is based on cash flow, but used to calculate the period return for each interval, it’s usually used as a reflection of the investment strategy. Investors find it’s easier to calculate returns once the performance is broken down into sub-periods.

The TWR method helps them further isolate cash flows for each period and gain more accurate results. Plus, the TWR multiplies each sub-period, and shows how the returns compound over time.

This performance method is crucial for investment managers, since they don’t have control over cash flows in the portfolios they manage.

What Does the Time-Weighted Return Tell?

Since TWR is used to generate sub-periods and link them, it’s one of the best methods to see how the returns compound over time. When calculated correctly, TWR also shows the results of an investment strategy. It strips the impact of cash flows, and reveals pure investment performance.

How to Calculate Time-Weighted Return

Investors and fund managers who calculate time-weighted return start by calculating the rate of return for each sub-period. This is done by subtracting the ending balance from the initial value.

Then, they divide that difference by the initial value of the holding period.

The key is to create a new sub-period for each cash flow, and calculate the RoR for each of these.

Investors then add “1” to each of the return amounts. This simplifies the calculation of negative return numbers, and assures the formula works correctly.

Then, they multiply the rates of return for each sub-period, and subtract “1” to yield the time-weighted return.

TWR Formula

TWR = ((1+HP1) x (1+HP2) x (1+HPn)) – 1

TWR = Time-Weighted Return

HP = (End Value – (Beginning Value + Cash Flow)) / (Beginning Value + Cash Flow)

n = Number of Periods

HPn = Return for sub-period n

In addition to the basic TWR formula, two other calculations can clarify the portfolio performance — Simple and Modified Dietz methods.

Simple Dietz method

Since TWR doesn’t account for cash flows that likely occur during the holding period, the Simple Dietz method can be used to address this. This method assumes that cash flows occurred either at the beginning, middle, or the end of the measured periods (day, month, or year).

It compensates for external cash flows. The formula is:

R = B – A – C / A + C/2

R = rate of return,

A = beginning market value

B = ending market value

C = net external inflow during the period

Modified Dietz Method

The Modified Dietz Method is the most common way of calculating time-weighted returns.

The Modified Dietz method is also the most common way of calculating TWR. However, it’s not perfect, and may skew the results in certain circumstances.

Issues with timing

One of the main issues with calculating portfolio performance is the assumption that all transactions happen at the same time within each sub-period. If the sub-period is one day, we calculate the data as if all transactions happen at the beginning and end of the day.

This can lead to errors, as sometimes the change in the portfolio is equal to zero and we can’t apply some formulas. In such cases, experts would have to further adjust the Modified Dietz method for better results.

Issues with negative or zero capital

The average capital is usually positive. However, if a larger outflow occurs, the average capital could go to zero or become negative. This can cause the Modified Dietz calculations to show a negative balance when there’s an actual profit, and vice versa.

One of the solutions is to catch a moment when the outflow happens, account for it, and use the simple returns calculation for specific period returns.

Excel Sheet

Some fund managers like to use Excel to calculate the time-weighted return. They either download an existing template, or use formulas in the sheet.

Others create their own Excel sheet. They enter the portfolio data manually, starting with the beginning and ending values for each period. Then, they calculate the return for each of the sub-period.

To get to the TWR, experts should add 1 to each of the results (to mitigate the negative returns), use the geometric mean function, and finally subtract one at the end. Excel can then turn it into a percentage form.

Automatically Calculating TWR With The Navexa Portfolio Tracker

If you’re looking for an easier way to get the accurate time-weighted return, the Navexa portfolio tracker uses a version of the Modified Dietz method. Our performance calculation accounts for the performance of assets, and the size, and frequency of cash flows for each sub-period.

This provides a clear idea actual investment performance. Simply upload the portfolio data you need to track, and Navexa will calculate the returns. Plus, the tracker will also annualize the numbers for an easier overview.

Navexa does so using live market data from the ASX, NASDAQ, NYSE and global cryptocurrency markets, displaying intra-day pricing and performance.

Advantages of the Time-Weighted Return

There are several advantages to the time-weighted return method. It:

Is a solid indicator of investment performance,

Eliminates the impact of cash flow,

Provides a clear picture of returns after each deposit/withdrawal,

Is suitable for measuring investment managers’ performance,

Links periodic returns.

Disadvantages of the Time-Weighted Return

Due to the complex nature of investing, TWR still has some disadvantages. This calculation can turn out to be challenging when the money moves in and out of the portfolio more often. The common changes may skew the final number, and provide less accurate results.

Additionally, the TWR doesn’t measure how long the money has been invested, or when it was invested. This is why some investors may prefer IRR instead.

TWR is often used to track performance month over month. However, using the TWR is tricky if there’s an increased cash flow occurring within each month or day.

Examples of Using the Time-Weighted Return

The best way to understand how the time-weighted rate of return works is through an example. Let’s say that an investor has the portfolio of this value:

Dec. 31, 2011 — $100,000

Jan. 31, 2012 — $110,000

Apr. 30, 2012 — $103,000

Nov. 30, 2012 — $120,000

Dec 31. 2012 — $135,000

This makes four time periods we should observe:

Dec. 31, 2011 to Jan. 31 2012 (HP1)

Jan. 31, 2012 to Apr. 30 2012 (HP2)

Apr. 30, 2012 to Nov. 30, 2012 (HP3)

Nov. 30, 2012 to Dec 31. 2012 (HP4)

Additionally, this person made a $12,000 withdrawal on March 3, 2012 (occurred during HP2) and a $20,000 deposit on December 20, 2012, (HP4).

Now we should calculate the holding period return for each period:

To get to time-weighted rate of return, we should now add 1 to each of the period results and multiply them together, then subtract one:

( (1 + 0.100) x (1 + 0.0455) x (1 + 0.1650) x (1 + 0.0417) ) – 1 = 0.2840

To get a percentage, multiply the result by 100, which equals 28.4%.

The Navexa Portfolio Tracker automatically tracks portfolio performance using the Modified Dietz Method and money-weighted return calculation.

Summary: Time-Weighted Return Calculation

The time-weighted rate of return is a great method of measuring portfolio performance. It’s a preferred method among financial experts, bankers, and fund managers. The TWR formula focuses on time periods when cash flows occurred, and helps experts calculate growth for each period.

Time-weighted return is considered a standard in portfolio management, but still has some flaws. But by adjusting the calculation, fund managers and investors can overcome these issues, and measure growth correctly.

A money-weighted return, on the other hand, measures compound growth in the value of all funds invested in a portfolio over the evaluation period.

Navexa is one of the easiest tools to use for understanding your returns and portfolio performance. Our advanced performance calculation utilizes the Modified Dietz method.

Not only that, but when you track your performance in Navexa, you can examine performance at both the portfolio and individual investment level, and toggle between simple and compound returns in a single click.

Your guide to calculating capital gains tax in Australia in 2022. From tax rates, CGT events, taxable income and more. Plus, discover four key tax reporting strategies investors use to adjust and optimize their total taxable capital gain.

Paying tax is a part of investing. It has long been a fact of life that a significant portion of our earnings will always be earmarked for payment to the state. This includes capital gains.

Tax is applied to a wide range of earnings including wages, salaries, and investment income from property, shares, and cryptocurrency.

In Australia, the tax rate that is applied to your investment income is known as the Capital Gains Tax, or CGT.

Whether you’re a seasoned investor or just starting out, it’s important to be aware of how CGT works. This article will explain how the CGT works, and how to calculate and report your capital gains in Australia in 2022.

While you can’t avoid paying CGT on your investment income, there are some strategies you should be aware of for minimizing the impact of tax on your capital gains. This blog post examines some of these strategies and provides examples of how they might look.

