Thom Benny has worked in financial research & communications since 2013. He pursues his fascination with financial literacy, investing and economics as Communications Director at Navexa, a portfolio tracking platform for shares & crypto.

Warren Buffett has been in the markets longer than many investors have been alive.

In 1965, his Buffett Partnership Ltd. company acquired textile manufacturing firm, Berkshire Hathaway, and assumed its name as it transformed into a diversified holding company.

This diversified holding company is now among the S&P 500’s top 10 listings, and among the largest private employers in the United States. It’s class A shares have the highest public company per-share value on the planet.

Buffett’s investing and business success is objectively impressive.

Rather than throwing lavish parties in luxury mansions, or parading between red carpet events in bespoke supercars or megayachts, Warren keeps his lifestyle modest, preferring to let his investments — and their near six-decades of outperforming the S&P 500 by nearly 10% a year — do the talking.

But, the impressive performance charts and corporate filings aren’t the only way to observe Buffett’s brilliance.

Six decades of shareholder letters

When Buffett took control of Berkshire Hathaway in ’65, he started writing letters to the company’s shareholders.

Initially ‘signed off’ by other figures in the business, Buffett eventually started publishing in his own name, building a (so far) near six-decade body of writing covering a huge range of markets, events and ideas in his now-signature friendly, casual tone.

You can read the 1965 letter (pictured below) here.

Wall Street Journal writer, Karen Langley, recently started with the letter above and went all the way — reading every single shareholder letter Warren has ever written.

Here’s six of the best excerpts:

Six of Buffett’s best investing ideas

1: Fear & greed as ‘super-contagious diseases‘ — 1987

‘Occasional outbreaks of those two super-contagious diseases, fear and greed, will forever occur in the investment community. The timing of these epidemics will be unpredictable. ‘And the market aberrations produced by them will be equally unpredictable, both as to duration and degree. Therefore, we never try to anticipate the arrival or departure of either disease. ‘Our goal is more modest: we simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.

2: Watch the playing field, not the scoreboard — 1992

‘It’s true, of course, that, in the long run, the scoreboard for investment decisions is market price. But prices will be determined by future earnings. ‘In investing, just as in baseball, to put runs on the scoreboard one must watch the playing field, not the scoreboard.‘

3: A ‘really long-term example‘ — 2006

‘It’s been an easy matter for Berkshire and other owners of American equities to prosper over the years. ‘Between December 31, 1899, and December 31, 1999, to give a really long-term example, the Dow rose from 66 to 11,497…. This huge rise came about for a simple reason: Over the century American businesses did extraordinarily well and investors rode the wave of their prosperity,‘

4: The power of price on perspective — 2012

‘The first law of capital allocation — whether the money is slated for acquisitions or share repurchases — is that what is smart at one price is dumb at another.‘

5: Bubbles, wisdom & folly — 2012

‘Over the past 15 years, both Internet stocks and houses have demonstrated the extraordinary excesses that can be created by combining an initially sensible thesis with well-publicized rising prices. ‘In these bubbles, an army of originally skeptical investors succumbed to the ‘proof’ delivered by the market, and the pool of buyers — for a time — expanded sufficiently to keep the bandwagon rolling. ‘But bubbles blown large enough inevitably pop. And then the old proverb is confirmed once again: ‘What the wise man does in the beginning, the fool does in the end‘.‘

6: What to do when the skies rain gold — 2017

‘Charlie and I have no magic plan to add earnings except to dream big and to be prepared mentally and financially to act fast when opportunities present themselves. Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it’s imperative that we rush outdoors carrying washtubs, not teaspoons.’

‘The Architect of Berkshire Hathaway’

That last excerpt refers, of course, to the late Charlie Munger, vice chairman of Berkshire Hathaway, who passed away in 2023.

Buffett referred to Munger as ‘The Architect of Berkshire Hathaway’, and credited him with shaping not just the company, but Buffett’s whole way of viewing business and the markets.

Berkshire Hathaway reported a profit of $96.2 billion for 2023. The company ended the year with a record $167.6 billion in cash, prompting plenty of speculation from commentators on what, if anything, Buffett’s now-colossal firm might do with it.

For context, $167.6 billion is more than enough to buy Nike, Morgan Stanley, Boeing, BlackRock, Airbnb, or Sony, among other huge firms.

Quote of the week

‘In my whole life, I have known no wise people… who didn’t read all the time. ‘You’d be amazed at how much Warren reads, at how much I read. ‘My children laugh at me. They think I’m a book with a couple of legs sticking out.‘

— Charlie Munger

That’s it for this week’s The Benchmark email.

Forward this to anyone you know who needs to read it.

And, if one of our awesome subscribers has forwarded it to you…

Subscribe here for weekly emails with ideas, stories and content about long-term, high-performance investing!

All information contained in The Benchmark and on navexa.io is for education and informational purposes only. It is not intended as a substitute for professional financial or tax advice. The Benchmark and any contributors to The Benchmark are not financial professionals, and are not aware of your personal financial circumstances.

We all like to marvel at lines that go up and to the right.

But what’s most interesting about this one — the Bridgewater Pure Alpha 1 fund’s performance between 1991 and 2015 — is how it ends up pretty much where the S&P500 does…

Without the massive falls in 2000 and 2008.

While stocks were tumbling amid the two bloodbaths…

Ray Dalio’s investors were making money.

That’s what qualifies this man to lecture the rest of us on what the economy is, how it behaves, and why.

Long-term productivity growth, with the short and long-term debt cycles overlaid.

As you’ll see in the video, there’s three key factors you need to understand:

Productivity Growth: Over time, we become more productive and raise our living standards.

Short-Term Debt Cycle: At the consumer level, our borrowing and deleveraging generally moves in ~6-year cycles.

Long-Term Debt Cycle: At the broader economic level, society’s borrowing and deleveraging generally happens in ~75-year cycles.

According to Ray, both the 1929 ‘Great Depression’ and the 2008 ‘Great Recession’ both marked the beginning of ‘deleveraging’ phases on the long-term debt cycle.

Understanding this fundamental economic truth was what allowed Bridgewater’s Pure Alpha 1 to effectively dodge the 2008 crash.

If the market is really this easy to predict, where are we now?

Ray Dalio is not only one of the wealthiest people on the planet, financially speaking.

He’s also — I would argue — one of the wealthiest in terms of his knowledge and understanding of the financial world.

(And, as we like to remind you in The Benchmark, knowledge pays the best interest.)

Ray is about as on the money as one can get about the fundamental nature of the economic world we live in.

Here are some comments he made in 2023:

‘In my opinion the tightening that began in March 2022 ended the last paradigm in which central banks gave away money and credit essentially for free, which was great for the borrower-debtors. ‘We are now in a new paradigm in which central banks will strive to achieve balance, in which real interest rates will be high enough and money and credit will be tight enough to satisfy lender-creditors without interest rates being too high and money and credit being too tight for borrower-debtors.’

Dalio: 2024 a ‘pivotal year’

Ray’s January Principled Perspectives newsletter is a deep dive (an actual deep dive, not just another blog or email claiming to be) into how he sees these economic cycles playing out in the world.

It’s well worth a read, if you have the time and intellectual energy to absorb some very big ideas.

Here’s why:

‘2024 will almost certainly be a pivotal year in a number of ways— for example, we will find out whether the existing democratic order in the US will or won’t hold up well, and whether or not the world’s international conflicts will be contained. ‘Of course, like all years, 2024 and the events in it will be just small parts of the long string of years and events that make the Big Cycle arc of history, which is what is most important to pay attention to.’

All information contained in The Benchmark and on navexa.io is for education and informational purposes only. It is not intended as a substitute for professional financial or tax advice. The Benchmark and any contributors to The Benchmark are not financial professionals, and are not aware of your personal financial circumstances.

How, exactly, does Morgan Stanley recommend readers of its sage wisdom act on these bleak observations?

‘Balance expectations and portfolios by buying the equal-weighted S&P 500 Index or actively favoring value-style stocks, with a focus on financials, industrials, utilities, consumer staples and healthcare.’

Basically, buy the market, or buy a bunch of stocks from those five sectors.

In this email, we’re going to do two things:

First, let’s check in to see how markets are tracking since setting off from Morgan Stanley’s ‘precarious point’ on January 1.

Second, we’ll show you a few pieces of information that help long-term investors avoid getting caught up, bogged down, or bothered by reports such as that outlined above.

Stocks in 2024: The story so far

So far, four months into 2024, Morgan Stanley’s predictions of ‘an average year for markets’ appear to be wide of the mark.

The S&P 500: Up 7.5%

Source: Google Finance

NASDAQ 100: Up 7.8%

Source: Google Finance

Of course, these performance charts in no way tell us what might come next for the S&P 500 and the NASDAQ.

But, consider this:

Going down while going up (and vice versa)

Ben Carlson is the Director of Institutional Asset Management at Ritholtz Wealth Management (who manage about $2.5 billion of client capital).

In his post, he makes the case that investing is pretty much always confusing in the short term.

Even when stocks are trending higher, they can and do crash lower, or ‘draw down’.

Equally, when stocks are trending down, they can produce short-term price increases.

Ben also notes that since 1928, the S&P 500 has gained 20% or more in a year 34 times.

That’s 35% of the years up to and including 2023.

Of those 34 years, the index has corrected by 10% or or more in 16 of them.

In other words, nearly half the S&P 500’s strongest annual performances include a double-digit correction/drawdown.

Here’s the proof:

In Ben’s words:

‘Risk and reward are attached at the hip when it comes to investing. One of the reasons the stock market provides such lovely returns in the long-run is because it can be so darn confusing in the short-run. ‘You don’t get the gains without living through the losses.’

We’ve written before in The Benchmark about so-called ‘dangerous short-termism‘ — the phenomenon that makes people, and investors, struggle to see beyond events and concerns that are immediately in front of them.

What Ben Carlson writes about living through the losses to get the gains, this next chart illustrates (over the much longer term).

Here’s the Dow Jones Industrial Average from 1915 to March, 2024:

As you can see, the index’s 2,217% return over the more than 100 years has not come without multiple massive crashes and downtrends.

The Great Depression crash and the protracted bear market in the 1970s stand out as the most dramatic drawdowns.

If you’re a newer investor, and you’re yet to develop the long-term view common to history’s most successful and wealthy investors, annual market forecasts like Morgan Stanley’s might scare you.

But as Ben Carlson shows, billionaire Kenneth Fisher’s statement that ‘time in the market beats timing the market‘ is a good general approach to the stock market.