The Australian tax year, or financial year, runs from July 1 to June 30. This is the period for which you will need to submit your tax assessment based on any income you received during the financial year. This period is known as ‘tax season’.

How Does CGT Work?

The Australian Tax Office (ATO) requires individuals to declare investment activity in their tax return and pay tax on all investment earnings, including capital gains and dividend income.

If you buy shares, invest in property, or hold other investments which you sell at a higher price than what you bought them for, you will have made a capital gain. This means you will be paying CGT.

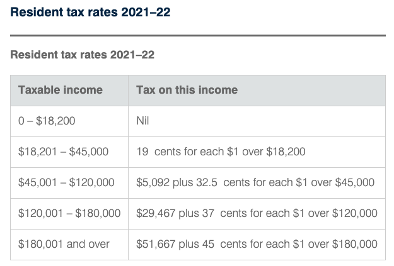

CGT is the tax rate that is applied to net capital gains (total gains minus total losses). It is not a set rate, but is calculated according to your marginal tax rate. This is the tax rate that you usually pay on your personal income, and will be the tax rate applied to your investment earnings.

Capital gains are taxed at an individual’s marginal tax rate

While CGT rates for individuals vary according to their marginal tax rate, flat rates apply for companies and self-managed funds.

Trading companies pay 26% if their annual turnover is less than $50 million, and if it exceeds $50 million, the CGT applied is 30%. Investment companies don’t qualify for the 26% rate and are taxed at 30%. Self-managed super funds are taxed at a lower rate of 15%.

If you sold any assets during a financial year, you will need to work out your capital gain or capital loss for each asset. CGT will need to be paid on your net capital gains.

To calculate your capital gains, you first need to know the ‘cost base’ or original purchase price of the asset. From there, you can work out how much profit you’ve made by subtracting the selling price from the cost base.

Depending on how long you’ve held the shares for, you may or may not qualify for Australia’s 50% CGT discount on investments held longer than 12 months.

The Navexa platform provides an automated solution for making these calculations — more on that later.

That’s how the CGT rate is determined. So, let’s take a closer look at which investments the CGT applies to.

What Does CGT Apply To In Australia?

CGT applies to a wide range of investment income in Australia, including earnings generated from real estate, shares, cryptocurrency, foreign exchange, and collectibles.

When you dispose of an asset for more than what you paid for it, you realize a capital gain which you will have to pay CGT on.

There are a range of other situations that will trigger the requirement to pay CGT. These are known as ‘CGT Events’. A CGT event occurs when an investor makes a capital gain or incur a capital loss on an asset.

The Australian Tax Office (ATO) imposes CGT when you make a capital gain or loss

How Does CGT Apply To Shares?

When you sell shares for more than what you paid for them and realize a capital gain, you will have to pay CGT. When other CGT events occur, you will also have to pay CGT on your shares. Examples include switching shares in a managed fund between funds, or owning shares in a company that is subject to a takeover or merger.

It is important to keep good records of all your share transactions, including amounts and dates of purchase. When you file your tax return, CGT will need to be calculated for any profits you made from selling your shares.

Does CGT Apply To Dividend Pay-outs?

Many Australian investors enjoy investing in companies that pay out dividends (a percentage share of their profits) to their shareholders. But, like other forms of income, dividends are subject to taxation.

Dividends are paid from profits that have already been subjected to Australian company tax. Because the profits have already been taxed, shareholders won’t be taxed again when they receive the profits as dividends, provided that their marginal tax rate is lower than the tax rate paid by the company.

These dividends are described as being ‘franked’. A ‘franking credit’ is attached to the dividend and represents the tax that has already been paid by the company distributing the dividend. The shareholder who receives the dividend with an attached franking credit will either pay less than their usual tax rate, or receive a tax refund.

The general rule is that if your marginal tax rate is lower than the rate of tax paid by a company or fund, you might be entitled to claim a refund. However, if your marginal tax rate is higher than the tax already paid on the dividend, you may have to pay additional tax.

Does CGT Apply To Crypto?

If you were hoping to avoid paying CGT by investing in cryptocurrency, we have bad news for you. Cryptocurrency investment in Australia is also subject to taxation, in a similar way to other investment assets.

In recent years, the cryptocurrency market has grown rapidly, and the ATO has been quick to catch up.

Crypto gains are subject to CGT in Australia.

Cryptocurrency markets have exploded in recent years and the ATO is all over it

As with other assets, CGT may apply in circumstances other than just selling your crypto. The ATO classifies four main CGT events for crypto activity:

You’ll be taxed when you:

Sell crypto.

Exchange one crypto for another.

Convert crypto to a fiat currency like AUD.

Pay for goods or services in crypto.

Just like when you pay CGT at your marginal tax rate when you sell shares, you pay this rate when you sell crypto.

Generally, you could apply the same tax rules to your crypto portfolio as you would for investment in stocks.

You must pay CGT when you realize a capital gain from property. This could include selling an investment property for more than what you paid for it or selling a block of land that you created through a subdivision process.

Your main residence is generally excluded from CGT if you meet certain criteria specified by the ATO:

You will need to have lived in the home for the whole period that you have owned it.

The home can’t have been used to produce income or have been bought with the intention of renovating and selling it for a profit.

It must be on land no greater than two hectares.

If you meet the criteria, you may be able to avoid paying CGT when you sell your house. If not, you may still qualify for a partial exemption. The ATO provides a property exemption tool on their website to help you make the calculations.

In Australia, investors can expect to pay CGT on shares, crypto, property and more.

Capital Gains Tax (CGT) has to be paid on investment income from property

If you acquired property on or prior to 20 September 1985, CGT does not apply. But it will apply to certain capital improvements made after this date. It is also important to keep track of any rental income you receive from property and include it in your tax return. For more details on CGT and property, visit the ATO.

If You Are An Investor, It Pays To Know About CGT

As you can see, CGT applies to a wide range of investment income. When you prepare your tax return, you will need to provide the ATO with your assessable income and any capital gains or capital losses you made that year.

While this article isn’t financial advice, we do advise you to be well informed. The above is not an exhaustive list of what CGT applies to in Australia, so you should check with the ATO if you are unsure about what your tax obligations are.

You can’t escape having to file a tax return, but fortunately there are a few strategies you can use to reduce your tax burden, legally.

Let’s explore some of the strategies that investors use to minimize investment tax.

Effective Strategies To Minimize Tax Payments

There are several legal investment strategies investors employ to minimize tax bills and claim tax deduction. This goes for both gains and income.

Below you’ll find some of the ways Australian investors hold on to as much of their investment gains and income as possible.

The following is not investment advice. As with all the information on the Navexa blog, it’s general investment information our writers have collated from other sources. For any financial or investment decisions, you should always understand the risks, and seek professional advice if necessary.

Strategy 1: Hold Onto Your Investments For Longer Than 12 Months

Australian tax law makes a distinction between short and long term capital gains. A long term capital gain is when you make a profit on an investment that you’ve held for longer than 12 months. It’s a short term capital gain if you’ve held the asset for shorter than 12 months.

As an investor, this is important to understand because of something known as the ‘CGT discount’.

If you’ve held an asset for longer than 12 months before a given ‘CGT event’ occurs, you may be able to claim a CGT discount of 50%. Remember, a ‘CGT event’ is the point at which you make a capital gain or loss on an asset.

Let’s say you made $30,000 profit from investments that you’d held for less than 12 months, and your marginal tax rate was 37%. You’d have a $11,100 tax liability.

However, if you’d held the asset for longer than 12 months before you sold, the CGT discount would mean your tax liability was just $5,500! That’s a significant amount saved on your tax bill.