Before we hammer on the point too much (although I’d argue it’s always worth considering such proof and observations, especially when dealing with difficult ‘drawdown’ episodes along the way), here’s one last visual for your consideration:

This one’s from Long Term Mindset writer Brian Feroldi:

Decades > Years > Months > Days

Morgan Stanley and other Wall Street firms can predict, forecast and prognosticate all they want about what the market might or might not do.

But the reality is — for those looking to build wealth in the markets over the long term, at least — that what happens this month, or even this year, is of little relative consequence when you have your sights set on a bigger picture far beyond the short or medium-term horizon.

With ups come downs, and as Ben Carlson says, risk and reward are joined at the hip.

That’s it for this week’s The Benchmark email.

Forward this to anyone you know who needs to read it.

And, if one of our awesome subscribers has forwarded it to you…

Subscribe here for weekly emails with ideas, stories and content about long-term, high-performance investing!

All information contained in The Benchmark and on navexa.io is for education and informational purposes only. It is not intended as a substitute for professional financial or tax advice. The Benchmark and any contributors to The Benchmark are not financial professionals, and are not aware of your personal financial circumstances.

Senior journalist and MIT Technology Review contributor Richard Fisher has been studying how humans perceive time.

Just as a child grows from only being able to imagine tomorrow, or next week, to eventually grasping the idea of not only their own life, but the distant past and distant future either side of it…

The whole human species’ sense of time has evolved with our civilization.

‘While we may have this ability, it is rarely deployed in daily life. If our descendants were to diagnose the ills of 21st-century civilization, they would observe a dangerous short-termism: a collective failure to escape the present moment and look further ahead.

‘So often it’s a struggle to see beyond the next news cycle, political term, or business quarter.’

The ‘short-termism’ Fisher notes is, of course, very much present in the investment world.

With their capital at risk, investors easily fall prey to a market’s daily, or weekly, or monthly volatility.

You don’t have to look far to find someone who sold early — or didn’t buy in the first place — because they fell into ‘dangerous short-termism’ instead of stepping back and trying to see the big picture.

Meanwhile, the big picture, long-term thinkers position themselves on the other side of such decision making.

As the king of long-term benchmark outperformance, Warren Buffett, says:

‘The stock market is a device for transferring money from the impatient to the patient.’

The market’s next year decade

In the spirit of highly-evolved, long-term thinking, let’s consider the idea of the ‘secular bull market’.

‘A secular bull market is a market that is driven by forces that could be in place for many years, causing the price of a particular investment or asset class to rise or fall over a long period. In a secular bull market, positive conditions such as low interest rates and strong corporate earnings push stock prices higher.

‘In a secular bear market, where flagging corporate earnings or stagnation in the economy leads to weak investor sentiment, stocks experience selling pressure over an extended period of time.

The idea here, is that there are short and long-term cycles in markets.

And if, as Buffett says, the stock market transfers money from the impatient to the patient, surely it pays to know about these long term ‘secular’ markets, right?

Take a look at this:

On the chart above, you can see the S&P all the way back to the 1920s.

Zoomed out that far, you can see the argument for ‘long-term secular trends’ in the stock market.

The argument basically goes that over the long term, the US stock market moves through periods of expansion and contraction that last about 16 to 18 years.

Viewed through this lens, you can make two observations:

First, there have only been two secular bull markets since the 1920s — one in the 1950s and 1960s, and another in the 1980s and 1990s.

Second, those ‘expansionary’ periods preceded periods of contraction, which you can see marked by red text.

These are inflationary or deflationary periods where stocks basically grind sideways over the long term.

The last two contraction periods for the market occurred from the mid 1960s until the early 1980s and from the late 1990s to about 2014.

So going by the chart, we’re in a secular bull market right now.

Could stocks rise for the next 10 years?

Some of the most experienced investors and fund managers on the planet right now certainly think so.

Robert Sluymer has been analyzing and forecasting financial markets for some of the largest institutions in the world for more than 30 years.

Late last year, he went on record with his prediction for where the S&P500 — the biggest in the world — is headed in the next decade.

‘The long-term secular trend for US equity markets remains positive with an underlying 16 to 18 year cycle supportive of further upside into the mid 2030s, potentially to S&P 14,000.

‘The S&P could move toward 14,000 by 2034 which is when we expect the current 16 to 18 year secular bull cycle to peak.’

Bank of America technical strategist, Stephen Suttmeier, has a similar take:

‘The secular bull market breakouts from 1950, 1980 and 2013 suggests that the S&P 500 can spend much of 2024 north of 5,000. This corroborates bullish pattern counts for the S&P 500 near 5,200 and 5,600, respectively.’

This chart shows the 1950 and 1980 secular bull markets with the 2013 (current) one overlaid:

‘Patience is bitter…’

‘Patience is bitter, but its fruit is sweet.’ So said Swiss political philosopher Jean-Jacques Rousseau.

This email is not arguing for or against the view that the stock market is going to rise for roughly the next 10 years.

The point is that, either way, taking a step — or a few steps — back from the day-to-day behaviour of the stock market can give you a fresh perspective and appreciation for time.

Take a look at this chart, showing the number of times the media called the top of the market between 2009 and 2017:

Nine times, these publications claimed ‘the easy money has already been made‘. And all nine times, stocks kept climbing.

As Richard Fisher observes, it’s the more highly developed and evolved among us who can grasp the bigger picture and appreciate timescales beyond ‘dangerous short-termism‘.

And if, as Buffet says, the market merely moves wealth from the impatient to the patient…

Then perhaps it’s useful to make sure we’re among the latter, rather than the former.

Now…

You’re still reading, so I’m going to presume you found this email useful, or interesting, or maybe even both.

If that is the case, it would make our day if you’d help us make someone else’s — forward this email on so we can share The Benchmark with more great readers.

All information contained in The Benchmark and on navexa.io is for education and informational purposes only. It is not intended as a substitute for professional financial or tax advice. The Benchmark and any contributors to The Benchmark are not financial professionals, and are not aware of your personal financial circumstances.

You’re reading this because you joined the Navexa mailing list.

Which means you have, at the very least, a passing interest in investing, the markets, and building wealth.

Which means that — we hope — you’ll find this email informative and entertaining.

Here’s why:

Mission statement

‘An investment in knowledge pays the best interest,‘ as Benjamin Franklin said.

That statement sums up why we’ve launched this email.

Each week, we’ll write to you with stories, ideas and content that offers some insight and/or perspective to what’s happening in the markets and the wider investing world.

These will include (but not be limited to):

Stories about the history of money, wealth and economics.

Notes on current events moving markets.

Interviews with our global network of HNW investors, traders, analysts and digital asset pioneers.

Analysis & comparisons of investment strategies

Answers to your questions

The Benchmark will not be making investment recommendations, nor providing financial advice.

Our aim is to provide investing knowledge that ‘pays interest’.

While this isn’t an investing email for beginners, necessarily, we should start with some basics.

And it doesn’t get much more basic than why we invest in the first place.

Check out this post:

The case for investing, in starkly simple terms.

If the idea that investing is essential to building real wealth, as Willy Woo so clearly shows, resonates, then this email is for you.

But, hang on a second.

Why The Benchmark?

This is why:

From 1965 to 2023, Warren Buffett has achieved an annualized return of 19.8%.

Compare that to the S&P 500 index, which has returned 10.2% a year.

Buffett has ‘beaten the benchmark’ by 9.6% for nearly six decades.

That might not sound like much to the average, short-term thinking, investor.

But let’s take a look at what that delta means in dollar terms.

The S&P 500’s 10.2% annualized return turns a $100,000 investment into just shy of $28 million.

Not bad right?

Most of us wouldn’t turn our noses up at that prospect.

But what about the Oracle of Omaha?

Well, the result of his 9.6% outperformance over those 58 years probably have something to do with the look on his face in this photo:

Warren ‘The Benchmark Beater’ Buffett

Because 19.8% a year, for 58 years, turns $100,000 into more than $3.5 billion.

Even with six decades of inflation accounted for, that’s still an exponentially larger sum than $28 million.

That 9.6% outperformance, over that timeframe, amounts to the $3.2 billion difference.

In other words, consistent long-term outperformance has exponential, real-money, consequences.

That’s why we invest in the first place.

It’s why we built the Navexa portfolio tracker.

And it’s why we’ve launched The Benchmark — to deliver ideas, stories and perspectives that will help you become a more effective and complete investor.

Quote of the week

‘Money does not buy you happiness, but lack of money certainly buys you misery.’ — Daniel Kahneman

The headline for this email comes from the late Daniel Kahneman, who died earlier this year. Daniel’s book, Thinking, Fast and Slow, released in 2011, was the culmination of a life spent exploring human decision making.

He won the Nobel memorial prize in economics in 2002 ‘for having integrated insights from psychological research into economic science, especially concerning human judgment and decision-making under uncertainty‘.

What now?

Next week, we’ll dive into the stock markets, exploring where they’ve been, where they’re at, and where they’re (possibly) going.

If you enjoyed this email and you’re looking forward to the next one, then be sure to whitelist us in your inbox, and, if you have a spare five seconds, send us a quick reply with any questions or comments you have for The Benchmark.

All information contained in The Benchmark and on navexa.io is for education and informational purposes only. It is not intended as a substitute for professional financial or tax advice. The Benchmark and any contributors to The Benchmark are not financial professionals, and are not aware of your personal financial circumstances.

In October 2023, we unveiled a major new update to the Navexa Portfolio Tracker. Here’s an explainer on the key changes.

Navexa started life as a basic portfolio tracking tool. Today, it’s developed into a multi-asset, multi-market platform that gives investors professional-level portfolio tracking and analysis on a level no other tool can match.

In October 2023, we launched the most advanced iteration of Navexa to date. In this post, we explain the changes and walk you through a few of the powerful new tools we’ve created to make understanding and optimizing your investments easier than ever before.

Watch our Navexa 3.0 Webinar

We revealed and explained the latest iteration live on a webinar for our customers. Watch the replay free — just click the player:

Navexa 3.0: The Philosophy Behind The Redesign

Navexa started life in 2018 as a basic portfolio tracking tool. It quickly evolved, supporting more markets and offering more solutions to the all-too-common problems investors encounter trying to accurately track and analyze their long-term investment performance.

Today, we’re shedding our reputation as ‘another portfolio tracker’ and revealing four big new changes and additions to our platform.

Here, we introduce and explain the key new tools and updates, and show you why Navexa now offers performance tracking and portfolio analysis tools distinctly different from other platforms.