Capital Gains Tax discount applies to a wide range of investment income, including shares, property, and cryptocurrency.

As you can see, holding onto your investments for longer than 12 months to take advantage of this discount can be much more tax effective than disposing of them quickly.

Remember, you must be an Australian resident for tax purposes to take advantage of the CGT discount. There are also some other situations where the CGT discount does not apply.

For example, the discount is not available if the asset is your home and you started using it as a rental property or business less than 12 months before disposing of it.

A CGT discount of 50% is available to Australian trusts, and complying super funds can receive a discount of 33.33%. However, companies can not take advantage of the CGT discount.

When you file your tax return, you must subtract any capital losses that you may have from your capital gains before applying the CGT discount. In most cases you will be eligible for the discount if the asset has been held for longer than 12 months.

Navexa provides a platform where you can easily track your portfolio performance and calculate both your taxable capital gains and taxable income. Our CGT Reporting Tool gives a detailed breakdown of which assets are ‘non-discountable’ from a CGT perspective (those which have been held for less than the required 12 months to qualify), reducing the amount of tedious leg-work at tax time.

Navexa’s tax reporting tools remove the need to manually calculate your portfolio’s tax obligations and show you the most tax effective way to prepare a tax return.

Provided the portfolio data in your account is correct and up-to-date, you can run an automated tax report in just a few seconds.

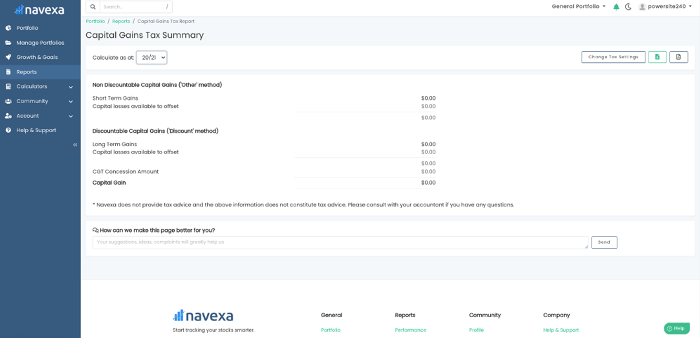

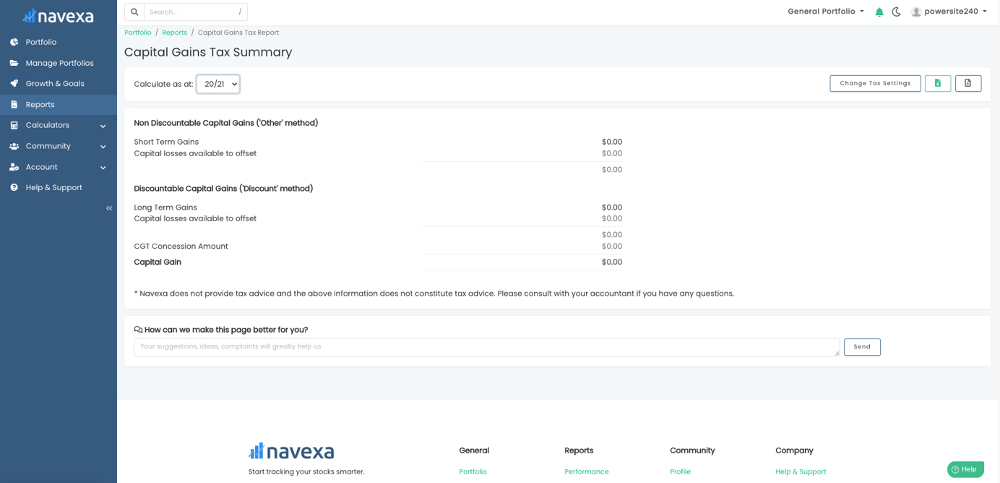

Navexa’s CGT Reporting Tool.

What you see above is Navexa’s CGT Report.

Navexa calculates your taxable gains and displays a detailed breakdown. Capital gains are displayed according to Short or Long Term status alongside your Capital Losses Available to Offset. The report also calculates your CGT Concession Amount and finally, your total Capital Gain.

Navexa’s CGT Reporting Tool makes it easy to categorize your investments for your tax return.

Strategy 2: Offset Your Capital Gains With Capital Losses

Another useful strategy at tax time is using capital losses to offset your capital gains. While it would be nice if your assets always made gains and never losses, most of us who invest know that this isn’t the case. Thankfully, the silver lining here is that your capital losses can be used to reduce the tax you pay on your capital gains.

You will have made a capital loss when you sell an asset for less than what you paid for it. This loss can be deducted from capital gains that you made from other sources, to reduce the tax you pay. If you don’t have any capital gains to deduct from, the capital loss can generally be carried forward to future financial years. If you make capital gains in future years, the capital losses are still up your sleeve to deduct from any gains and reduce tax.

While there is no time limit on how long you can carry the losses forward if you don’t make any gains, the ATO does require that capital losses are used at the first available opportunity. This means when you have a capital gain to declare and capital losses available to offset, you must do so. They also require the earliest losses to be used first.

For example, if an investor owed $5,000 in CGT for their investments in a financial year, but had declared losses of $1,500 the previous financial year, they could carry these losses over to offset their capital gain, resulting in a reduced tax bill of $3,500.

There are some capital losses that can’t be deducted, so be aware of these. These include personal use assets such as boats or furniture, or collectables below a certain value. The ATO also won’t allow capital losses to be deducted from collectables unless they are deducted from capital gains from collectables.

Capital losses can also be deducted from your cryptocurrency assets, too. Let’s say you bought $5,000 worth of Ethereum because it had been surging in price and you were experiencing crypto-FOMO. You buy near the peak and in subsequent weeks the price crashes heavily, after a large nation announces that it won’t endorse cryptocurrency in their economy. Despite this disappointment, don’t forget that if you sell the asset and realize a capital loss, it could be a handy tool to offset other capital gains in your portfolio.

Despite a few exclusions, however, most capital losses from your investments can be deducted from capital gains you have made from other assets. If you are unsure about whether you can deduct a particular capital loss, check with the ATO.

Strategy 3: Invest In Companies That Pay High Dividends And Franking Credits

We’ve already looked at how the ATO taxes dividends, so what does this mean for minimizing your income tax obligations? Again, this is not financial advice.

Remember that companies must pay the Australian Companies Tax on their profits. If an investor receiving a dividend has a tax rate greater than the company tax rate that has already been applied to the company’s profits, they will receive a franking credit.

Let’s look at an example. Say an investor with a 32.5% tax rate receives a $1,750 dividend with a $750 franking credit attached. The franking credit takes the taxable income to $2,500, with gross tax of $812.50 payable. The franking credit rebate of $750 is deducted from the gross tax and the investor is left to pay a reduced tax amount of $62.50, leaving them with $1,687.50 after tax income. As you can see, the impact of the franking credit rebate is significant. For a full breakdown of this and other franked dividend scenarios, click here.

The investor in the above situation manages to retain most of their dividend income. Because the franking credit offsets their CGT so significantly, the amount of tax the individual pays is greatly minimized. Obviously, if your marginal tax rate is lower than 32.5% you will pay less tax and receive a larger chunk of the dividend. If you’re in a higher tax bracket than this, you will receive less.

Regardless of your marginal tax rate, franked dividends are a useful tool to reduce your tax obligations. Choosing to invest in companies that pay dividends, especially fully or highly franked dividends, is a popular strategy for minimizing tax paid on investment returns.