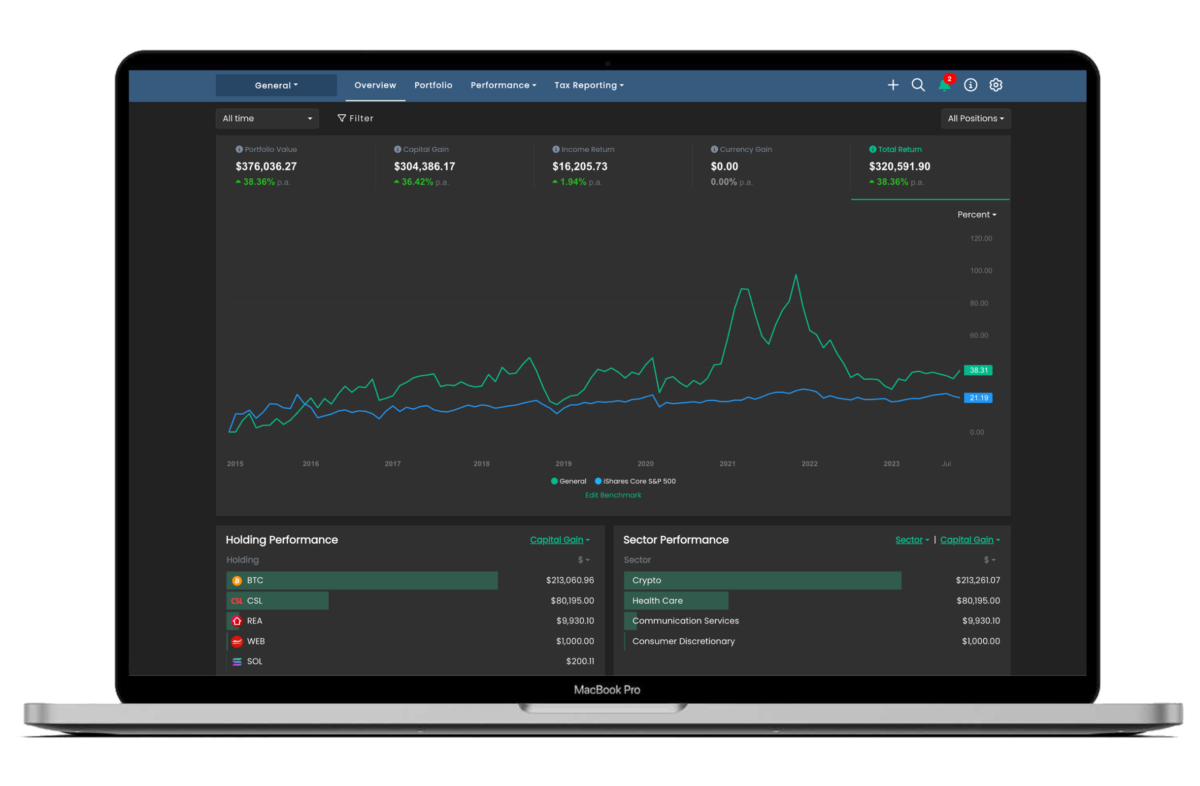

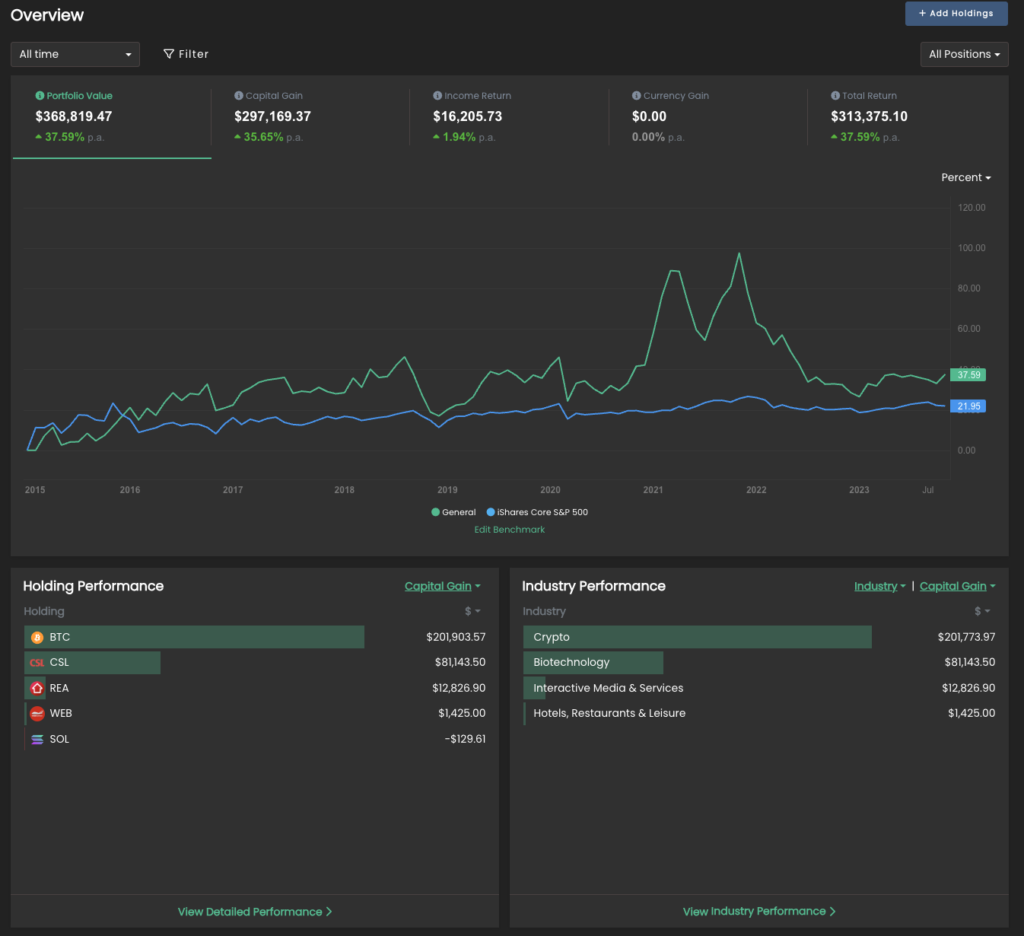

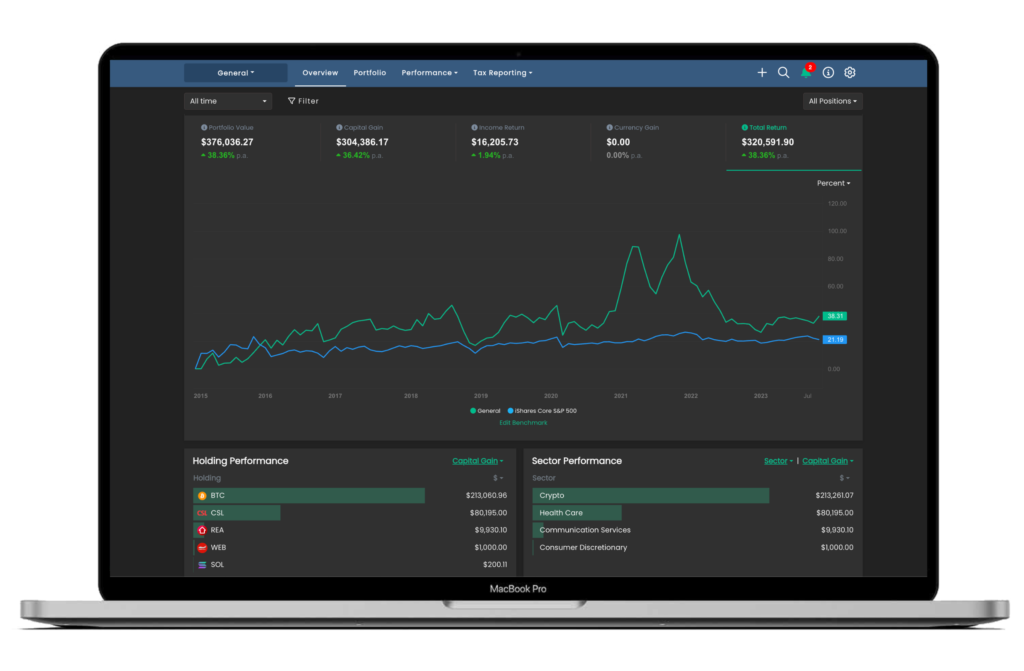

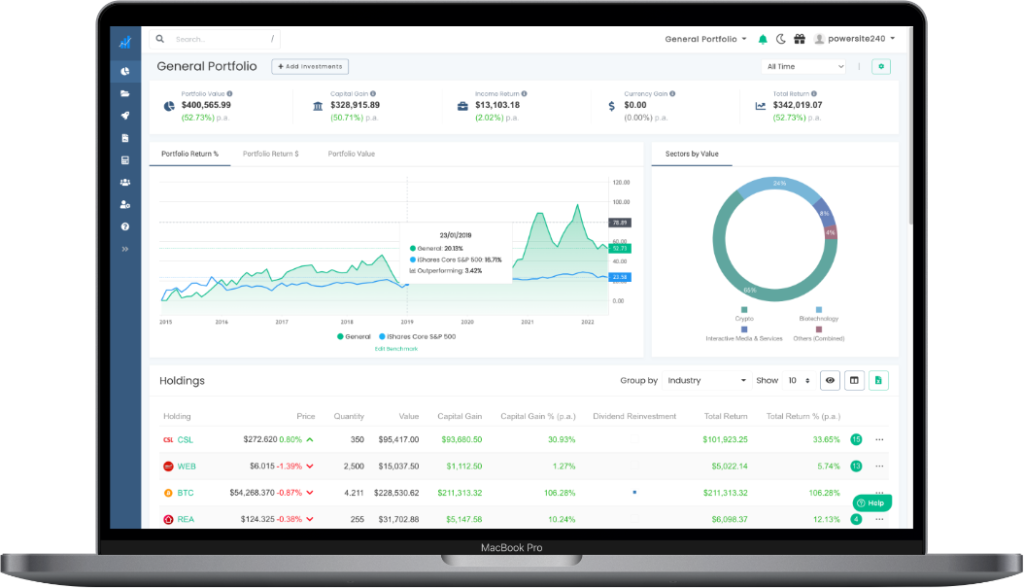

New: Portfolio Overview Screen

The most visible update we’ve made to Navexa is the new Overview screen:

The idea behind this screen is that investors can see all their key portfolio performance metrics at a glance in one place.

While previously (and on other platforms) you needed to visit different parts of your account to find everything you might need to know, the new overview is effectively a one-stop shop for checking your portfolio’s vitals.

The five key metrics at the top of the chart (value, gain, income return, currency gain and total return) are now clickable — clicking each will display a chart for that specific metric.

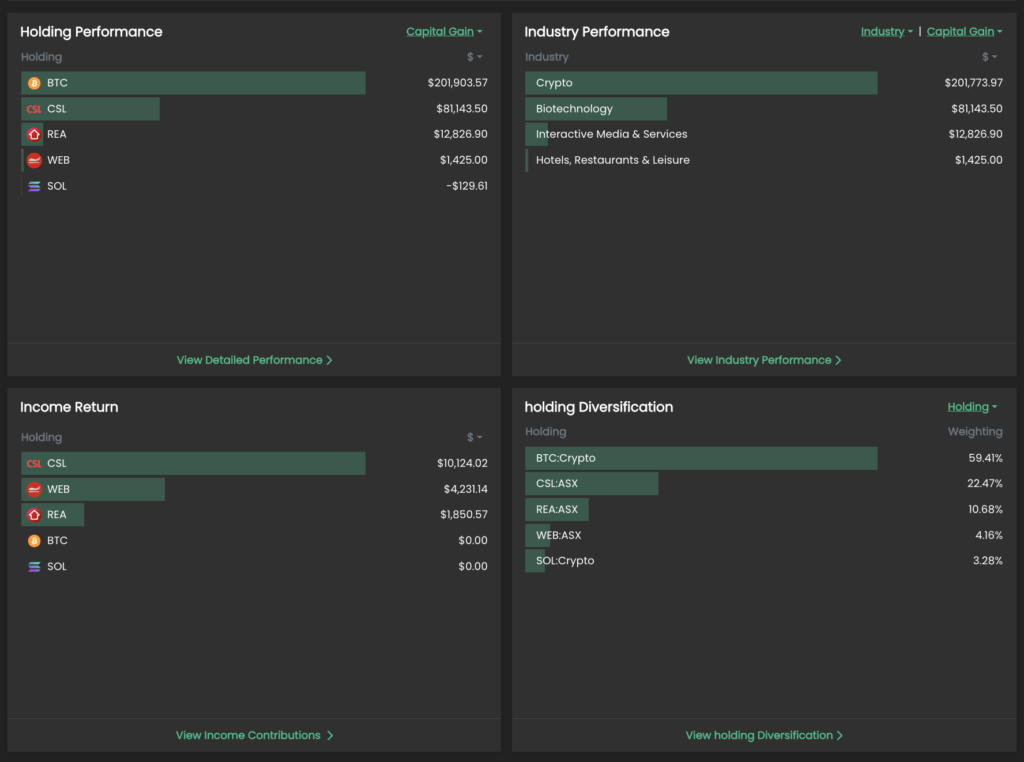

Below the chart, you’ll find four bar chart panels.

Clockwise from top left:

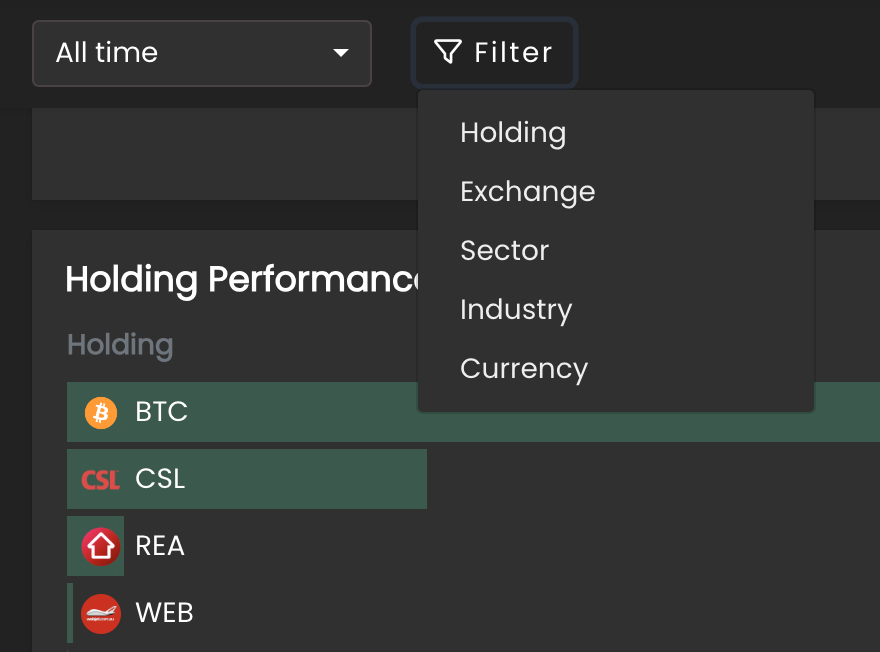

Holding Performance: A list of the top performing holdings in the portfolio.

Category Performance: A list of the top performing sectors in the portfolio.

Diversification: Select from holding, exchange, sector, industry and currency to view the portfolio’s diversification.

Income Return: A list of the highest income-earning holdings in the portfolio.

The first three panels all have clickable dropdown menus. You can customize what they show, like return, value, dollar or percentage.

This screen lets you both understand your portfolio performance at a glance, and allows you to drill down into greater detail. Just click the bottom of each panel to access the corresponding report based on your settings.

New: Filtering System

A key tool in Navexa 3.0 is the filter system.

This small, but powerful, tool allows you to ‘filter’ what you view throughout your account.

Click it and select from the dropdown (holding, exchange, sector, industry, currency). This will prompt you to make a selection.

Once you choose your filter, your account will reload, and all the charts, metrics and reports will apply only to your selection.

Note: Your filter selection remains as you move throughout your account — you’ll see it above the chart, and can click the ‘X’ to remove it and revert to an unfiltered view.

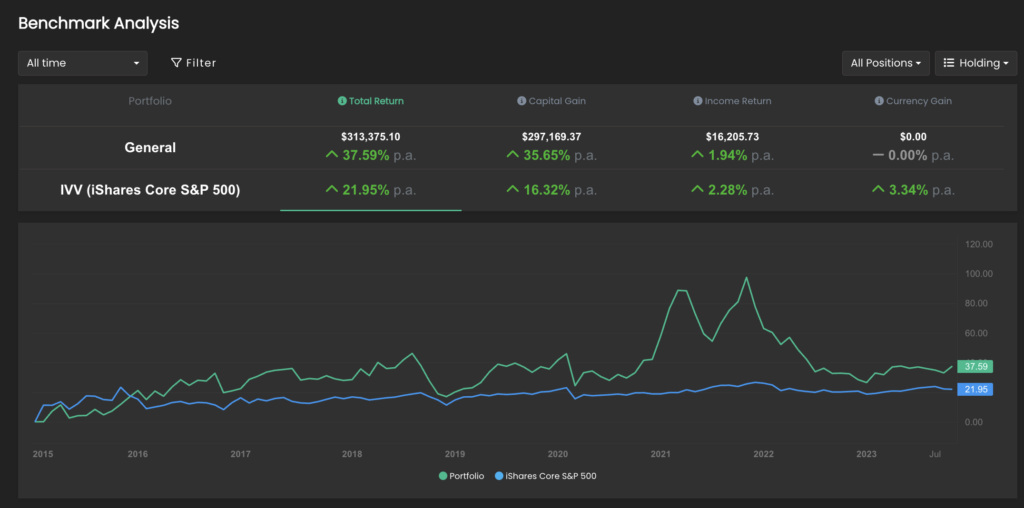

New: Benchmark Analysis

You’ve long since been able to choose your portfolio performance benchmark in Navexa.

But whereas previously, this was a simple addition to the main portfolio performance chart, we’ve now created a new Benchmark Analysis page:

Like the Overview screen, the Benchmark Analysis chart features clickable metrics along the top. Click each to view the corresponding performance chart and benchmark chart together.

You can edit the benchmark both on this page and on both the Overview and Portfolio screens.

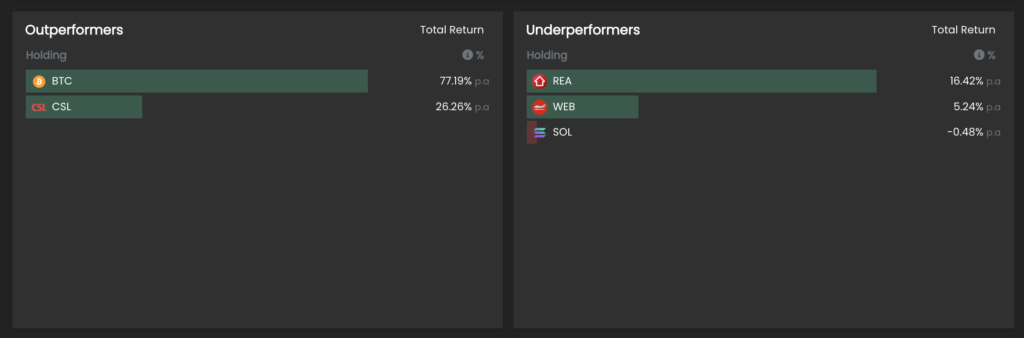

Below the chart, you’ll find two panels with bar charts:

These display which holdings (or sectors, exchanges, currencies, or industries) are overperforming and underperforming relative to your selected benchmark.

New: Income Calendar

We have another cool new tool for you — the Income Calendar.

Where previously Navexa could only forecast confirmed upcoming dividends, the new Income Calendar lets you estimate portfolio income 12 months in advance.

The solid coloured bars represent confirmed income, and the shaded bars represent predicted, or forecast, income.

Navexa calculated the predicted income based on the previous year’s earnings.

Below the chart, you’ll see a list of holdings and income ordered by date.

More New Stuff: Charts, cash account options & more!

We have left no stone unturned in this latest big upgrade.

You’ll also now find a Sankey chart for analyzing your portfolio income, the option to rename cash accounts, a slew of UX improvements (like labelling, and switching between showing open or closed positions).

Navexa 3.0 is live now — start tracking today!

Ready to start tracking and analyzing your portfolio?

In this post, we profile 16 of the best investing, personal finance blogs and podcasts (and YouTube channels) you’ll find on the web in 2022. Whether you’re new to personal finance and investing, or you’re looking for advanced economic analysis and trading content, these podcasts, blogs and channels will build your knowledge and financial literacy.

There’s never been more content about investing, personal finance, money management and financial independence than there is today.

As you’re reading this, thousands of content creators and journalists around the world are producing and publishing content aimed at helping you better understand personal finance, the markets and the deeper economic forces that drive them.