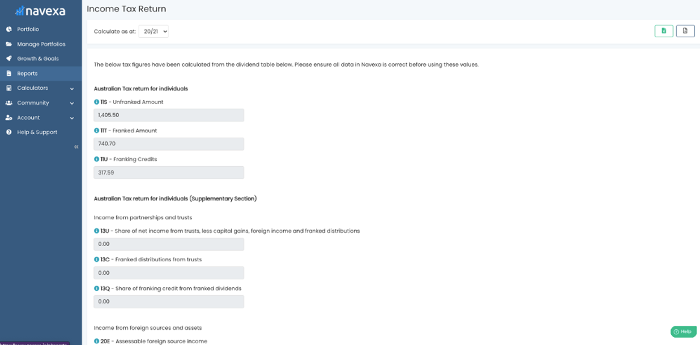

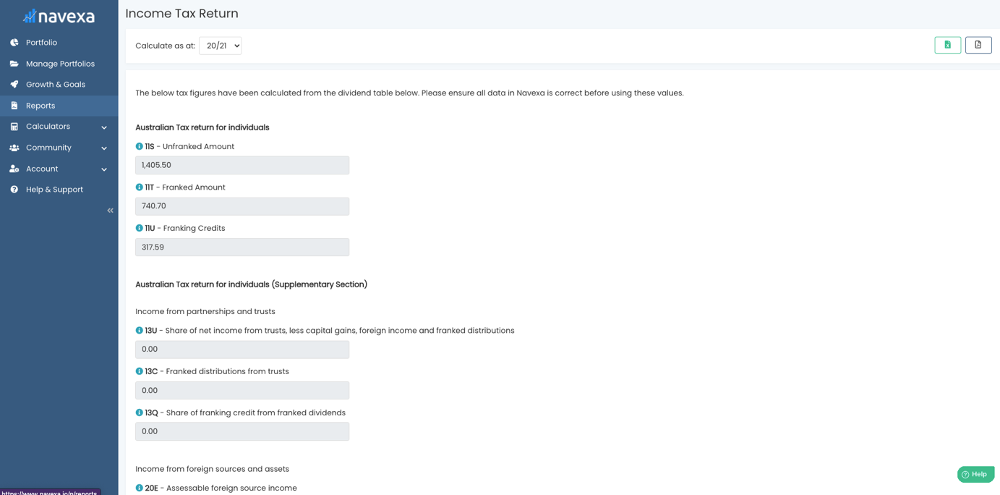

Navexa’s Taxable Income Reporting Tool

Navexa can help you accelerate the process of determining your taxable income. When you automate your portfolio tracking in Navexa, the Taxable Investment Income Report provides you with everything you need to know to prepare your tax return.

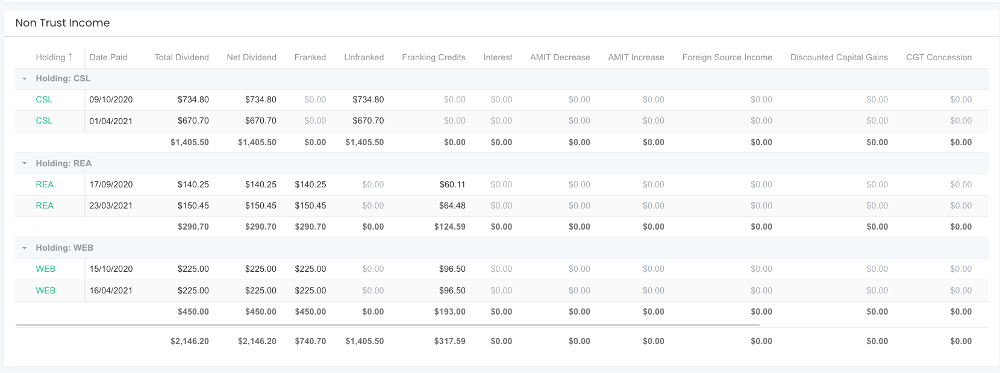

Navexa’s Taxable Investment Income Tool.

As you can see above, the Taxable Income Tool displays the Unfranked Amount and the Franked Amount for your dividends, as well as the total franking credits attached to them.

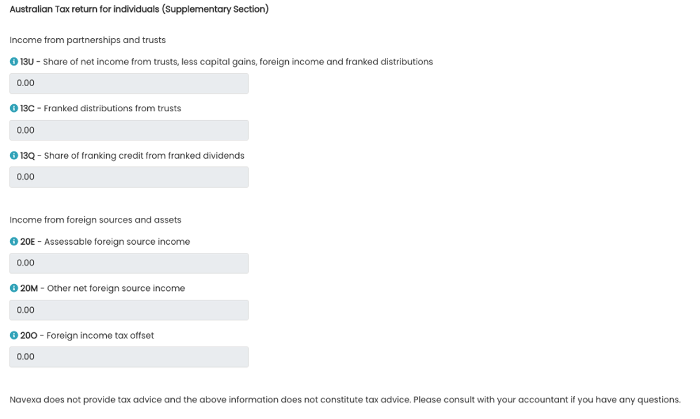

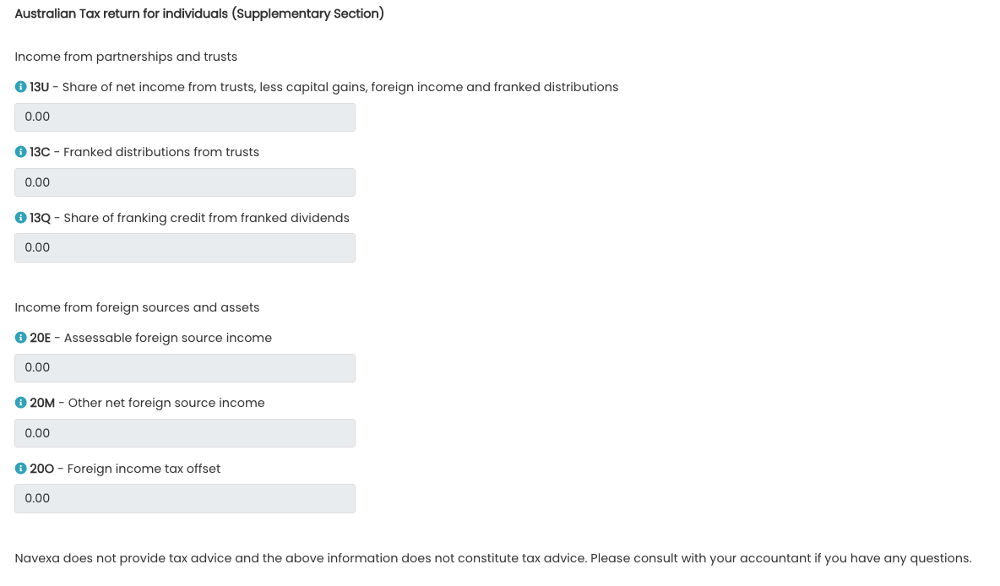

And in the below image, you can see the additional fields in the ‘Supplementary’ section. These display further tax-relevant information such as the amount of Franked Distributions From Trusts, the amount of Assessable Foreign Source Income, and your Foreign Income Tax Offset.

The report automatically categorizes sources and tax return codes.

A foreign income tax offset is when you may have already paid tax on something in another country. This might be employment income or capital gains. In some instances, you may be able to claim a foreign tax offset as part of your tax return. Navexa’s Taxable Investment Income Tool will calculate and display these details for you.