I’ve been in the financial research and publishing world for more than a decade. I’ve read, watched and listened to a lot of posts, videos and podcast episodes on investing, trading, personal finance and financial independence.

There are plenty of fantastic finance podcasts and blogs out there for those learning about everything from how to get started investing, or saving money, through to more advanced areas like options trading, portfolio management and macroeconomic theory.

But, as with most topics in this content-saturated era we’re living in, there’s also a lot of junk — clickbait content that promises fascination but turns out to not really say much at all.

That’s why I’ve put this post together. The 16 podcasts, blogs and channels I profile here are, in my and the Navexa team’s experience, some of the best investing and personal finance blogs and podcasts out there today. From deep economic analysis to business news, interviews with the world’s wealthiest investors and model portfolios designed to uncover once-in-a-lifetime investment ideas, these shows and websites span the spectrum of expertise.

Presented in no particular order.

#1: Chat With Traders — Pro Traders Share Their Stories

Professional trader Aaron Fifield launched the Chat With Traders podcast in 2015. Each podcast episode takes the form of a long conversation between the host and the guest — a billionaire fund manager, legendary options trader, a strategy specialist, or other industry expert.

These interviews are deep explorations that dive into what drives and motivates pro traders, what they’ve learned in their journey, and how they apply their knowledge to making money.

The CWT podcast is definitely not for beginners. While some of the ideas and principles you’ll learn in these episodes are universal and useful to investors of every level, you probably want to have a high degree of prior knowledge of trading (as opposed to investing) to get the most out of it.

I recommend podcast episode 214 with professional trader, James King, who shares four principles that drive elite performance.

Chat With Traders has some great free resources available.

#2 Equity Mates — An Aussie Investing Podcast Ecosystem

You can’t find an investing or finance podcast in Australia without stumbling upon Equity Mates. Founded in 2017, university mates Alec and Bryce created Equity Mates as a means to share their journey into investing and wealth building. They felt that ‘financial markets were seen as complex and inaccessible and financial media catered to the industry but not everyday Australians’.

The content you’ll find on the Equity Mates podcast and blog today is very much the opposite of industry-centric. Now spanning nine podcasts, online courses and even the FinFest live event, Equity Mates has expanded to cover a huge range of personal finance and investing content.

From the original Equity Mates Investing Podcast to Crypto Curious, Get Started Investing and more, there’s pretty much something for investors of almost every level to learn here. Thanks to their rise to prominence in Australia’s investing podcast world, Equity Mates now pulls some high-profile guests on its shows, too.

Check out this podcast episode, in which the Head of Research & Portfolio Management at InvestSmart, Nathan Bell, shares his 2, 4, 6 rule of portfolio construction.

EquityMates offers an ecosystem of podcasts, blog content & investing resources.

#3 Equity ASA: Short & Sharp Podcast Episodes For Australian Investors

The Australian Shareholders Association has been around since 1960. It’s a membership-based association that represents retail shareholders. The ASA ‘safeguards shareholder interests in Australian equity capital markets, helps its members to improve investment knowledge and fosters a connected retail investor community’.

Navexa has worked with the ASA several times, presenting webinars on portfolio performance tracking and delivering a live presentation on financial democratization at the 2022 ASA conference in Melbourne.

A more recent part of the ASA’s offering is its podcast series presented by the brilliant Phil Muscatello. Phil has his own podcasts, which I’ll get to shortly, but he still finds the time to front the ASA’s Equity Podcast.

The podcast takes the form of brief, varied interviews with guests ranging from portfolio managers and financial research houses to algorithmic traders and precious metals experts.

Each podcast episode seeks to inform the listener about a different aspect of the financial industry, and grant access to some of the most influential and experienced people on behalf of ASA members.

Equity ASA is the Australian Shareholders’ Association’s official podcast.

#4: Shares For Beginners — The Jargon-Free Investing Podcast

Our podcast episode discusses the pros and cons of the modern, app-first investment world and, of course, goes into the reasons why we’ve developed a portfolio tracking platform that allows investors to track all their investment performance in a single account.

But more broadly, the Shares For Beginners podcast is what is says it is — a great place to get into the ideas and concepts around investing without a huge amount of prior knowledge.

Phil’s effortless, casual podcast presentation and interview style does away with jargon and industry-speak in favour of easy-to-digest conversations with guests from fintech startups (us) to hedge fund managers, private investors, psychologists, even the editor-in-chief of Investopedia.

The episodes and topics are wide ranging, and you can be sure to learn something from pretty much any of the short, sharp episodes you dive into.

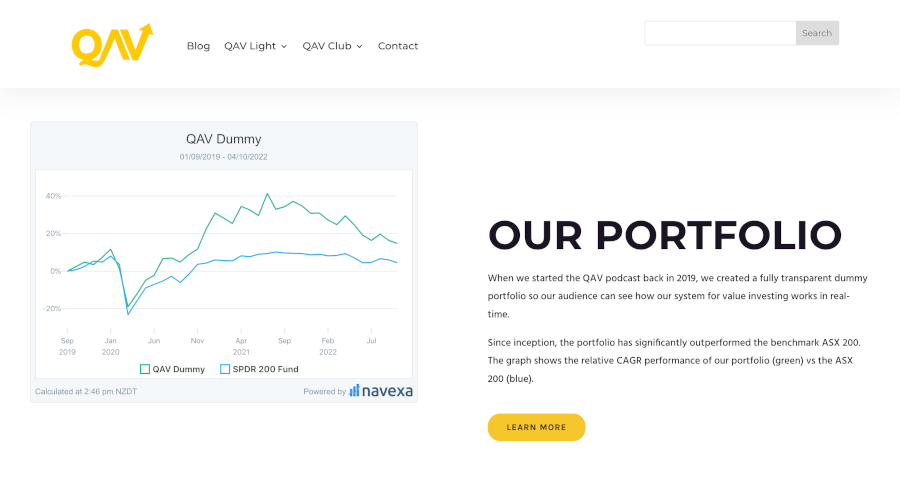

#5: QAV Podcast — Dedicated Value Investing Content

While I’m on the subject of finance podcasts we’ve appeared on, I should mention the small, but growing (and loved by its audience) Quality At Value Podcast.

Started by investors and friends Cameron Reilly and Tony Kynaston, QAV is a podcast, blog and membership club for value investors. The episodes and content centre on Tony’s impressive history as a long-term value investor.

Tony has achieved an annualized return of around 19.5% for the 30 years he’s been investing in the markets. That’s a seriously strong performance.

In the QAV podcast episodes and content, Tony and Cameron dive into all thing value investing. Specifically, they share Tony’s wealth of experience and the specific rules he’s created to spot winning stocks over his impressive 30-year run in the markets.

Navexa provides the QAV team with performance tracking for their model portfolio — which at the time of writing is outperforming the SPDR 200 benchmark by more than 10%.

The QAV podcast features Tony Kynaston, who has made a 19.5% annualized return over a 30-year value investing career.

#6: New Money — Top Quality Investing YouTube Channel

You shouldn’t, in my opinion, restrict your personal finance and financial education content consumption purely to podcasts. In the past few years, YouTube has produced a new generation of content creators spanning personal finance, investing, financial freedom, financial independence and so on.

Search ‘invest like the best’ or ‘financial freedom’ on YouTube and you’ll find hundreds of videos on everything from opening a crypto exchange account, to real estate investing, personal finance and beyond.

Of course, not all of it is great personal finance content. There’s no shortage of clickbait videos by blinged-out teenagers promising to reveal the secret to owning three Teslas before you have a driver’s license.

But dig a little deeper, and you will find some truly top-notch channels, like New Money, an investing and markets-focused show led by Australian Brandon Van Der Kolk. Brandon’s videos are about 10-20 minutes long.

They focus on topics like what stocks Warren Buffet and Berkshire Hathaway are buying and selling, how to understand key economic indicators and predictions, and — my personal favourite — deep dives into Dr. Michael Burry’s enigmatic tweets.

There’s a lot to learn here. The content is entertaining, easy to understand, and useful for investors whether they’re new to the markets or already years into their investing journey.

#7: We Study Billionaires — Wealth Hacking The World’s Best

So far I’ve kept the list local to Australia. But of course, you can’t dive into the world of investing — or investing and personal finance podcasts — without looking to the biggest market in the world, the US.

We Study Billionaires is a podcast on The Investor’s Podcast Network. Hosted by Danish investor, author and former professor Stig Brodersen and veteran CEO Trey Lockerbie, this show does what it says in the title.

The duo study, discuss and interview some of the wealthiest and most influential investors and businesspeople on the planet to learn the key factors and lessons in their success.

We Study Billionaires podcast features Warren Buffett, Howard Marks, Bill Gates and plenty of other high-calibre guests. There’s fresh episodes every week, plus the brilliant starter packs you can use to get up to speed on key topics fast.

We Study Billionaires is a podcast that seeks to unlock key strategic lessons from the world’s most successful investors.

While you’re looking at US-based podcasts, you’ll likely find financial research publisher The Motley Fool’s show, Motley Fool Money. These short and sweet daily episodes don’t necessarily follow a strict theme, like We Study Billionaires or QAV.

Host Chris Hill and a revolving cast of the firm’s analysts cover daily business and market headlines and break down implications for stocks and investors.

On the weekends, they run investing class-style episodes that teach financial and investing literacy from ‘special guests helping to shape the future’.

One notable feature of Motley Fool Money is the show’s episode notes, which break down key talking points with timestamps, and list the ticker symbols of any stocks discussed in that episode. Great for browsing and finding episodes on companies you hold or want to know more about!

#9: WSJ Your Money Briefing — Financial Literacy With Wall Street’s Leading Journalists

While we’re talking big American personal finance podcast players, I should mention the Wall Street Journal‘s Your Money Briefing. Billed as a ‘personal finance and career checklist’, Your Money Briefing is another show that seeks to interpret mainstream financial and economic news and translate that into actionable personal finance ideas for the listener.

Whether it’s spending and saving habits, predictions on energy prices or trends in the corporate workforce, the show is broader than just stock market commentary.

The Wall Street Journal is one of the premier business publications on the planet, and their reporters and analysts are among the best in the business.

One interesting piece of trivia about Your Money Briefing is that the host, J.R. Whalen, was in a past role responsible for assigning dollar values to each question on the show Who Wants To Be A Millionaire. If that’s not a sign that this show’s host understands the value of information, I don’t know what is.

Your Money Briefing runs daily Monday to Friday, and joins nine other high quality podcasts in the WSJ stable — one of which I cover below.

The WSJ runs the Your Money Briefing podcast.

#10: WSJ The Future Of Everything — Covering Big, World-Shaping Trends

The WSJ’s future focused podcast aims to answer a big question — what will the future look like? By projecting the trends we’re seeing in the world today into the decades ahead, The Future Of Everything brings a unique macro view to any investor’s podcast library.

You can expect plenty of science and tech — obviously — and you’ll find a nice balance between both challenges facing civilization and the breakthroughs that could overcome them.

Episodes tackle big topics like how best to decide which species to save and whether genetically modified crops are the future of food.

Hosted by Danny Lewis and Alex Ossola, The Future Of Everything comes out about every fortnight. Each episode runs for around 20 minutes.

#11: Money For The Rest Of Us — Former Pro Investor Helps Everyday People Build Wealth

Former financial advisor and money management expert Bret Stein quit his professional investing career after 20 years and started the Money For The Rest Of Us Podcast.

The big idea is that Bret now shows listeners how to apply the principles and investment philosophies he developed at $15 billion asset management firm FED Investment Advisors in their retail investing and personal finance journeys.

Money For The Rest Of Us is less about financial news and economic coverage than is is about how those things impact personal finance, investment strategy and retirement planning for everyday investors.

According to Bret, ‘Money For the Rest of Us is for people like you and me who aren’t relying on someone else to make sure we have enough to retire. We’ve taken control of our financial future’.

With close to 20 million downloads, this personal finance podcast is among the most popular of its kind. And it goes beyond just the weekly personal finance podcast episodes, which run for around 30 minutes.

Money For The Rest Of Us also offers free reports, an email newsletter, a members-only education platform (which teaches students to manage their personal finance like a professional) and Bret’s book, Money for the Rest of Us – 10 Questions to Master Successful Investing.

Money For The Rest Of Us is one of the most popular personal finance and investing podcasts.

#12: Contrarian Edge — Great Content On Investing & Life

Vitaliy Katsenelson is a deep thinker whose curiosity about the world of finance extends beyond just the markets and investing. A professional investor, educator and writer, Vitaly’s Contrarian Edge blog is packed with deeply researched and brilliantly-written content.

The prolific Vitaliy shares opinions and analysis on a wide range of subjects related to investing. From macroeconomic and geopolitical coverage through to single stock analysis, personal finance and more philosophical pieces on the qualities and principles one need cultivate for a fulfilling investment journey, Contrarian Edge is as informative as it is entertaining.

Vitaly has published two books to date, Active Value Investing and The Little Book of Sideways Markets, with a third title on the way at the time of writing.

While Contrarian Edge is a blog, you’ll also find podcast episodes on the site — a mix between Vitaliy’s guest appearances on podcasts and audio versions of his blog posts.

#13: Value Investing with Sven Carlin, Ph.D. — The Dedicated Value Investing YouTube Channel

You won’t find many people with a doctorate in investing. But Dr, Sven Carlin is one such man. Having developed a Real Value Risk Model for emerging market stocks during his studies, Sven has worked for Bloomberg in London and taught finance and account at The Amsterdam School of International Business.

Today, he runs the 200k-plus subscriber YouTube channel, Value Investing with Sven Carlin, Ph.D. The channel is packed with video content on everything from individual stock analysis and commentary, commodities, tips for beginner investors, investing book reviews, and Sven’s YouTube model portfolio, which he launched in 2022.

The model portfolio is an interesting differentiator here. Not many other YouTube investing content creators go beyond the tried and true (and, once you’ve watched a few of them, tedious) ‘how to open a brokerage account’ and ‘3 most popular ETFs’ formats.

Sven’s plan with his YouTube portfolio is to build a $1 million paper portfolio and run it for several decades, with regular videos explaining trades, trends, and the reasoning behind investing decisions.

Sven’s inspiration for his YouTube portfolio is one of the all-time value investing greats.

Munger’s 50-Year Journey To Find a Single Worthwhile Investing Idea

Berkshire Hathaway’s Charlie Munger is infamous for his contributions to the firm’s world-beating investment performance.

One of his stories illustrates how discerning the man is with investment ideas. Barron’s, a sister publication to the Wall Street Journal, has been around more than a century. Munger read the magazine for half a century before he found an investment idea in it that he thought worth following.

According to Munger: ‘In 50 years I found one investment opportunity in Barron’s out of which I made about $80 million with almost no risk. I took the $80 million and gave it to Li Lu who turned it into $400 or $500 million. So I have made $400 or $500 million reading Barron’s for 50 years and following one idea.’

This is what Sven Carlin is trying to emulate with his YouTube portfolio; a long-term investment idea generator which perhaps uncovers one big winner, and which teaches much along the way.

Charlie Munger claims to have made $500 million by reading Barron’s for 50 years.

#14: The Acquirer’s Podcast — Making Complex Financial Analysis Casual & Entertaining

Here’s another podcast that’s also a blog and, in this case, an investment fund. Tobias Carlisle is a professional investor, author, and lawyer. He runs The Acquirer’s Multiple, where he shares his wisdom from a career spent managing merger and acquisition transactions, and his own deep value investing.

Tobias has published four value investing books. Most recently, The Acquirer’s Multiple: How The Billionaire Contrarians of Deep Value Beat The Market was the #1 new business and finance book on Amazon. Over on his website, The Acquirer’s Multiple, you’ll find The Acquirer’s Podcast, along with the ‘absurdly simple, ridiculously powerful’ stock screener which is available on a subscription basis.

The podcast itself is super high quality. It leans more towards to expert end of the finance podcast spectrum. It’s long-format and doesn’t dumb anything down. The episodes I’ve listened to are packed with interesting information, but they don’t put you to sleep like some of the other expert-level shows you might stumble upon.

If you’ve seen The Big Short (which I list below, for reasons I’ll explain), you’ll have enjoyed that rare balance of dense finance topics with light, accessible explanation. Or, you will have become dizzy with all the Wall Street jargon, slam zooms and quick cuts.

I mention this, because tuning into The Acquirer’s Podcast feels sort of similar to watching this film. You’re in the room with veteran professional investors whose careers and lives have been shaped by the markets. They speak the language of Wall Street, but they let you in on what it means.

This recent episode features Tobias and his two regular guests discussing the complexities of defining a bear market. It’s a great example of the sort of content you’ll get from the podcast — market and economics analysis discussed by professional traders as though they’re enjoying a post-work debrief at a bar.

#15: The Big Short — The Feature-Length Adaptation Of The 2008 Subprime Crisis

I know. It’s not a personal finance podcast or YouTube channel. But hear me out. Because while there’s plenty of shows and channels out there for market and economics commentary and education, there are relatively few that take you behind the scenes of the upper echelons of the financial markets.

Adam McKay’s The Big Short is, in my opinion, a must-watch for anyone investing in the markets. Why? Because in just over two hours, the film explains the 2008 global credit crisis with both massive scope and detailed depth.

The cast of characters includes Christian Bale’s memorable performance as Dr. Michael Burry, the hedge fund manager who predicted and led the betting against the crash. It pulls together top-tier dramatic talent like Ryan Gosling, Steve Carrell and Jeremy Strong with celebrity cameos from Margot Robbie and the late Anthony Bourdain, all in service of explaining and illustrating the economic, market and cultural circumstances that set up the biggest crash (so far) of the 21st century.

The film goes deep into the psychology of the people who contributed to, predicted and profited from the ’08 subprime crash. More than any other film about the financial markets — which tend to get lost in portraying the luxury lives of the ultra-wealthy — The Big Short illustrates the disconnect between Wall Street and Main Street in early-2000s America.

To go even deeper into this fascinating episode of financial history, check out the Michael Lewis book, The Big Short: Inside The Doomsday Machine, on which McKay based his film.

The Big Short is perhaps the best investing film ever made.

#16: A Wealth Of Common Sense — Pro Institutional Investor Making the Complex Simple

While we’re looking at content that helps you navigate the complex world of finance and economics, I should mention A Wealth Of Common Sense. This blog, written by Ben Carlson (Director of Institutional Asset Management at Ritholz Wealth Management) is another example of a professional investor breaking down market news and analysis for everyday readers.

Huge institutions turn to Ben for investment advice and portfolio guidance. Having managed people’s money his whole career, he has broad and deep knowledge of the markets, money and financial advice. But his ethos on the blog — and the accompanying podcast, Animal Spirits — is to keep it simple.

According to Ben: ‘Both the economy and the financial markets are complex adaptive systems, but I’ve never found complex problems require complex solutions. Common sense and self-awareness are extremely underrated attributes in the world of finance.’

This post on surviving bear markets at different stages of life is a brilliant example of the quality and readability of Ben’s writing. And this episode of Animal Spirits shows you the type of in-depth analysis and commentary you’ll find on the show’s weekly, roughly hour-long episodes.

How To Make The Most Of Financial Independence & Personal Finance Podcasts

So there you have it. My 16 best personal finance and investing podcasts and blogs from across the web. From advanced, pro trader-level podcasts to more everyday content aimed at helping ‘normal’ people invest, save money and build their financial independence.

The shows and sites (and the feature film) I’ve featured here give, IMHO, a wide range of content that I hope result in you discovering at least one new resource on your own financial journey.

Of course, I have included two finance podcasts that we’ve appeared on ourselves here at Navexa. That’s because we’ve created a platform to help investors make the best possible financial decisions for their investment portfolio.

The Navexa Portfolio Tracker: Optimize Your Investment Journey

Whatever your financial goals, or which industry experts you might listen to for tips on money matters and financial topics, one thing we all need on our personal financial journey is a reliable tool for tracking our performance and returns.

As you’ll hear on our episode of the QAV Podcast with Cameron and Tony, our founder Navarre is a long-term, buy-and-hold investor to whom strong, annualized returns matter more than eye-grabbing one-off gains.

He’s been learning about investing for a long time. Everything he’s learned has proved it’s far better to work with hard data than skewed or incomplete information about a portfolio.

This is why the Navexa Portfolio Tracker, today, is one of the leading portfolio tracking platforms. It allows you to add portfolio data from stock brokers, crypto exchanges, cash accounts and even unlisted investments like property.

This means you can track all your investments in one place. Which, in turn, means you can look at your overall portfolio performance, measured together using the same industry-standard performance calculation.

Once you load your portfolio into Navexa, you can see true performance over the long term. You can see at a glance your capital gains, currency gains, investment income — all net of your trading fees.

You can run comprehensive tax reports with a couple of clicks. You can track & analyze more than 8,000 ASX & US-listed stocks and ETFs, plus cryptos, cash accounts and unlisted investments (like property).