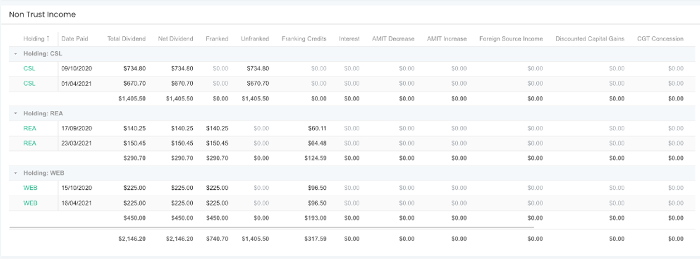

Below these fields, you’ll be provided with a holding by holding breakdown of your taxable investment income, like this:

Navexa’s holding by holding investment income breakdown.

This shows you subtotals for payments from each holding, with grand totals for each column at the bottom. Assets are organized by the dates at which you acquired them, which has important tax implications.

At the top right of the report, you’ll find buttons for exporting the report as both an XLS and a PDF file.

This helps you accelerate the process of preparing your investment income for assessment.

Let’s take a look now at how different investors might choose to dispose of their assets.

Different Tax Strategies For Disposing Of Investments

When the time comes that you want to sell, it can be easy to get excited about the potential gains you are about to realize. This excitement can be dampened, however, when you are faced with the reality of your tax bill.

Choosing a particular method to dispose of your assets can have a major impact on the profits you generate and the tax you pay on them.

Please remember that this does not constitute financial advice. Our writers have collated a wide range of information relating to investment tax that we think is useful for you to consider. As always, we recommend you do your own research before making any investment decisions — tax or otherwise

Strategy 1: First-In-First-Out (FIFO)

The first-in-first-out (FIFO) approach is a common method used by investors when they sell holdings. When you purchase a group of shares at a given price, they will constitute a ‘parcel’.

You may acquire shares in the same company in several different transactions over a period of time. Each transaction forms its own parcel of shares.

The concept of FIFO relates to the disposal of investments. When you are ready to sell shares, you can choose which parcels — sometimes called ‘lots’ — of shares you would like to sell.

Using the FIFO method, you would sell the parcels that have been held for the longest period. Provided that the share price has risen since the time of purchase, the FIFO method will ensure the greatest capital gain from the sale of a parcel of shares. Obviously, this won’t always be the case, and adopting a FIFO approach might not result in the greatest capital gain.

For example, if an investor purchased 100 shares in a company at $20 per share three years ago, and another 100 shares at $40 two years ago, they might choose to use the FIFO method when they choose to sell some of those shares.

Let’s say the company’s share price has now risen to $50. The investor sells using the FIFO method, disposing of the first 100 shares that were purchased at $20. Because the share price has grown $30 since they purchased them, they realize a gross profit of $3,000. However, if they had chosen to sell the more newly acquired shares parcel, they would only realize a gross profit of $1,000.

As mentioned, FIFO will only result in the largest capital gain if the share price has risen consistently over time. If share prices have dropped since you bought them, the FIFO approach might not result in the greatest capital gain — but it could lower your tax burden.

Strategy 2: Last-In-First-Out

In the above example, the investor opted to sell their more recently acquired shares because they wanted to maximise their capital gains. Because the share price rose over time, the FIFO approach achieved this goal.

LIFO works in the opposite manner to FIFO — your newest shares are sold first. The LIFO method ‘typically results in the lowest tax burden when stock prices have increased, because your newer shares had a higher cost and therefore, your taxable gains are less’.

If we continue to assume a consistent growth in share price, LIFO would be a useful strategy to dispose of assets and realize less capital gain from the disposal — and subsequently pay less tax.

However, don’t forget that you can only qualify for the CGT discount if you’ve held shares for longer than 12 months.

Investors have four main ways to calculate their portfolio’s capital gains.

FIFO and LIFO are based on shares being organized by time

The FIFO and LIFO approaches above assume that share prices have risen over time. When the opposite is the case, a smaller capital gain may be realized by selling the newly acquired shares or vice versa. The degree to which FIFO or LIFO suits your goals will depend on how the share price has behaved since you acquired the asset.

Some investors might opt for a more precise method of disposal such as maximum or minimum gain, to ensure that they dispose of the parcels which will return the greatest capital gain or result in the lowest tax burden.

Strategy 3: Maximum Gain

The FIFO and LIFO methods are based on selling assets based on the time at which you acquired them. One alternative approach is maximum gain, which is focused on the price at which shares were bought, rather than the time they were bought.

The suitability of FIFO or LIFO will depend on what has happened with the share price since you bought, and what your goal is. Maximum gain focuses on disposing of the assets that were acquired for the lowest price, rather than those which were acquired first or last. This approach is suitable for those looking to ensure maximum capital gains when they sell.

An example of the maximum gain approach: A prospective home buyer has found their dream home and needs to prove to their bank that they can service a large mortgage. They carefully select the shares that were bought at the lowest price in their portfolio to sell, so they can realize the maximum possible capital gain from the sale. While they will pay the most tax using this method, the capital gain will be the largest, and this will help paint a healthy financial picture to the bank.

But, you may want to minimize your CGT obligations.

Strategy 4: Minimum Gain

The minimum gain approach works in the opposite way to maximum gain — you select the parcels of shares in your portfolio that you acquired for the most expensive price and sell these first. By choosing to sell the tax lots with the highest cost base, you will minimize your gain.

This strategy is generally used by investors who want to minimize their CGT obligations. As we know, less capital gain = less tax paid.

Minimum and Maximum gain, as well as FIFO and LIFO approaches, will suit different investors depending on their requirements.

Regardless of what your aspirations are, and which approach you choose, it is important to make sure that your investment portfolio is kept in good order.

Record keeping is paramount in both portfolio management and personal finance — particularly as it concerns reporting your investment activity to the tax authorities.

The above strategies are probably best deployed when you have a clear understanding of your portfolio’s performance. It is important to keep an accurate record of your transaction history, including the dates and prices at which you bought particular shares. This knowledge is vital if you wish to select the most tax-efficient disposal strategy that you can. Or in some instances, simply if you want to maximise your capital gains.

The Navexa Portfolio Tracker automates this entire process, from tracking trades and transactions to optimizing how you report CGT on a portfolio.

Remember, Navexa doesn’t offer tax advice. We always encourage you to consult your accountant or seek other professional advice when it comes to investments and taxes.

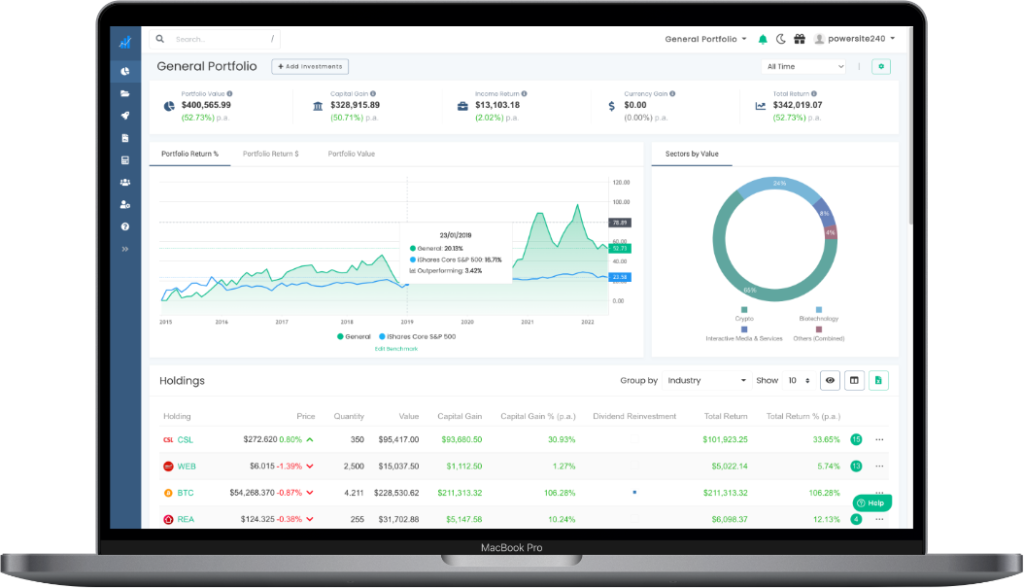

The Navexa portfolio tracker’s portfolio overview.