And, you can go even deeper, running reports like Portfolio Contributions, which shows you in chart form which of your investments are boosting (and which are dragging down) your overall performance.

Invest In Knowledge While You Invest in The Markets

We’ve developed Navexa so that you can spend more time learning about the financial and economic forces driving the markets, the strategies that some of the world’s best investors use to outperform the rest of the market, and the investing and personal financial principles that underpin strong long-term investment strategies.

How? Because once you start tracking your portfolio performance in Navexa, you’ll no longer need to spend time manually tracking, calculating and reporting your investment performance — especially at tax time, when the government requires you provide accurate, comprehensive records of every trade and transaction you’ve made in a given financial year.

Not that podcasts or blogs were around in his time, but Benjamin Franklin famously (among many other things) said, ‘an investment in knowledge pays the best interest’. By which he meant that taking the time to learn about how money and the markets work can be more valuable than buying and selling investments themselves.

Between the 16 investing and personal finance podcasts and blogs I’ve detailed here, and the powerful portfolio performance tracking tool we provide here at Navexa, I hope you’re now better equipped to learn about investing and to build your financial literacy!

Your guide to calculating capital gains tax in Australia in 2022. From tax rates, CGT events, taxable income and more. Plus, discover four key tax reporting strategies investors use to adjust and optimize their total taxable capital gain.

Paying tax is a part of investing. It has long been a fact of life that a significant portion of our earnings will always be earmarked for payment to the state. This includes capital gains.

Tax is applied to a wide range of earnings including wages, salaries, and investment income from property, shares, and cryptocurrency.

In Australia, the tax rate that is applied to your investment income is known as the Capital Gains Tax, or CGT.

Whether you’re a seasoned investor or just starting out, it’s important to be aware of how CGT works. This article will explain how the CGT works, and how to calculate and report your capital gains in Australia in 2022.

While you can’t avoid paying CGT on your investment income, there are some strategies you should be aware of for minimizing the impact of tax on your capital gains. This blog post examines some of these strategies and provides examples of how they might look.

The Australian tax year, or financial year, runs from July 1 to June 30. This is the period for which you will need to submit your tax assessment based on any income you received during the financial year. This period is known as ‘tax season’.

How Does CGT Work?

The Australian Tax Office (ATO) requires individuals to declare investment activity in their tax return and pay tax on all investment earnings, including capital gains and dividend income.

If you buy shares, invest in property, or hold other investments which you sell at a higher price than what you bought them for, you will have made a capital gain. This means you will be paying CGT.

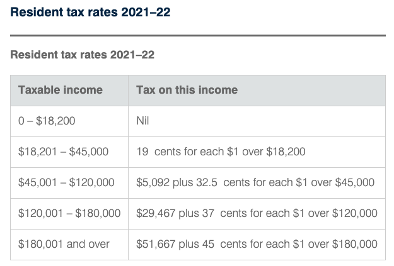

CGT is the tax rate that is applied to net capital gains (total gains minus total losses). It is not a set rate, but is calculated according to your marginal tax rate. This is the tax rate that you usually pay on your personal income, and will be the tax rate applied to your investment earnings.

Capital gains are taxed at an individual’s marginal tax rate

While CGT rates for individuals vary according to their marginal tax rate, flat rates apply for companies and self-managed funds.

Trading companies pay 26% if their annual turnover is less than $50 million, and if it exceeds $50 million, the CGT applied is 30%. Investment companies don’t qualify for the 26% rate and are taxed at 30%. Self-managed super funds are taxed at a lower rate of 15%.

If you sold any assets during a financial year, you will need to work out your capital gain or capital loss for each asset. CGT will need to be paid on your net capital gains.

To calculate your capital gains, you first need to know the ‘cost base’ or original purchase price of the asset. From there, you can work out how much profit you’ve made by subtracting the selling price from the cost base.

Depending on how long you’ve held the shares for, you may or may not qualify for Australia’s 50% CGT discount on investments held longer than 12 months.

The Navexa platform provides an automated solution for making these calculations — more on that later.

That’s how the CGT rate is determined. So, let’s take a closer look at which investments the CGT applies to.

What Does CGT Apply To In Australia?

CGT applies to a wide range of investment income in Australia, including earnings generated from real estate, shares, cryptocurrency, foreign exchange, and collectibles.

When you dispose of an asset for more than what you paid for it, you realize a capital gain which you will have to pay CGT on.

There are a range of other situations that will trigger the requirement to pay CGT. These are known as ‘CGT Events’. A CGT event occurs when an investor makes a capital gain or incur a capital loss on an asset.

The Australian Tax Office (ATO) imposes CGT when you make a capital gain or loss

How Does CGT Apply To Shares?

When you sell shares for more than what you paid for them and realize a capital gain, you will have to pay CGT. When other CGT events occur, you will also have to pay CGT on your shares. Examples include switching shares in a managed fund between funds, or owning shares in a company that is subject to a takeover or merger.

It is important to keep good records of all your share transactions, including amounts and dates of purchase. When you file your tax return, CGT will need to be calculated for any profits you made from selling your shares.

Does CGT Apply To Dividend Pay-outs?

Many Australian investors enjoy investing in companies that pay out dividends (a percentage share of their profits) to their shareholders. But, like other forms of income, dividends are subject to taxation.

Dividends are paid from profits that have already been subjected to Australian company tax. Because the profits have already been taxed, shareholders won’t be taxed again when they receive the profits as dividends, provided that their marginal tax rate is lower than the tax rate paid by the company.

These dividends are described as being ‘franked’. A ‘franking credit’ is attached to the dividend and represents the tax that has already been paid by the company distributing the dividend. The shareholder who receives the dividend with an attached franking credit will either pay less than their usual tax rate, or receive a tax refund.

The general rule is that if your marginal tax rate is lower than the rate of tax paid by a company or fund, you might be entitled to claim a refund. However, if your marginal tax rate is higher than the tax already paid on the dividend, you may have to pay additional tax.

Does CGT Apply To Crypto?

If you were hoping to avoid paying CGT by investing in cryptocurrency, we have bad news for you. Cryptocurrency investment in Australia is also subject to taxation, in a similar way to other investment assets.

In recent years, the cryptocurrency market has grown rapidly, and the ATO has been quick to catch up.

Crypto gains are subject to CGT in Australia.

Cryptocurrency markets have exploded in recent years and the ATO is all over it

As with other assets, CGT may apply in circumstances other than just selling your crypto. The ATO classifies four main CGT events for crypto activity:

You’ll be taxed when you:

Sell crypto.

Exchange one crypto for another.

Convert crypto to a fiat currency like AUD.

Pay for goods or services in crypto.

Just like when you pay CGT at your marginal tax rate when you sell shares, you pay this rate when you sell crypto.

Generally, you could apply the same tax rules to your crypto portfolio as you would for investment in stocks.

You must pay CGT when you realize a capital gain from property. This could include selling an investment property for more than what you paid for it or selling a block of land that you created through a subdivision process.

Your main residence is generally excluded from CGT if you meet certain criteria specified by the ATO:

You will need to have lived in the home for the whole period that you have owned it.

The home can’t have been used to produce income or have been bought with the intention of renovating and selling it for a profit.

It must be on land no greater than two hectares.

If you meet the criteria, you may be able to avoid paying CGT when you sell your house. If not, you may still qualify for a partial exemption. The ATO provides a property exemption tool on their website to help you make the calculations.

In Australia, investors can expect to pay CGT on shares, crypto, property and more.

Capital Gains Tax (CGT) has to be paid on investment income from property

If you acquired property on or prior to 20 September 1985, CGT does not apply. But it will apply to certain capital improvements made after this date. It is also important to keep track of any rental income you receive from property and include it in your tax return. For more details on CGT and property, visit the ATO.

If You Are An Investor, It Pays To Know About CGT

As you can see, CGT applies to a wide range of investment income. When you prepare your tax return, you will need to provide the ATO with your assessable income and any capital gains or capital losses you made that year.

While this article isn’t financial advice, we do advise you to be well informed. The above is not an exhaustive list of what CGT applies to in Australia, so you should check with the ATO if you are unsure about what your tax obligations are.

You can’t escape having to file a tax return, but fortunately there are a few strategies you can use to reduce your tax burden, legally.

Let’s explore some of the strategies that investors use to minimize investment tax.

Effective Strategies To Minimize Tax Payments

There are several legal investment strategies investors employ to minimize tax bills and claim tax deduction. This goes for both gains and income.

Below you’ll find some of the ways Australian investors hold on to as much of their investment gains and income as possible.

The following is not investment advice. As with all the information on the Navexa blog, it’s general investment information our writers have collated from other sources. For any financial or investment decisions, you should always understand the risks, and seek professional advice if necessary.

Strategy 1: Hold Onto Your Investments For Longer Than 12 Months

Australian tax law makes a distinction between short and long term capital gains. A long term capital gain is when you make a profit on an investment that you’ve held for longer than 12 months. It’s a short term capital gain if you’ve held the asset for shorter than 12 months.

As an investor, this is important to understand because of something known as the ‘CGT discount’.

If you’ve held an asset for longer than 12 months before a given ‘CGT event’ occurs, you may be able to claim a CGT discount of 50%. Remember, a ‘CGT event’ is the point at which you make a capital gain or loss on an asset.

Let’s say you made $30,000 profit from investments that you’d held for less than 12 months, and your marginal tax rate was 37%. You’d have a $11,100 tax liability.

However, if you’d held the asset for longer than 12 months before you sold, the CGT discount would mean your tax liability was just $5,500! That’s a significant amount saved on your tax bill.

Capital Gains Tax discount applies to a wide range of investment income, including shares, property, and cryptocurrency.

As you can see, holding onto your investments for longer than 12 months to take advantage of this discount can be much more tax effective than disposing of them quickly.

Remember, you must be an Australian resident for tax purposes to take advantage of the CGT discount. There are also some other situations where the CGT discount does not apply.

For example, the discount is not available if the asset is your home and you started using it as a rental property or business less than 12 months before disposing of it.

A CGT discount of 50% is available to Australian trusts, and complying super funds can receive a discount of 33.33%. However, companies can not take advantage of the CGT discount.

When you file your tax return, you must subtract any capital losses that you may have from your capital gains before applying the CGT discount. In most cases you will be eligible for the discount if the asset has been held for longer than 12 months.

Navexa provides a platform where you can easily track your portfolio performance and calculate both your taxable capital gains and taxable income. Our CGT Reporting Tool gives a detailed breakdown of which assets are ‘non-discountable’ from a CGT perspective (those which have been held for less than the required 12 months to qualify), reducing the amount of tedious leg-work at tax time.