Automate Your Portfolio Tax Reporting & Optimization With Navexa

Navexa is a platform for tracking your investment portfolio and displaying detailed information that will help you better understand your performance — and better handle investment tax reporting.

When it is time to prepare your tax return, you should have a clear vision of what you want to achieve. Whether you are looking to maximise your capital gains or minimize the impact of CGT, Navexa makes the process fast and stress-free.

Our CGT and the Taxable Income tools can help you determine your obligations and options when it is time to file your tax return.

Join thousands of Australian investors already using Navexa to manage their investment portfolios.

With Navexa you can:

Track your stocks and crypto investments together in one account.

Automatically track capital gains, portfolio income, currency gains and losses and trading fees.

Benchmark your long-term portfolio performance against any index you choose.

Automatically track your dividend and distribution income from stocks, ETFs, LICs and Mutual/Managed Funds

Use the Dividend Reinvestment Plan (DRPs/DRIPs) feature to track the impact of DRP transactions on your performance (and tax)

See the complete picture of your investment performance, including the impact of brokerage fees, dividends, and capital gains with Navexa’s annualized performance calculation methodology

Run powerful tax reports to calculate your dividend income with the Taxable Income Report

Calculate your CGT obligations with our Australian Capital Gains Tax Report and the Unrealised Capital Gains Tax Report

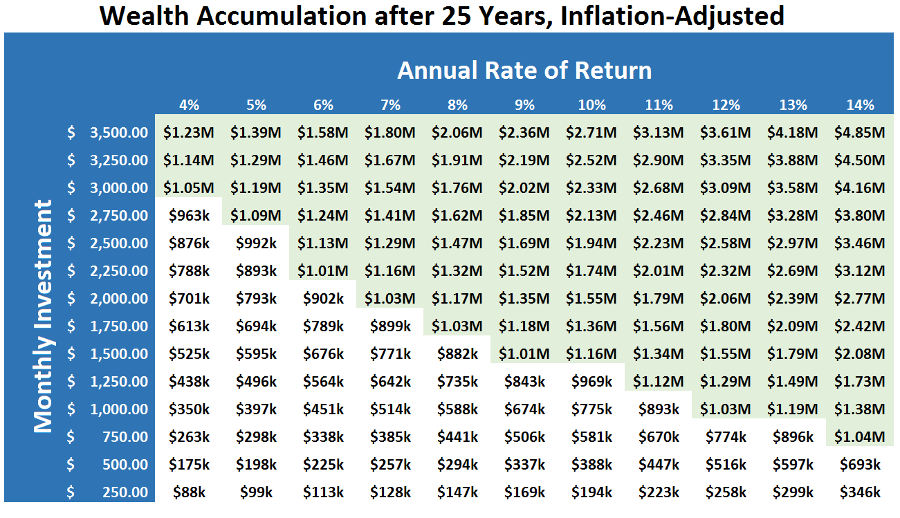

Using the Rule of 72 is a simple method for getting an approximate idea of how long it takes for your money to double. So how can you use it in tracking your investments?

In a perfect world, investors would like to know, in advance, how long it will take to double their money in the stock market. Knowing exactly how long this will take is helpful in planning out portfolio diversification, and eventually achieving financial freedom.

But, how does one go about working out how long it might take to double the value of a portfolio?. Investors can easily become confused. Especially when it comes to accounts that receive annual interest. Then, they may reach for complex formulae, and spreadsheets.

But, there’s a simpler, better way of calculating the period it will take to double one’s investment.

One of the best ways is to use the Rule of 72 — one of the simplest methods of calculating when one’s portfolio will double in value.

What is the Rule of 72?

The Rule of 72 refers to the mathematical concept that shows how long it will take an investment to double in value (in theory). It’s a simple formula that anyone can use to determine the approximate time when an investment will double at a given annualized rate of return.

However, the Rule of 72 only works for calculating compounding growth. Investors can use the Rule of 72 only for an account that earns compound interest, not simple interest. Additionally, the Rule of 72 works better with an interest rate ranging from 6% to 10%.

Besides being used to show exponential growth of a portfolio, the Rule of 72 is also used to show exponential decay. For example, the loss of purchasing power caused by inflation, or the drop in the population numbers.

Compound Growth vs. Simple Growth

Interest helps the portfolio growth, and allocating a certain amount of money to an account that earns interest is a smart move investors make. There are two types of growth, or interest — simple and compound, and these are crucial for using the Rule of 72.

Compound interest is added to the already existing interest, plus the principal amount of the loan or deposit.

This type of interest is calculated with the following formula:

A = P (1 + r) (n)

On the other hand, simple interest is added only to the original investment. The formula for simple interest is:

A = P (1 + Rt)

Compound interest is better, as it can reduce the time required to double the money in an account, and grows the investments exponentially.

In other words, compounding interest grows an investment more and more every year, since the interest gets calculated on progressively larger amounts. Whereas simple interest doesn’t compound on itself over time.

Origins of the Rule of 72

While it may sound surprising, the Rule of 72, and the concept of interest aren’t new ideas. Even ancient civilizations, such as the Mesopotamian, Greek, and Roman, used them in transactions, and basic money management.

While it may not have been called the Rule of 72, it was always around. For example, lenders always wanted to know how to manage their investments, and the rate of return.

Who Came up With the Rule of 72?

The first person to ever take note of the Rule of 72 was Luca Pacioli. Pacioli was an Italian mathematician. He mentioned the Rule of 72 in his book Summa de Arithmetica, Geometria, Proportioni et Proportionalita (Summary of Arithmetic, Geometry, Proportions, and Proportionality), published in 1494.

Pacioli stated that people who wish to know how many years it will take to double their investment should always ‘keep the number 72 in mind.’

Pacioli never went deeper into defining or explaining the reasoning behind 72.

With that in mind, it could have happened that someone else invented the number to improve their calculation of the interest rate, and portfolio growth. Some even say that Albert Einstein was the one to invent the Rule of 72, but that was never confirmed.

Why Is It Called the Rule of 72?

There’s no specific reason this rule is called the Rule of 72. Still, it serves to replace the complex logarithmic calculation that most investors are having trouble dealing with. The exact formula for determining how many years it takes to double your money based on compounding interest, or growth, is:

ln(2) / ln(1 + (interest rate/100))

where “In” represents the natural log value.

Good mathematicians could use this formula to get accurate results by observing return rates, and natural logs. The actual number that’s derived from the formula is 69.3. However, since this number is not easy to work with, people usually replace it with 72, since it’s equally good in showing the approximate number of years necessary to double the investment.

Navexa’s portfolio tracker is even easier to use. Our portfolio tracker automatically calculates every aspect of portfolio performance for shares, cryptocurrency, cash accounts and more.

How to Use the Formula?

To calculate how long it would take for the investment to double in value, one can use the following formula:

Years to double = 72 / expected rate of return

This method can also be used to calculate the expected rate of return.

Investors should divide 72 with the years to double to get the rate of return on their investment (expected rate of return = 72 / years to double).

This principle handles fractions, or portions of the year. Plus, the resulting rate of return includes compounding interest on the investment.