Navexa’s tax reporting tools remove the need to manually calculate your portfolio’s tax obligations and show you the most tax effective way to prepare a tax return.

Provided the portfolio data in your account is correct and up-to-date, you can run an automated tax report in just a few seconds.

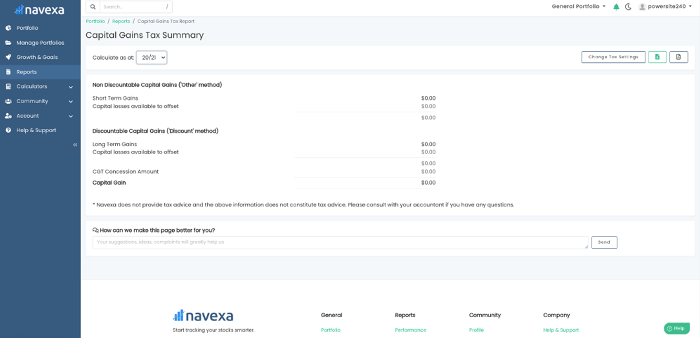

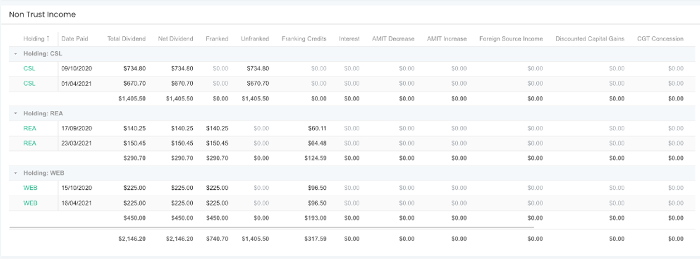

Navexa’s CGT Reporting Tool.

What you see above is Navexa’s CGT Report.

Navexa calculates your taxable gains and displays a detailed breakdown. Capital gains are displayed according to Short or Long Term status alongside your Capital Losses Available to Offset. The report also calculates your CGT Concession Amount and finally, your total Capital Gain.

Navexa’s CGT Reporting Tool makes it easy to categorize your investments for your tax return.

Strategy 2: Offset Your Capital Gains With Capital Losses

Another useful strategy at tax time is using capital losses to offset your capital gains. While it would be nice if your assets always made gains and never losses, most of us who invest know that this isn’t the case. Thankfully, the silver lining here is that your capital losses can be used to reduce the tax you pay on your capital gains.

You will have made a capital loss when you sell an asset for less than what you paid for it. This loss can be deducted from capital gains that you made from other sources, to reduce the tax you pay. If you don’t have any capital gains to deduct from, the capital loss can generally be carried forward to future financial years. If you make capital gains in future years, the capital losses are still up your sleeve to deduct from any gains and reduce tax.

While there is no time limit on how long you can carry the losses forward if you don’t make any gains, the ATO does require that capital losses are used at the first available opportunity. This means when you have a capital gain to declare and capital losses available to offset, you must do so. They also require the earliest losses to be used first.

For example, if an investor owed $5,000 in CGT for their investments in a financial year, but had declared losses of $1,500 the previous financial year, they could carry these losses over to offset their capital gain, resulting in a reduced tax bill of $3,500.

There are some capital losses that can’t be deducted, so be aware of these. These include personal use assets such as boats or furniture, or collectables below a certain value. The ATO also won’t allow capital losses to be deducted from collectables unless they are deducted from capital gains from collectables.

Capital losses can also be deducted from your cryptocurrency assets, too. Let’s say you bought $5,000 worth of Ethereum because it had been surging in price and you were experiencing crypto-FOMO. You buy near the peak and in subsequent weeks the price crashes heavily, after a large nation announces that it won’t endorse cryptocurrency in their economy. Despite this disappointment, don’t forget that if you sell the asset and realize a capital loss, it could be a handy tool to offset other capital gains in your portfolio.

Despite a few exclusions, however, most capital losses from your investments can be deducted from capital gains you have made from other assets. If you are unsure about whether you can deduct a particular capital loss, check with the ATO.

Strategy 3: Invest In Companies That Pay High Dividends And Franking Credits

We’ve already looked at how the ATO taxes dividends, so what does this mean for minimizing your income tax obligations? Again, this is not financial advice.

Remember that companies must pay the Australian Companies Tax on their profits. If an investor receiving a dividend has a tax rate greater than the company tax rate that has already been applied to the company’s profits, they will receive a franking credit.

Let’s look at an example. Say an investor with a 32.5% tax rate receives a $1,750 dividend with a $750 franking credit attached. The franking credit takes the taxable income to $2,500, with gross tax of $812.50 payable. The franking credit rebate of $750 is deducted from the gross tax and the investor is left to pay a reduced tax amount of $62.50, leaving them with $1,687.50 after tax income. As you can see, the impact of the franking credit rebate is significant. For a full breakdown of this and other franked dividend scenarios, click here.

The investor in the above situation manages to retain most of their dividend income. Because the franking credit offsets their CGT so significantly, the amount of tax the individual pays is greatly minimized. Obviously, if your marginal tax rate is lower than 32.5% you will pay less tax and receive a larger chunk of the dividend. If you’re in a higher tax bracket than this, you will receive less.

Regardless of your marginal tax rate, franked dividends are a useful tool to reduce your tax obligations. Choosing to invest in companies that pay dividends, especially fully or highly franked dividends, is a popular strategy for minimizing tax paid on investment returns.

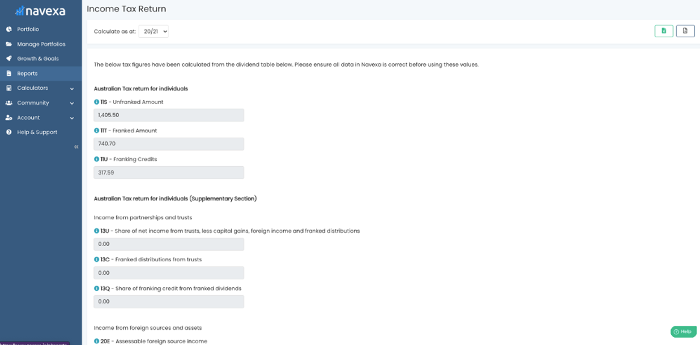

Navexa’s Taxable Income Reporting Tool

Navexa can help you accelerate the process of determining your taxable income. When you automate your portfolio tracking in Navexa, the Taxable Investment Income Report provides you with everything you need to know to prepare your tax return.

Navexa’s Taxable Investment Income Tool.

As you can see above, the Taxable Income Tool displays the Unfranked Amount and the Franked Amount for your dividends, as well as the total franking credits attached to them.

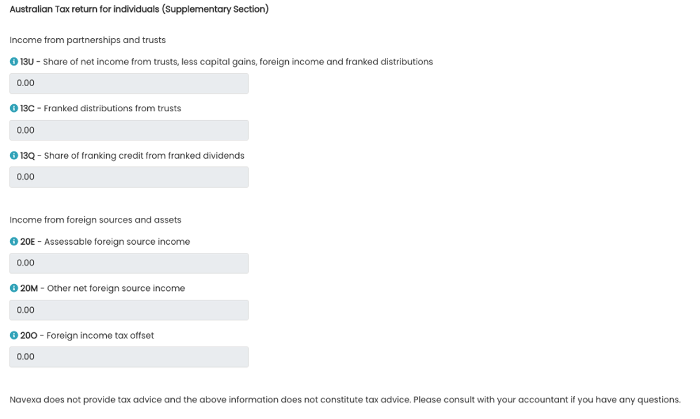

And in the below image, you can see the additional fields in the ‘Supplementary’ section. These display further tax-relevant information such as the amount of Franked Distributions From Trusts, the amount of Assessable Foreign Source Income, and your Foreign Income Tax Offset.

The report automatically categorizes sources and tax return codes.

A foreign income tax offset is when you may have already paid tax on something in another country. This might be employment income or capital gains. In some instances, you may be able to claim a foreign tax offset as part of your tax return. Navexa’s Taxable Investment Income Tool will calculate and display these details for you.

Below these fields, you’ll be provided with a holding by holding breakdown of your taxable investment income, like this:

Navexa’s holding by holding investment income breakdown.

This shows you subtotals for payments from each holding, with grand totals for each column at the bottom. Assets are organized by the dates at which you acquired them, which has important tax implications.

At the top right of the report, you’ll find buttons for exporting the report as both an XLS and a PDF file.

This helps you accelerate the process of preparing your investment income for assessment.

Let’s take a look now at how different investors might choose to dispose of their assets.

Different Tax Strategies For Disposing Of Investments

When the time comes that you want to sell, it can be easy to get excited about the potential gains you are about to realize. This excitement can be dampened, however, when you are faced with the reality of your tax bill.

Choosing a particular method to dispose of your assets can have a major impact on the profits you generate and the tax you pay on them.

Please remember that this does not constitute financial advice. Our writers have collated a wide range of information relating to investment tax that we think is useful for you to consider. As always, we recommend you do your own research before making any investment decisions — tax or otherwise

Strategy 1: First-In-First-Out (FIFO)

The first-in-first-out (FIFO) approach is a common method used by investors when they sell holdings. When you purchase a group of shares at a given price, they will constitute a ‘parcel’.

You may acquire shares in the same company in several different transactions over a period of time. Each transaction forms its own parcel of shares.

The concept of FIFO relates to the disposal of investments. When you are ready to sell shares, you can choose which parcels — sometimes called ‘lots’ — of shares you would like to sell.

Using the FIFO method, you would sell the parcels that have been held for the longest period. Provided that the share price has risen since the time of purchase, the FIFO method will ensure the greatest capital gain from the sale of a parcel of shares. Obviously, this won’t always be the case, and adopting a FIFO approach might not result in the greatest capital gain.

For example, if an investor purchased 100 shares in a company at $20 per share three years ago, and another 100 shares at $40 two years ago, they might choose to use the FIFO method when they choose to sell some of those shares.

Let’s say the company’s share price has now risen to $50. The investor sells using the FIFO method, disposing of the first 100 shares that were purchased at $20. Because the share price has grown $30 since they purchased them, they realize a gross profit of $3,000. However, if they had chosen to sell the more newly acquired shares parcel, they would only realize a gross profit of $1,000.

As mentioned, FIFO will only result in the largest capital gain if the share price has risen consistently over time. If share prices have dropped since you bought them, the FIFO approach might not result in the greatest capital gain — but it could lower your tax burden.

Strategy 2: Last-In-First-Out