However, there are a few things to pay attention to:

the interest rate should not be a decimal

this formula should be applied to an investment that receives annual interest (compounding)

the farther the interest rates are from 8%, the less accurate the results would be

to calculate lower interest rates, one can drop the number to 71

this formula is easily divisible, but not perfectly accurate

Rule of 72 — Variations

Since this principle provides an approximate result, sometimes investors use slight variations, like the Rule of 69, Rule of 70, or Rule of 73.

These numbers are used in the same way, and serve to calculate the years required for the investment to double in value.

Rule of 72 — Examples

Here’s a simple example of using the method to calculate how long it takes for the investment to double:

Let’s say an account earns 4% of annual interest.

dividing 72 by 4 would give the years it takes for the money to double – 18.

When used to show inflation, and other deprecating numbers, the formula is the same.

However, the final result will show the years it will take for the amount to be cut in half.

Since this principle provides an approximate result, sometimes investors use slight variations, like the Rule of 69, Rule of 70, or Rule of 73.

Both novice, and experienced investors could use the Rule of 72 to estimate the doubling time of their holdings. Since the Rule of 72 is easy to use, almost anyone can estimate how long it will take for a certain number to double in value.

Who Uses The Rule of 72?

Since this rule can be used outside of personal finance and investing, it’s also used by other experts who need to estimate how many years it will take for a value to double.

What Is the Rule of 72 Good For?

The Rule of 72 is a good method that can be applied to anything that grows (or decays) exponentially. For example:

GDP

Inflation

Investment compounding interest rate

Credit card debt

House mortgage

Car loan refinancing

How Does the Rule of 72 Work?

By using the Rule of 72, investors can get an approximation of the years it will take for their assets to double in value.

This makes the Rule of 72 one of the key personal finance formulae to understand for investingt. Plus, this rule gives a general idea of how many “doubles” an investor might get during their lifetime, or for a certain period.

Does It Show Accurate Results?

When it comes to the accuracy of this rule, the Rule of 72 provides approximate information about the desired time period.

This formula is a simplification of the more complex logarithmic equation. Investors who wish to get an accurate result would have to do the entire calculation, or use an electronic spreadsheet calculator.

As we previously mentioned, this rule is usually used to determine the rate of return on the investment. However, experts in various industries can also apply this principle to anything that is compounding, and this doesn’t necessarily involve money.

For example, a city’s population that grows/decreases by a certain percentage per year can also use the rule to check how long it would take for the population to double, or halve.

Limitations of This Principle

Besides not being completely accurate in showing data, this formula is also mainly applied to compounding interest accounts, not simple interest ones. What’s more, the Rule of 72 works better for lower interest rates, and is less precise as the interest rate increases.

Additionally, this calculation can’t be used to forecast how long it might take to get a double return with decentralized finance and cryptocurrency, due to high market volatility, and sudden changes in prices.

In fact, no calculation can give anyone a 100% accurate prediction of what their investments may or may not do in the future.

Speculating Future Returns With The Rule Of 72

When people invest, they often want to know how long it will take to double their money. However, predicting the exact number of years can be tricky.

This is why the Rule of 72 exists. When used correctly, with an investment that involves compound interest,this formula is generally fairly accurate — provided, of course, the annualized rate of return remains consistent.

here are certain limitations investors should be aware of. This mathematical concept works only with accounts that receive compounding annual interest at lower rates.

The higher the rates go, the less accurate the results will be.

This principle doesn’t work with simple interest.

On the other hand, investors can slightly change the number, based on their annual interest rate. For example, some may use 69.3, or 73, depending on the percentage of their rate.

The Navexa portfolio tracker and reporting platform is a fast, accurate way to determine your annualized rate of return across shares, ETFs, cryptos, cash accounts and more. We handle all portfolio performance calculations behind the scenes so you can focus on better understanding your portfolio and returns.

Managing a complex portfolio and calculating cash dividends might be challenging. Here’s how it can be done with ease with a few formulas — and with the Navexa portfolio tracker.

Most people who consider investing are familiar with owning stocks. Some are also highly interested in receiving a dividend payout. Those who go deeper into researching an investment, might decide on purchasing stocks of companies because that pay cash dividends.

Dividends might help investors maintain a stable portfolio, remain invested in quality companies, and earn a profit, all while holding shares.

However, novice investors may find dividends confusing — especially when it comes to calculating their dividend yield per share.

The traditional way to calculate dividend per share is using the company’s income statement and similar reports. But, there are other, easier methods, too.

Dividends Explained

Cash dividends are payments companies make to shareholders from their profits.

A dividend is defined as a distribution of a company’s earnings or stocks to a class of its shareholders. Dividend payouts are determined by the board of directors, and shareholders receive them for as long as they hold the stock.

A dividend is a form of reward to shareholders for investing in the organization and for holding the stock. Dividends may also help a stock’s price remain relatively stable.

Some companies offer dividend payments and prefer to keep the shareholders satisfied. Others decide not to pay dividends, instead reinvesting profits back into the company.

Dividends are paid monthly, quarterly, or annually, depending on the company. They’re paid at a scheduled frequency, so investors always know when they’ll receive the profit from holding shares.

Receiving a dividend based is a great way to increase one’s income, but there’s more to it.

Shareholders also pay attention to other factors, such as dividend yield, rates, retention ratio, and other key numbers.

Dividend Rate vs Dividend Yield

The dividend rate is a percentage that shows how much the company pays in dividends annually, relative to its stock price. The dividend rate can be fixed or adjustable, and it’s expressed as a dollar figure.

The dividend rate is calculated with the following formula:

Dividend rate = dividend per share / current price

On the other hand, the dividend yield is expressed as a percentage, and shows the ratio of a company’s annual dividend payout, compared to its share price.

Shareholders can calculate the dividend yield by using the following formula:

Dividend yield = annual dividends per share / current share price x 100

Navexa helps share investors by calculating dividend performance automatically. Navexa’s app is easy to use, and tracks multiple types of investments. This includes tracking and reporting on cryptocurrency investments.

Dividend Payout Ratio vs. Retention Ratio

The dividend payout ratio shows how much of the company’s earnings after tax are paid to the shareholders. It’s in direct relation to the organization’s net income amount, and it’s used to measure the net income percentage.

It’s calculated by the following formula:

Dividend payout ratio = total dividends / net income

On the other hand, the dividend retention ratio represents the percentage of net income that the company keeps to grow the business, instead of paying it out to the shareholders as dividends.

It’s calculated by the following formula:

Retention ratio = retained earnings / net income attributed to stockowners

Calculating Dividends per Share and Earnings per Share

Dividends per share (DPS) is the number of stated dividends paid by companies for each of the shares outstanding. It represents the number of dividends each shareholder receives based on the shares they own.

DPS is often used to calculate dividend yield, and the formula goes as follows:

DPS = total dividends paid over a period – special dividend payout / shares outstanding

On the other hand, earnings per share (EPS) are useful in calculating how profitable the company is based on measuring the net income for each of the company’s outstanding shares.

EPS is also an important number used to determine share price.

EPS shows whether investing in a certain company and holding its shares would benefit the shareholders and improve their net income.

For example, if the company reports an EPS that’s below a certain estimate, that might cause its share prices to drop.

The formula for calculating earnings per share goes as follows:

EPS = net income – preferred stock dividends / outstanding shares

Types of Dividends

Four types of dividends include cash, stock, property, and liquidating dividend.

There are several types of dividends that a company may pay to the shareholders. These include:

Cash dividend

Stock dividend

Property dividend

Liquidating dividend

Cash dividends are the most common. They represent a simple distribution of funds to incentivize shareholders to hold their shares, improve the shareholders’ equity, and increase confidence in the organization.

What Are Cash Dividends?

Cash dividends represent money a company pays to the shareholders per share they own. The money can come from the organizations’ current earnings or accumulated profit. Cash dividends are paid regularly, usually by quarterly or annual payments.

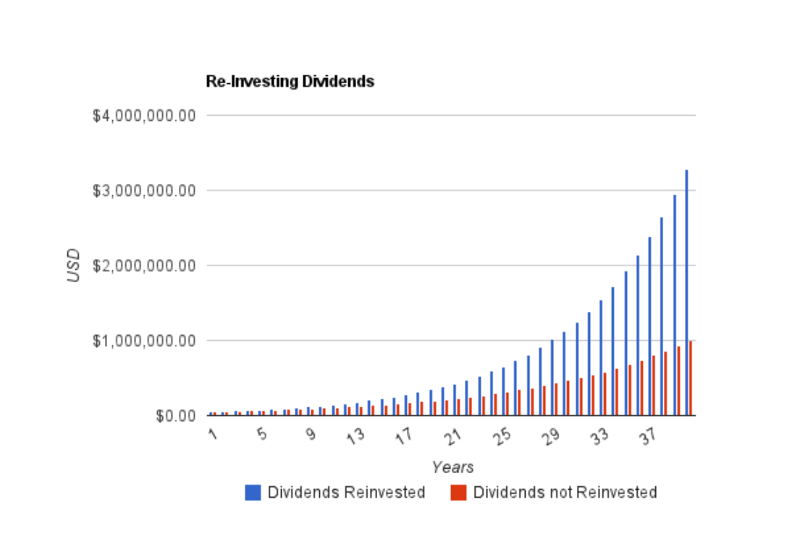

Once the shareholders receive this dividend, they may have the option to accept the cash payment, or reinvest in additional shares (known as a dividend reinvestment plan) and improve their position in the market.

The willingness of the company to pay cash dividends shows a solid financial strength, and positive performance, although that’s not always the case. Sometimes the companies may keep paying dividends, but still be in a poor financial position and eventually shut down.

This is why potential stock owners must be careful when investing and take everything into consideration before they invest in the organization.

Which Company Can Afford to Pay a Cash Dividend Yield?

Many companies have outstanding earnings, and can afford this form of dividend payout. These are just some of the companies that offer dividend payouts across the ASX, NASDAQ and NYSE:

IBM

AT&T

Johson & Johnson

QUALCOMM

Fortescue Metals Group

BHP

Magellan Financial Group

More experienced investors can easily determine which company has a solid income statement, and capital, which helps them invest in profitable shares. On the other hand, novice investors may struggle in finding the dividend shares worth investing in.

Potential stock owners must be careful when investing and take everything into consideration before they invest in the organization.

Still, investing in shares that pay these types of dividends can help both new and experienced investors increase capital.

Additionally, those who wish to invest often check out the company’s trailing 12 months (TTM).

This is a set of performance data that shows how the organization managed finances in the last year. TTM is beneficial for understanding a company’s growth and potential.

Example of a Cash Dividend Payout

Here’s a simple example of a cash dividend:

One investor owns 100 shares of company X. At the end of a quarter, the company X calculates its financial performance for that quarter.

The board of directors then reviews the information, and decides on a $0.50 dividend per share for the quarter.

This means that the investor is entitled to $0.50 x 100 shares = $50

How Does a Cash Dividend Work?

When a company earns enough, it may decide to distribute part of its earnings to the shareholders. This part of the earnings is most commonly distributed via cash dividends paid in regular intervals, usually quarterly.

While these dividends are a great way of motivating shareholders to stay with the company, they may cause the stock price to drop. Still, investors love companies that offer dividends, as they know they can count on regular payouts.

Why Does a Cash Dividend Matter?

There are many reasons these dividends are important to shareholders. For example, the cash dividends could signal whether the company has good financial health.

It may show that a company is more effective in using its capital, compared to companies that don’t pay dividends.

Dividend payment per stock also increases the chance of shareholders remaining invested in the stock. This means the company’s stock price may stay more stable.

Are Cash Dividends Better Than Stock Dividends?

When it comes to the cash dividend, shareholders have no other option but to either keep it, or reinvest it and increase the number of shares they own.

Even though these dividends are a more common way of paying shareholders, stock ones are sometimes considered better.

When it comes to the cash dividend, shareholders have no other option but to either keep it, or reinvest it and increase the number of shares they own.

With a stock dividend, they can keep the shares or turn them into cash. Plus, stock dividends aren’t treated as taxable, as they’re usually not turned into income.

The Advantages of Cash Dividends

There are many advantages of the dividend payout for shareholders. One of the main advantages is the steady income. These dividend payouts are regular, so shareholders know when they’ll receive the funds.

Regular payouts are especially beneficial for those who build a large portfolio with a view to living on the income.

Receiving dividend payments can also be a good way of establishing a market hedge. This defends the shareholders from the stock price dropping, which often happens during a bear market.

Furthermore, they know that companies that pay dividend yield may be more careful with their financial decisions, as they want to keep people invested in their shares.

The Disadvantages of Cash Dividends

While these types of dividends are common, and can yield great profit for investors, there are certain financial disadvantages for companies.

One of the major disadvantages to paying the dividend is that the money that’s paid to shareowners can’t be used to further develop the business. In a way, paying the dividend prevents the company from investing in increasing sales and profits. Instead, offering a healthy dividend might sustain or even raise the share price — effectively raising capital for the business.

When it comes to shareholders, dividend payments mean they’ll have taxable income. However, if an investor has an income that’s too low to make them liable for tax, they may be entitled to a refund from the Australian Taxation Office.

Do Cash Dividends Go on the Balance Sheet?

A balance sheet is a financial statement that involves the company’s stock, other assets, liabilities, and shareholder equity. This sheet is also used to evaluate the business.

Dividends do impact the balance sheet, as they will show a decrease in the company’s dividends payable, and financial balance. The balance will be reduced.

To check the total amount of paid dividends, investors should also use a financial statement. This statement shows how much money is entering and leaving the company.

Why Do Shareholders Prefer Cash Dividends?

According to financial theory, investors don’t care much about whether they’ll receive cash or stock dividends, for as long as they have the same value. However, this approach doesn’t include other complexities, such as taxes, transaction costs, dividend payout, demographic attributes of investors, etc.

On the other hand, the theory states that investors would pay additional expenses for receiving cash dividends, and they may prefer them over stock dividends.

Some shareholders would rather pay the taxes and receive cash for their outstanding shares, than receive additional stocks, simply because of direct financial compensation.

Accounting for the Cash Dividend

These forms of dividends are usually accounted for as a reduction of a company’s retained earnings. After the board of directors allows this type of dividend payout, the company debits the retained earnings account, and creates a liability account called ‘dividends payable’.

By moving funds to a dividends payable account, the company reduces equity, which is instantly shown in the company’s balance sheet even though no money has been paid out yet. This, in turn, increases liability.

Once the payment date comes, the company then reverses the dividend payable with a debit entry, and credits the cash account for the cash outflow.

In that way, these forms of dividends don’t actually affect the company’s income statement. Still, all companies that pay these dividends must report the payments in the cash flow statement.

Calculating Cash Dividend

Calculating the dividend payout for the given year is done by subtracting the retained earnings from the beginning of the year from the end-of-the-year numbers.

Based on the complexity of these types of dividends, potential stockholders may struggle in finding the appropriate information they can use to calculate the dividend payout. In general, companies report their dividends in a statement they send together with their accounting summary to their stock owners.

Some organizations share the date in press releases. However, that’s not always the case.

Those who can’t find this data officially, usually consult the company’s balance sheet, which can be found in the annual reports.